Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

How to configure upfront interest on your loan product

Updated

On this page

In some lending scenarios, collecting interest after disbursement can increase repayment risk—especially for short-term or high-volume loans.

Upfront interest solves this by allowing lenders to collect the interest portion of a loan immediately when the loan is disbursed.

For example, a digital lender offering ₦50,000 quick loans can deduct the interest before sending funds to the borrower. This ensures the lender earns revenue upfront, even if the borrower defaults later.

In Lendsqr, this is configured directly within your loan product settings.

What is upfront interest in lending?

When a lender disburses a loan, they typically collect interest in installments spread across the repayment period. Upfront interest flips this model: the interest portion of the loan is collected at the moment of disbursement, before the borrower receives their funds.

In practice, this means a borrower approved for $1,000 at 10% interest would receive $900. The $100 interest is deducted upfront. Repayments then cover only the principal.

This model is common among short-tenor lenders, salary advance providers, and microfinance institutions that want to eliminate the risk of interest default entirely. If a borrower cannot repay, the lender has already secured their return.

Why lenders use upfront interest

Immediate revenue recognition — Interest income is locked in at disbursement, regardless of repayment behavior.

Reduced credit risk — Late payments only delay principal recovery, not your profit margin.

Simpler cash flow forecasting — You know exactly what you have earned the moment a loan goes out.

For borrowers, the trade-off is transparency: they receive a smaller net amount but carry no interest burden in later installments. For short-term loans, this is often a fair exchange.

When should you use upfront interest?

Upfront interest is commonly used when:

Offering short-term or payday loans

Lending to new or high-risk borrowers

Running high-volume digital lending operations

You want predictable revenue at disbursement

How upfront interest works in Lendsqr

In Lendsqr, upfront interest is configured as a loan product attribute.

Once enabled:

The system calculates the interest on the loan

The interest is deducted at disbursement

The borrower receives the net loan amount

Repayment focuses primarily on the principal

This allows lenders to automate interest collection without manual adjustments.

This feature helps reduce the risk associated with loan repayments by ensuring that the interest is settled in advance. This guide will walk you through the steps to configure this feature on your loan product using the Lendsqr admin console.

Before you begin

Make sure the loan product you want to configure is already created in your Lendsqr admin console. You will also need admin-level access to edit product attributes.

How to enable upfront interest on Lendsqr

1. Login to the Admin Console 2. Go to Product Management in the left navigation, then click Loan Products.

3. Select the loan product you want to configure. If you need to create a new one first, click Create.

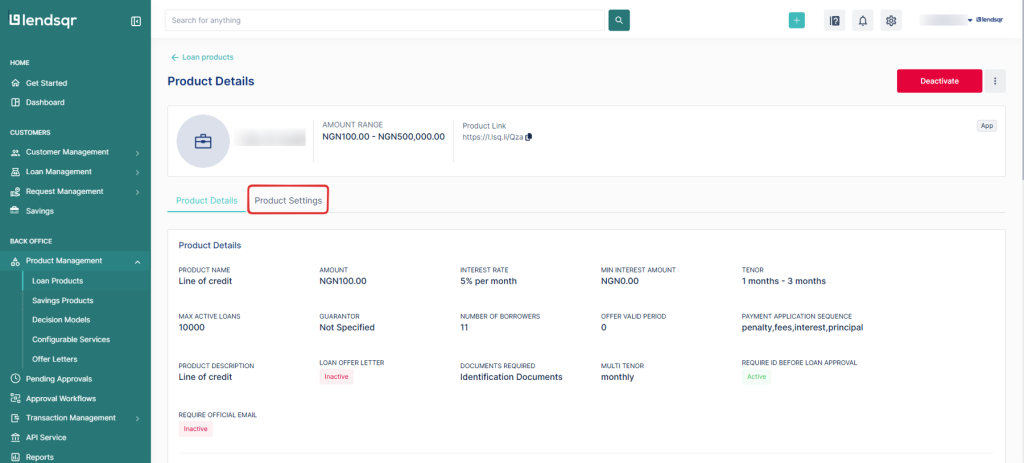

4. Click the Product Settings tab on the product page.

5. Scroll to find the Upfront Interest Payment attribute. Click the three-dot menu beside it and select Edit.

6. Check the box next to Upfront Interest Payment to set it to true. Click Save to apply the change.

Note: This setting applies to all new loans booked under this product going forward. Existing active loans are not affected.

What borrowers will see

When a borrower applies for a loan product with upfront interest enabled, they will see a breakdown showing the loan amount, the interest deducted at disbursement, and the net amount they will receive. This transparency is important — make sure your offer letter or loan agreement reflects it clearly.

Frequently asked questions

Does upfront interest work with all repayment frequencies?

Yes. Upfront interest is a product-level attribute and is independent of whether repayments are daily, weekly, or monthly. The interest is simply collected before disbursement, and the repayment schedule covers the remaining principal.

Can I use upfront interest alongside other fees?

Yes. Upfront interest works alongside other configured fees such as processing fees or management charges. Each is calculated and deducted separately at disbursement. Review your fee configuration to ensure borrowers are not over-charged.

Is upfront interest legal in my country?

Regulations around upfront interest vary by jurisdiction. In some countries, regulators require that the effective interest rate be disclosed clearly to borrowers. Always verify compliance with your local lending regulations before enabling this feature.

feature")