Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

How to set up line of credit (overdraft) products

Updated

On this page

Introduction

Your customer needs cash urgently but does not want to apply for a new loan every time. Your business borrower wants a buffer for slow months without going through a full credit process repeatedly. A line of credit solves both problems.

Unlike a traditional loan, a line of credit does not disburse a fixed amount upfront. Instead, borrowers draw funds up to a set limit whenever they need it. They pay interest only on what they actually use. This makes it an ideal product for customers with recurring short-term needs or businesses that want cash on demand without repeated applications.

On Lendsqr, you can configure any wallet-based loan product as a line of credit directly from the admin console. This guide walks you through the full setup and explains how to choose the right interest strategy for your borrowers.

What is a line of credit, and how does it work?

A line of credit is a type of revolving credit facility. The lender sets a credit limit. The borrower draws from it as needed, repays what they used, and the available credit replenishes. Unlike a term loan, the borrower does not receive the full amount at once and does not pay interest on funds they have not drawn.

This structure suits several real-world lending scenarios.

A trader runs a small retail business. Their cash flow fluctuates monthly depending on stock cycles. A line of credit lets them draw funds when inventory needs restocking and repay when sales come in, without applying for a new loan every cycle.

A salaried employee faces an unexpected car repair midway through the month. Instead of applying for a full personal loan, they draw only what they need from their available credit line and repay it on payday. They pay interest only on that amount, not on the full limit.

In both cases, the borrower gets flexibility. The lender retains control through a configured credit limit and interest structure.

Why offer a line of credit?

Lenders across different markets are adding this product to their portfolios. Here is what it delivers.

Flexibility for borrowers. Customers access funds as needed rather than taking one lump sum upfront. They borrow on their own terms within the limit you set.

Pay for what is used. Borrowers pay interest only on the amount they draw, not the full credit limit. This makes the product more attractive and more affordable than a traditional loan of the same size.

Customer loyalty. Offering an overdraft builds stickiness. Customers stay with lenders who give them adaptable credit solutions they can rely on repeatedly.

Efficiency for lenders. Fewer repeat loan applications mean faster turnaround times and lower processing overhead for your team. One approved credit line replaces multiple individual loan applications from the same borrower.

Before you begin

Line of credit only works for loan products where the “Disburse To” setting is configured as “Wallet.” Confirm this before you start. If your product disburses to a bank account, update that setting first before enabling the credit line configuration.

You also need admin-level access to manage loan products on the admin console. To understand how loan product settings work more broadly, see: Configuring your loan product.

Step-by-step guide

1. Login to the Admin Console 2. Click on “Loan Products” under “Product Management“

3. Create a loan product or open an existing one

Line of credit only works for products configured with disburse to set to ‘wallet’.

