Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

How to update a loan schedule

Introduction

An admin can decide to update the loan schedule of a particular loan. This update can be done before loan approval and after the loan has been approved. This situation usually occurs when a lender based on a second-level review of the user’s loan application or a prior discussion with the user decides to update or vary the user’s loan schedule.

Step-by-step guide

To modify the schedule of a loan;

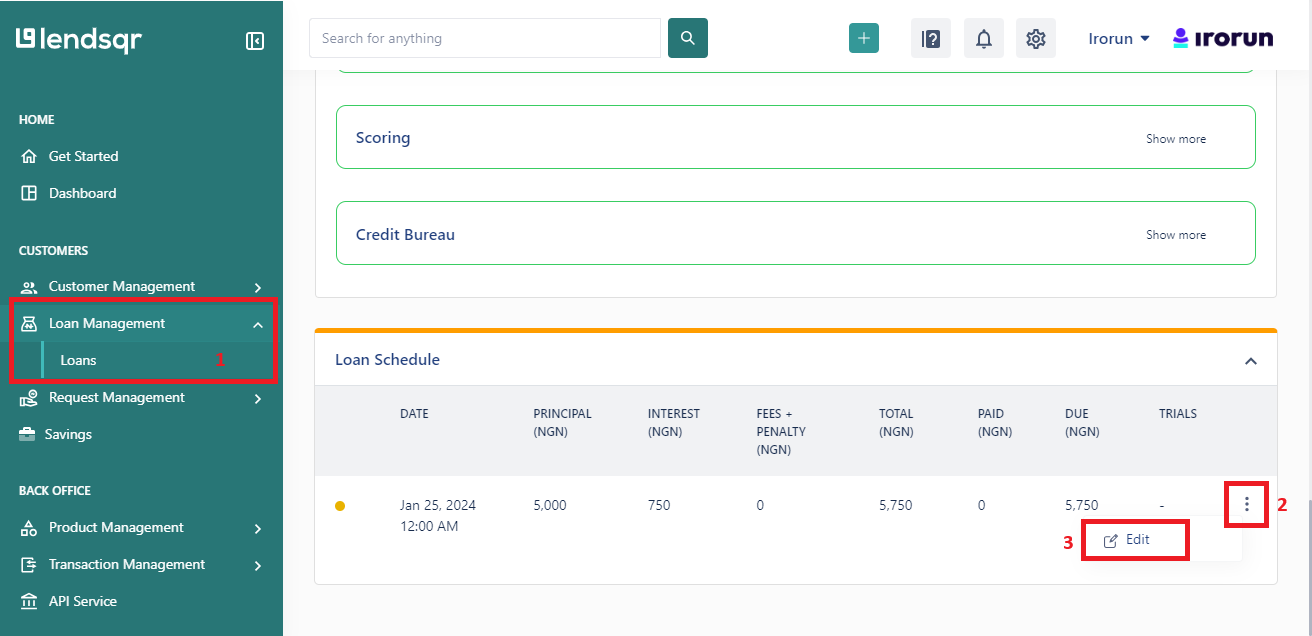

Follow the steps highlighted in the section above to locate a loan.

Similar to that of a loan request, navigate to the “Loan Schedule” segment and click on the option to edit.

Enter the desired details and select “Submit”. There are more fields such as Principal Paid, Fees Paid, etc. on this modal to account for repayments that may have been made outside the platform and how they are to be distributed.

feature")