Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

Identifying bad actors through blacklisting on Lendsqr’s Karma database

Updated

On this page

Identifying bad actors using Lendsqr Karma

In lending, one of the most critical responsibilities is ensuring that credit is extended to the right customers. While many borrowers are genuine, some intentionally default on loans, commit fraud, or repeatedly exploit lending systems. These individuals are referred to as bad actors.

Lendsqr’s Karma system is designed to help lenders identify and manage such individuals effectively. By leveraging shared data across the ecosystem, Karma enables lenders to detect high-risk borrowers early and prevent avoidable losses.

This guide explains what bad actors are, why identifying them is important, how to use the Karma feature within your dashboard, and the governance considerations required when adding or searching records.

What are bad actors

Bad actors are individuals with a history of fraudulent activity, loan defaults, or behavior indicating a high likelihood of non-repayment.

These may include:

Borrowers who deliberately take loans without the intention to repay

Individuals who use false or inconsistent identity information

Customers who repeatedly default across multiple lenders

Users who attempt to exploit system loopholes

Bad actors are typically flagged and recorded in shared systems like Karma, which serves as Lendsqr’s blacklist database. This allows lenders to identify high-risk individuals across different platforms.

Why identifying bad actors is important

Identifying bad actors early helps protect your lending business from financial losses and operational inefficiencies.

When bad actors are not properly filtered:

Default rates increase

Recovery costs rise

Operational resources are wasted on high-risk users

Overall portfolio quality declines

By using tools like Karma, lenders can make more informed decisions, reduce exposure to risky borrowers, and maintain a healthier loan portfolio.

Understanding the karma (blacklist) feature in lendsqr

Karma is a system-level feature that allows lenders to record and access data about bad actors.

It functions as both:

A blacklist database where lenders can report verified risky users

A search system that allows lenders to check if a borrower has been flagged by other organizations

This shared intelligence strengthens fraud prevention and helps lenders make faster, more accurate decisions.

Identity types explained

When adding or searching for a Karma record, you will be required to provide an identity type. These identifiers help uniquely match individuals across systems.

Common identity types include:

BVN (Bank Verification Number): A unique identifier issued by Nigerian banks used to verify identity across financial institutions

Phone number: Often used as a primary contact and identity signal

Email address: Useful for detecting repeat usage across platforms

IP address: Helps identify suspicious patterns or device-level activity

Always ensure that identity data is accurate and verified before use.

Access and permission requirements

Not all users within your organization may have permission to add or manage Karma entries.

You should confirm with a super admin or system administrator which roles are authorized to:

Add a user to Karma

Search external Karma records

Edit or review existing entries

This ensures proper governance and prevents misuse of the blacklist system.

All actions related to Karma entries should be traceable through internal audit logs, allowing organizations to review who added or modified a record and when.

Step by step guide to adding a customer to karma

Adding a Karma entry allows your organization to flag a user as a bad actor based on verified behavior such as fraud or loan default.

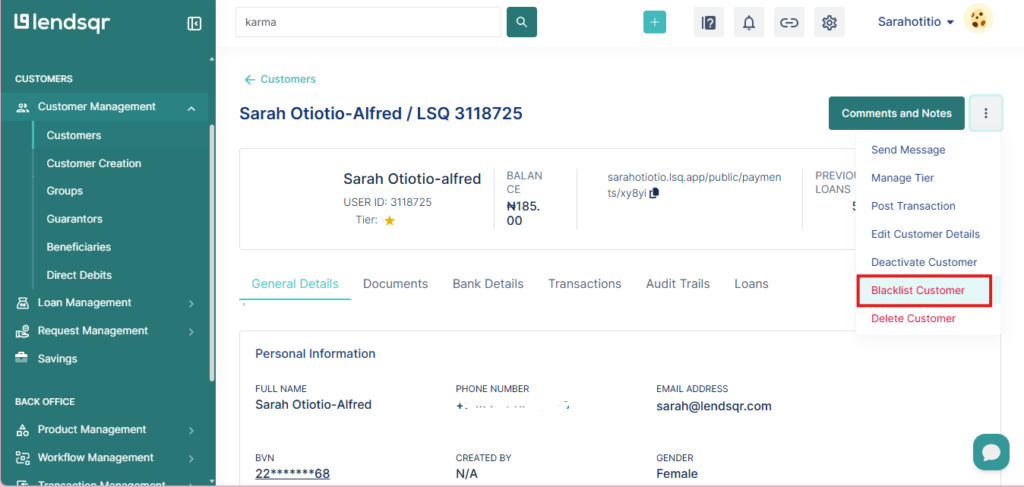

Step 1: Access the blacklist option from the customer profile

Navigate to the Customers page and select the specific customer you want to blacklist.

On the customer’s profile, click the three-dot menu located on the right-hand side. From the dropdown options, select the blacklist option.

This action opens a modal where you can enter the details of the Karma entry.