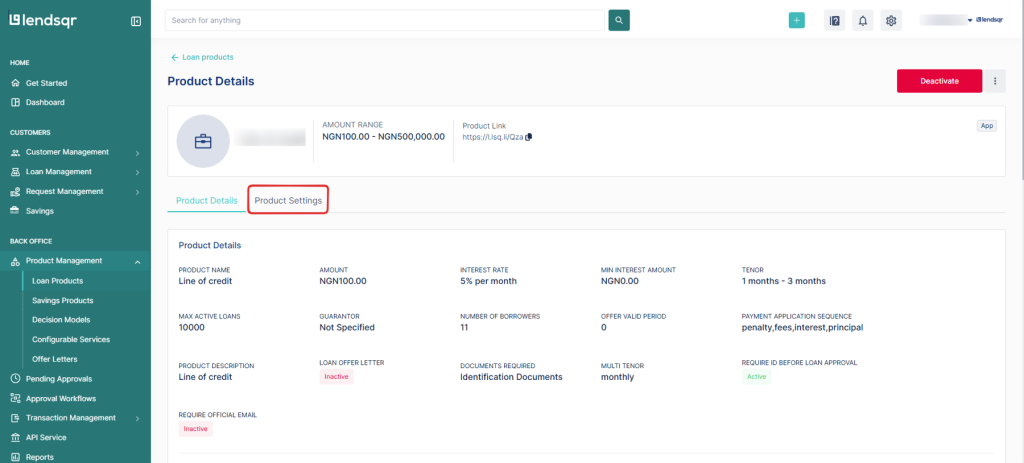

4. Click on the “Product Settings” tab on the “Product Details” page.

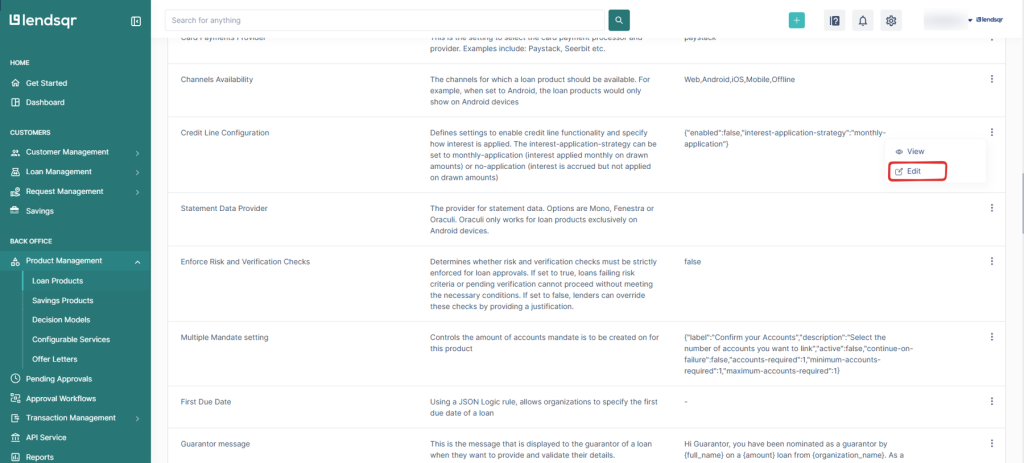

5. Locate the “Credit Line Configuration” setting. Click on the “three-dot” icon and select “Edit” beside this setting. By default, this setting is disabled.

6. To enable the credit line, check the box Enabled to activate credit line functionality for this product, and click on the “Submit” button to apply the changes to the product.

7. Select Interest Application Strategy: This is where you define how interest will be applied to drawn amounts. You have two options:

Monthly application applies interest at the end of each month based on what the customer has actually drawn.

No application accrues interest without formally applying it to the drawn amount each month. Lenders typically use this when they want to defer interest to a later date, such as at final settlement.

8. Once you’ve selected your strategy, click Submit. Review your configuration carefully and confirm to save changes.

Your loan product is now configured as a Line of Credit (Overdraft)

Choosing your interest application strategy

The interest application strategy determines how Lendsqr calculates and applies interest on the amounts your borrowers draw. Choosing the right strategy shapes how your borrowers experience repayment and how your revenue accrues.

Monthly application

Lendsqr applies interest at the end of each month based on the amount the customer has actually drawn. For example, a borrower has a credit limit of $10,000 but draws only $3,000 in October. Lendsqr charges interest on the $3,000 only, not the full limit.

This strategy gives borrowers a predictable monthly picture of what they owe. It reduces missed payments because borrowers always know their current obligation. For most retail and SME lending contexts, monthly application is the safer and more transparent default.

No application

Lendsqr accrues interest on drawn amounts without formally applying it to the account each month. The interest builds up and applies at a later date, typically at final settlement or at a point defined in your product configuration.

This strategy suits structured credit arrangements where both the lender and borrower agree upfront to defer interest to a specific settlement date. It works best with more sophisticated borrowers who understand deferred interest arrangements and have the financial capacity to settle a larger amount at once.

For most consumer and small business lending, a monthly application is the recommended choice. It keeps repayment straightforward and builds trust with borrowers who need visibility into what they owe.

How Lendsqr enables line of credit on your platform

Setting up a line of credit on Lendsqr does not require a separate product category or a different platform. You configure it directly within your existing loan product framework through the Product Settings tab.

Once enabled, the credit line configuration works with Lendsqr’s wallet infrastructure to track each borrower’s available balance, drawn amount, and repayment activity in real time. Borrowers see their available credit limit on their web or mobile app and can draw funds within that limit without submitting a new application each time.

This makes Lendsqr’s line of credit setup particularly practical for lenders who want to add a revolving credit product to their portfolio without building a separate system or undergoing a lengthy configuration process.

Troubleshooting

The Credit Line Configuration setting is not visible in Product Settings. Confirm that your product’s disbursement to the setting is configured as a wallet. The credit line option does not appear for products that disburse to a bank account.

The Enabled checkbox is greyed out. Check that you have admin-level access to edit loan product settings. If your role and access appear correct, contact Lendsqr support for assistance.

Borrowers are not seeing the credit line option on the web app. Confirm that the loan product is active and published. Also, confirm that the credit line configuration is enabled and saved correctly in Product Settings.

I selected the wrong interest strategy after publishing. Contact Lendsqr support before making changes to a live product with active borrower credit lines. Changing the interest strategy on a live product may affect existing drawn balances and repayment schedules.

Frequently asked questions

Can I set different credit limits for different borrowers on the same product? Yes. Credit limits can be set at the individual borrower level within your loan product configuration. Contact your Lendsqr support contact for guidance on configuring customer-specific credit limits.

Can I convert an existing loan product to a line of credit? Yes. Open the existing product, navigate to Product Settings, locate Credit Line Configuration, and follow the same steps above to enable it. Confirm that the product disburses to wallet first.

Can a borrower exceed their credit limit? No. Lendsqr blocks draw requests that exceed the configured credit limit. Borrowers can only access funds up to the limit you set on the product.

Can I change the interest strategy after the product goes live? Making changes to the interest strategy after borrowers have active draws may affect existing repayment schedules. Review the impact carefully and contact Lendsqr support before making changes to a live product.

Does the line of credit work on both mobile and web apps? Yes. Once configured on the admin console, the line of credit product is available to borrowers through both the web app and mobile app. Borrowers can view their available balance and draw funds from either channel.

feature")