Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

Activating a customer after manual creation

Updated

On this page

In some lending scenarios, lenders may need to manually create borrower accounts rather than relying entirely on self-registration. This often happens during assisted onboarding, offline customer acquisition, agent-led registration, enterprise partnerships, or situations where administrators need to pre-create accounts on behalf of borrowers. While manual user creation helps accelerate onboarding and improve operational flexibility, it is only the first stage in preparing a borrower account for full platform access.

After a user is manually created in Lendsqr, the borrower must complete an activation process before the account becomes fully functional. This activation process is especially important for financial operations involving third-party disbursements, bank transfers, and wallet-related transactions. Without activation, certain account functions remain unavailable, which may disrupt loan disbursement workflows and transaction success.

The activation process is intentionally structured to help confirm borrower identity, establish account ownership, and complete the setup required for secure platform interactions. By understanding how activation works and why it matters, lenders can improve onboarding outcomes while minimizing delays in loan processing.

Manual user creation allows administrators to add borrowers directly to the platform without requiring users to complete the initial registration process themselves.

This functionality is particularly useful for lenders onboarding customers through physical branches, relationship managers, call centers, field agents, or assisted digital channels. Instead of asking borrowers to independently create accounts, lenders can create profiles on their behalf and guide them through the remaining setup process.

However, manual creation alone does not fully activate the account.

Although the borrower profile exists within the system, additional actions are required before the account can support important financial activities such as wallet transactions, loan disbursements, and third-party transfers. To complete onboarding, borrowers must verify ownership of the account through activation.

This activation process ensures the platform can securely connect the borrower to the newly created account before financial operations begin.

Why account activation matters

Account activation is a critical step in enabling full borrower functionality.

Without activation, users may appear successfully created in the system but still lack access to important transactional features. This distinction becomes especially important for lenders handling loan disbursements through wallets, banks, or third-party service providers.

For example, many loan disbursement processes first route funds into a borrower’s wallet before onward transfers occur. If the borrower has not activated their account, the system may be unable to complete these financial workflows successfully.

Activation also supports identity verification and account ownership confirmation. Since manually created users are initially set up by administrators, the platform requires borrowers to establish credentials and log into the system themselves before granting full transactional access.

At an operational level, ensuring activation helps reduce failed transactions, onboarding delays, and borrower confusion.

How the activation process works

The activation process for manually created users follows a structured sequence designed to move borrowers from account creation to full platform access.

Each stage builds upon the previous step and contributes to successful account setup.

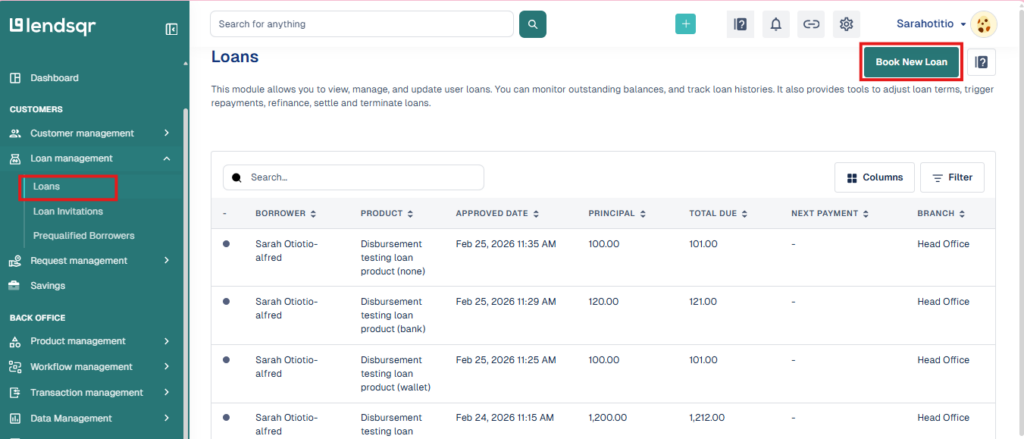

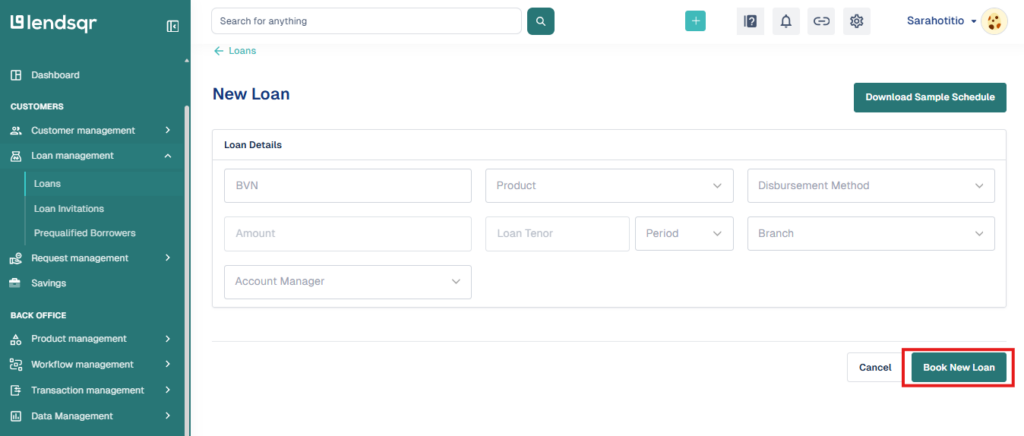

Step 1: Manually book a new loan

To manually book a loan, navigate to the Loans section under Loan Management. Then, select the Book New Loan option.

