Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

How to view users’ general details

Updated

On this page

Introduction

When managing customers on Lendsqr, making well informed lending decisions requires more than just surface level data. It is essential to understand who the customer is, how they earn, and what level of risk they may present. The platform provides a structured way to access this information through the user profile page, where key data points are grouped into clearly defined sections.

One of the most important sections on a user’s profile is the General Details tab. This section offers a concise but comprehensive snapshot of a customer’s identity, financial background, and support network. By reviewing this information carefully, lenders can build a clearer picture of the customer’s credibility and repayment capacity before approving any loan request.

Why general details matter to lenders

Viewing a user’s general details is central to three key lending functions: risk assessment, customer servicing, and regulatory compliance.

From a risk perspective, general details help lenders evaluate whether a borrower is likely to repay. Income, employment status, and guarantor strength all contribute to a clearer understanding of repayment capacity and default risk.

For customer servicing, accurate personal and contact information ensures that borrowers can be reached easily for onboarding, repayment reminders, or issue resolution. This reduces friction and improves the overall lending experience.

From a compliance standpoint, general details support Know Your Customer (KYC) requirements. Verifying identity, contact details, and supporting relationships such as next of kin helps ensure that the lender is dealing with a legitimate and traceable individual, which is critical for fraud prevention and regulatory adherence.

What general details are and why they matter

General details refer to the core background information about a customer that helps lenders understand their identity, financial position, and level of reliability. These details combine personal data, employment information, and support structures such as guarantors and next of kin into a single, accessible view.

Lenders rely on general details because they form the foundation of decision making. Without them, it is difficult to verify identity, assess repayment ability, or determine the level of risk associated with a loan.

When checking general details is necessary

Reviewing general details is important at multiple stages of the lending lifecycle.

A common scenario is during loan approval. For example, a credit officer reviewing an application may notice that a borrower’s monthly income appears sufficient. However, upon checking the General Details tab, the officer discovers that the borrower is self employed with irregular income and has no guarantors listed. Based on this, the officer may reduce the loan amount or request additional documentation.

Another scenario occurs during collections. If a borrower misses multiple repayments and becomes unreachable, a collections officer can use the phone number, email, next of kin, or guarantor details to initiate follow up. This improves the chances of recovery and reduces losses.

To view a customer’s general details on Lendsqr, follow these steps:

Navigate to the Customer Management section on the admin console. This is where all registered users and borrowers are listed and organized.

Click on a customer profile from the list. This action opens the user’s detailed profile page, which contains multiple tabs with different categories of information.

Select the General Details tab. This tab consolidates key background information into several subsections, making it easy to review the most relevant data at a glance.