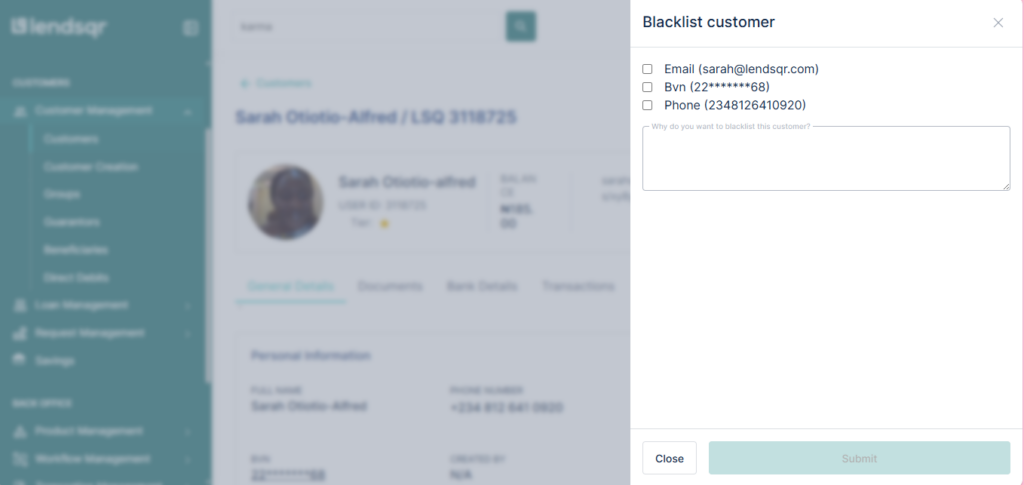

Step 2: Enter the identity details

Provide the identity of the individual you are flagging.

This could be a BVN, phone number, email address, or another supported identifier. Ensure that this information has been verified before proceeding.

Step 3: Select the identity type

Specify the type of identity you entered.

For example, if you provided a BVN, select BVN as the identity type. This ensures accurate categorization and improves searchability.

Step 4: Define the karma type

Indicate the reason for adding the Karma entry.

This could be related to loan default or fraudulent activity. Selecting the correct type ensures that other lenders understand the context of the record.

Step 5: Provide supporting details

Where applicable, include relevant supporting information such as:

Amount involved in the default or fraud

Date of occurrence

Internal notes or references

These details improve the quality and usefulness of the record.

Step 6: Submit and save

After filling in all required fields, submit the form.

The Karma entry will be added to your organization’s Karma list and may become visible to other lenders depending on system configuration.

Searching for karma records

Lendsqr allows you to search for Karma entries to verify whether a borrower has been flagged as a bad actor.

There are two main approaches.

Searching within your organization’s records

On the Karma page, you will see a table containing all entries added by your organization.

You can filter this table using parameters such as date and karma type. This is useful for internal tracking and audits.

Searching across the broader ecosystem

You can also search for Karma entries added by other lenders.

Use the search box located on the right side of the Karma page and enter the identity you want to check.

If the identity exists in the broader Karma system, the result will indicate whether it has been flagged.

To perform external searches, your virtual account must be funded. Each search incurs a fee, which is calculated per query. Ensure that you review current pricing and maintain sufficient balance before initiating searches.

Visibility and data sharing considerations

When you add a Karma entry, it contributes to a shared ecosystem of risk data.

However, visibility of this data may depend on system configurations and permissions. Other lenders may be able to see that an identity has been flagged, along with limited contextual information.

You should ensure that any data shared complies with applicable data protection and privacy regulations. Only verified and necessary information should be recorded.

Real-life scenarios

A borrower applies for a loan using a phone number that has previously been reported for fraud by another lender. When you search this number in Karma, you find a match and avoid approving a high-risk loan.

Another example is a customer who defaulted on a loan within your organization. By adding them to Karma, you ensure that other lenders are aware of this behavior, contributing to a safer lending ecosystem.

Editing, removal, and appeals

There may be situations where a Karma entry needs to be reviewed, updated, or removed.

If a borrower disputes a Karma record, you should:

Review internal records and supporting evidence

Confirm whether the entry was accurate at the time of submission

Update or remove the entry if it is found to be incorrect

Organizations should define internal workflows for handling such appeals to ensure fairness and accuracy.

Common errors and how to fix them

One common issue is entering incorrect identity details when adding a Karma entry. This reduces the effectiveness of the record. Always verify identity data before submission.

Another issue is selecting the wrong identity type. Ensure that the identity type matches the data provided.

Users may also attempt to search external Karma records without sufficient funds. Ensure your virtual account is funded before performing paid searches.

Failure to include supporting context such as amount or date can reduce the usefulness of a Karma entry. Always provide complete and accurate information.

Best practices for using karma

Only add Karma entries for verified cases of fraud or default. Avoid adding users based on assumptions or incomplete evidence.

Use multiple identity types where possible to improve traceability across systems.

Regularly search Karma before approving loans to identify risks early.

Maintain proper internal documentation for each entry to support audits and dispute resolution.

Ensure that all usage of Karma complies with data protection and regulatory requirements.

Conclusion

Identifying bad actors is a critical part of building a sustainable lending business. Lendsqr’s Karma feature provides a structured and collaborative way to detect, record, and share information about high-risk borrowers.

By understanding how to correctly add and search Karma entries, implementing proper governance, and following best practices, lenders can significantly reduce exposure to fraud and defaults.

Using Karma effectively not only protects your organization but also contributes to a more secure and reliable lending ecosystem overall.