You will be able to manually enter the customer’s details for whom you are booking the loan.

Step 2: SMS notification for password reset

Once a borrower is manually created on the platform, the system automatically sends an SMS notification containing password reset instructions.

This SMS includes a link directing the borrower to the web application where they can create a password and begin account setup.

The message acts as the borrower’s first point of interaction with the newly created account and provides clear guidance on how to proceed.

A sample notification may appear as follows:

Sample: [BGL Limite.] Hello Theresa, you have been created as a customer with us. Reset password to log in at bgl.lsq.app.

Because the activation process depends on this communication, lenders should encourage borrowers to review incoming SMS messages carefully and confirm receipt where necessary.

It is also helpful for lenders to verify that the correct phone number was entered during manual account creation to avoid onboarding delays.

Step 2: Password reset and login

After receiving the SMS, the borrower must follow the provided link to reset their password.

This step allows the user to establish secure login credentials associated with the account. Since administrators initially create the borrower profile, password setup helps transfer account control securely to the borrower.

Once the password reset is completed successfully, the borrower can log into the platform using newly created credentials.

This login step is more than a basic access requirement. It signals that the borrower has engaged with the account directly and confirms ownership of the registration details.

Lenders should communicate the importance of this step clearly to avoid situations where borrowers assume account creation alone means onboarding is complete.

Step 3: Account activation

After successfully resetting the password and logging into the account, the borrower’s account becomes officially activated.

This stage completes the onboarding process and enables the borrower to access platform features requiring account validation.

Activation is important because it allows the system to finalize identity verification and establish the operational readiness of the borrower profile.

Once activated, the account can support wallet functionality, transaction processing, and loan disbursement workflows that were previously unavailable.

Without activation, financial operations involving wallet-based flows may fail or remain incomplete.

Why activation is essential for loan operations

One of the most important reasons borrowers must activate manually created accounts relates to loan disbursement functionality.

Many loan repayment and disbursement systems within Lendsqr involve wallet-based infrastructure. Before funds move externally to banks, merchants, or service providers, transactions may first pass through the borrower’s wallet.

If the borrower has not completed account activation, the wallet may remain unavailable for processing.

Loan disbursements

For loans involving third-party disbursements or bank transfers, activation is necessary because the system first impacts the borrower’s wallet before moving funds elsewhere.

Without activation, the wallet may not function correctly, which can interrupt loan processing and delay borrower access to funds.

For lenders managing high transaction volumes, inactive accounts may create avoidable operational bottlenecks if borrowers are not guided through activation early.

Transaction success

Activation is equally important for ensuring successful transaction flows.

When users have not completed setup, loan funds may be unable to move properly between the borrower wallet and external destinations such as banks, vendors, or service providers.

This issue can create confusion for both lenders and borrowers, particularly when loan approval has already been completed but funds remain undisbursed due to activation delays.

Encouraging borrowers to activate accounts immediately after manual creation helps improve transaction success rates and reduces operational friction.

Common mistakes to avoid during manual onboarding

Although manual user creation simplifies borrower onboarding, some avoidable mistakes may slow down activation.

One common issue is assuming account creation automatically enables transactional functionality. In reality, borrowers must complete password reset and login before activation occurs.

Another mistake involves failing to confirm borrower contact details during setup. Incorrect phone numbers may prevent users from receiving password reset instructions, delaying onboarding and loan disbursement.

Lenders should also avoid waiting until loan approval before discussing activation requirements. Proactively communicating next steps immediately after account creation improves borrower readiness and reduces delays later in the lending process.

Finally, administrators should avoid overlooking activation status before processing sensitive financial operations.

The most effective lenders treat activation as an essential onboarding milestone rather than an optional follow-up step.

Organizations should educate borrowers about activation requirements immediately after manual account creation. Providing clear instructions on password reset and login steps helps reduce confusion and support requests.

Monitoring activation completion rates may also help lenders identify bottlenecks within onboarding workflows.

Some organizations additionally establish internal follow-up processes to remind borrowers who have not completed activation within a specific timeframe.

As lending operations become increasingly digital, smooth onboarding processes play an important role in transaction success and borrower satisfaction. Manual user creation provides flexibility for lenders, but activation remains necessary to unlock full account functionality.

By ensuring borrowers complete password resets, log into their accounts, and finalize activation promptly, lenders can improve disbursement reliability, reduce failed transactions, and create a smoother borrower experience from the start.