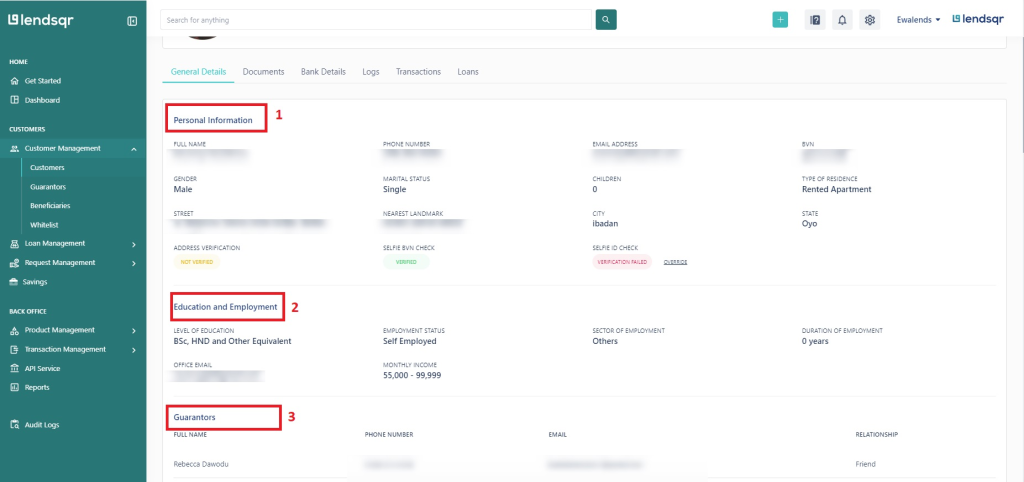

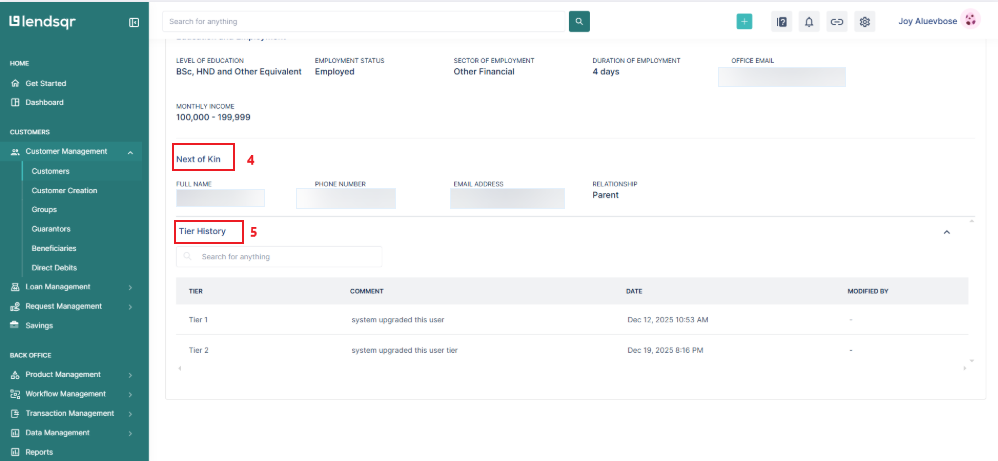

Within the General Details tab, you will find multiple subsections that collectively provide a holistic view of the customer. These include Personal Information, Education and Employment, Guarantors, Next of Kin, and Tier History. Each of these plays a distinct role in helping you assess the customer.

Personal information

The Personal Information section contains basic identity and demographic details about the customer. While these details may seem straightforward, they are essential for verification and communication.

This section typically includes:

Phone number: The customer’s primary contact number used for communication and verification.

Email address: The customer’s personal email used for notifications and account related communication.

Gender: The customer’s reported gender for identification purposes.

Marital status: Indicates whether the customer is single, married, or otherwise, providing context on financial responsibilities.

Number of children: Shows the number of dependents the customer may be financially responsible for.

The phone number and email address are particularly important for communication. They allow you to reach the customer for verification, updates, or reminders regarding their loan obligations. Consistency between these contact details and other submitted documents can also serve as an additional layer of identity validation.

Gender and marital status can sometimes provide context when evaluating household responsibilities or financial commitments. For example, a married individual with dependents may have different financial obligations compared to a single individual. Similarly, the number of children can indicate the level of financial responsibility the customer carries, which may indirectly affect their repayment capacity.

While these details should not be used in isolation to make lending decisions, they contribute to a broader understanding of the customer’s personal circumstances. When combined with financial and employment data, they help create a more complete borrower profile.

Education and employment

The Education and Employment section provides insight into the customer’s earning potential and financial stability. This is one of the most critical areas for assessing creditworthiness, as it directly relates to the borrower’s ability to repay a loan.

This section includes:

Highest level of education: The customer’s top educational qualification, which may indicate earning potential.

Employment status: Indicates whether the customer is employed, self-employed, or unemployed.

Office email: A work-related email that can help verify employment.

Monthly income: The customer’s reported earnings, used to assess repayment capacity.

The highest level of education can be an indicator of skill level and potential earning capacity. While it does not guarantee income, it can provide useful context when evaluating long-term financial prospects.

Employment status is a key factor in risk assessment. A customer with stable, full-time employment may present a lower risk than someone who is unemployed or working in a highly volatile job. Understanding whether the customer is employed, self-employed, or unemployed helps you gauge income reliability.

The office email serves as an additional verification point. A corporate email address, for instance, may help confirm the customer’s employment status. It also provides an alternative communication channel if needed.

Monthly income is perhaps the most critical data point in this section. It allows you to estimate the customer’s repayment capacity by comparing income against the proposed loan amount and repayment schedule. For example, a borrower earning a steady monthly income is more likely to meet repayment obligations than one with irregular earnings.

By analyzing these elements together, you can form a clearer picture of the customer’s financial health and determine whether they can manage additional debt.

Guarantors

The Guarantors section lists individuals who have agreed to act as financial backups for the customer’s loan. This section is particularly important in risk management, as guarantors provide an additional layer of security in case the borrower defaults.

A guarantor is typically someone who agrees to take responsibility for the loan if the borrower is unable to repay. This makes their credibility and financial stability highly relevant to your assessment.

Reviewing the guarantors linked to a customer can help you answer key questions such as:

Does the borrower have credible support in case of default?

Are the guarantors financially able to cover the loan?

Is there more than one guarantor, and what is their relationship to the borrower?

Strong guarantors can significantly reduce lending risk, especially for customers with limited credit history or lower income levels. On the other hand, weak or unverifiable guarantors may increase the overall risk of the loan.

The Next of Kin section contains information about a person who can be contacted in case of emergencies or when the customer is unreachable. While a next of kin is not financially responsible for the loan, their details play an important role in identity verification and communication.

This section includes:

Full name

Phone number

Email address

Relationship to the customer

The presence of a next of kin adds an extra layer of accountability. It helps confirm that the customer has provided traceable and verifiable personal connections. In situations where urgent communication is required, such as missed payments or account issues, the next of kin can serve as a secondary contact point.

The relationship field is also useful, as it indicates how closely connected the individual is to the borrower. A close relationship, such as a parent, sibling, or spouse, may suggest a higher likelihood of cooperation if contact is needed.

Although the next of kin is not obligated to repay the loan, their inclusion strengthens the overall reliability of the customer profile.

Tier history

The Tier History section provides a record of the customer’s progression through different verification or access levels on the platform. These tiers often reflect the extent to which a user has completed required documentation and verification processes.

This section typically shows:

The different tier levels the customer has held over time

The dates when changes occurred

The administrator or system action responsible for the upgrade

Tier levels are important because they often determine what services or loan limits a customer can access. A higher tier usually indicates that the customer has submitted more documentation and passed stricter verification checks.

By reviewing the tier history, you can assess how the customer has evolved over time. For example, a recent upgrade to a higher tier may indicate that the user has just completed additional verification steps. This could increase confidence in their profile.

You can also identify whether upgrades were system-driven or manually approved, which may provide further context for your evaluation.

If your organization requires specific documents for tier upgrades, you can configure and activate those requirements within the platform settings. Ensuring that all necessary documents are verified before approving loans helps maintain a strong risk control framework.

When reviewing general details, you may encounter incomplete, inconsistent, or suspicious information. In such cases, consider the following actions:

Edit details: If you have the appropriate permissions, correct obvious errors such as typos or outdated contact information. Ensure updates are supported by valid documentation.

Request additional documents: Ask the customer to provide missing or updated information, especially for income, employment, or identity verification.

Escalate for review: Flag the profile to a compliance or risk team if there are signs of fraud, identity mismatch, or suspicious guarantor details.

Engage guarantors or next of kin: In collections scenarios, use these contacts to re-establish communication.

Run reports: Generate internal reports to identify patterns such as multiple users sharing similar contact details or guarantors, which may indicate risk.

Adjust lending decision: Based on findings, you may approve, decline, or modify the loan terms to better reflect the customer’s risk profile.

Why the general details tab matters

The General Details tab brings together multiple dimensions of a customer’s profile into a single, easy-to-navigate view. Instead of switching between sections, you can quickly access the information you need for decision-making.

By carefully reviewing this tab, you can:

Verify the customer’s identity and contact information

Assess their financial stability and earning capacity

Evaluate the strength and reliability of their guarantors

Confirm the presence of a next of kin for additional accountability

Track their verification progress through tier history

For example, consider a customer applying for a loan with a moderate income, stable employment, and two credible guarantors. Even if their income alone might not fully support the loan amount, the presence of strong guarantors and a verified profile could make the application more acceptable.

On the other hand, a customer with incomplete personal details, unstable employment, and weak guarantors would present a higher risk, even if their requested loan amount is relatively small.

Using the ‘General Details’ tab effectively allows you to balance opportunity and risk, ensuring that lending decisions are both informed and responsible.