Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

How do I create a new credit risk rule?

Updated

On this page

Every new Lendsqr account comes with a sample credit risk rule, designed to support common retail lending needs. This default setup helps lenders get started quickly by providing a ready-made framework for evaluating borrower eligibility and automating loan decisions.

However, lending businesses often have unique risk requirements, customer profiles, and operational goals. To meet these specific needs, Lendsqr allows lenders to create and customize their own credit risk rules.

Whether you are lending to salary earners, gig workers, cooperative members, or small business owners, custom credit risk rules help you standardize decisions, improve risk control, and align lending outcomes with your business objectives.

Also read: How we built Oraculi to help lenders make informed decision

What are credit risk rules?

Credit risk rules are the conditions and evaluation logic used to determine whether a borrower qualifies for a loan.

These rules help automate loan decisions by assessing borrower information against predefined criteria such as repayment history, loan exposure, income level, account activity, and other risk indicators.

Rather than reviewing every application manually, lenders can configure rules that automatically determine eligibility based on their preferred lending standards.

For example, a lender may define a rule such as:

Approve loans below $200 for applicants with no outstanding loans and a monthly income above $500.

In this scenario, borrowers who meet the requirements would qualify automatically, while borrowers who fall outside the conditions may be restricted or reviewed further.

This creates more consistent lending outcomes and reduces dependency on manual underwriting.

Why custom credit risk rules matter

Every lender has a different appetite for risk.

Some lenders may prioritize growth and faster loan approvals, while others may focus more heavily on minimizing defaults and protecting portfolio quality.

Custom credit risk rules allow lenders to reflect these priorities within their lending process.

For example, a lender serving first-time borrowers may configure stricter requirements around repayment behavior and identity verification. Meanwhile, a lender focused on repeat customers may prioritize historical repayment performance and loyalty.

By creating rules tailored to their business model, lenders can improve approval quality and reduce exposure to high-risk borrowers.

Custom rules also help reduce fraud, improve operational efficiency, and ensure consistent treatment of borrowers across all loan applications.

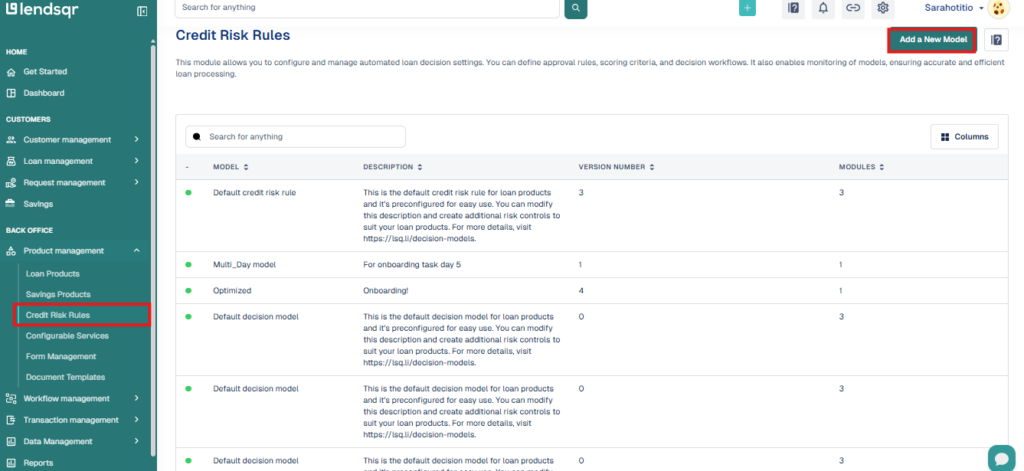

Ways to create a new credit risk rule

Lendsqr provides two methods for creating a new credit risk rule depending on your preference and level of customization required.

Clone an existing credit risk rule

The fastest and most efficient way to create a new rule is by cloning an existing one.

This approach allows lenders to duplicate an already configured credit risk rule and make adjustments instead of starting from scratch.

For example, a lender may already have a rule configured for salary earners but wants to create a slightly different version for self-employed borrowers.

Instead of rebuilding the logic entirely, the lender can clone the existing setup and adjust only the necessary parameters, such as income verification rules, exposure limits, or repayment thresholds.

This saves time, maintains consistency, and reduces the risk of configuration errors.

Because Lendsqr credit risk rules are highly configurable and contain numerous evaluation settings, cloning is often the preferred approach for most lenders.

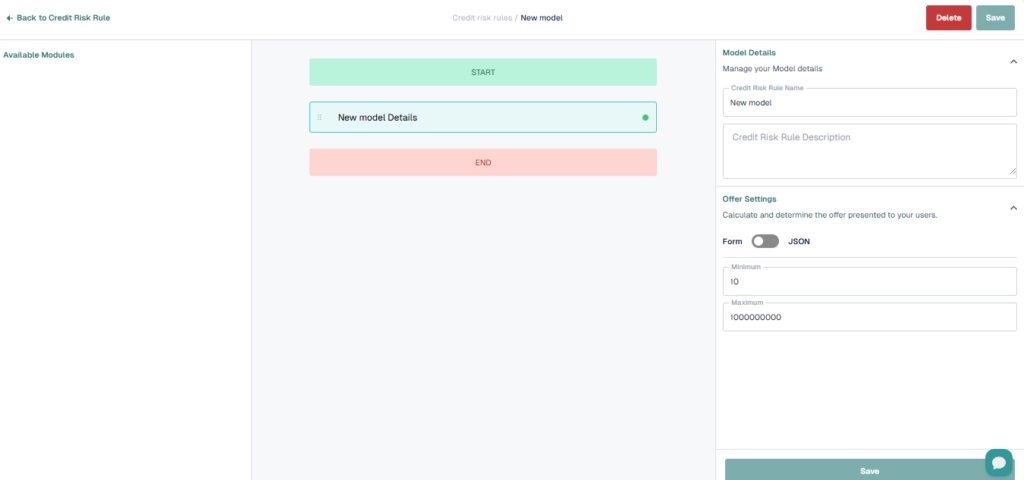

This option is ideal when creating an entirely new lending strategy or serving a borrower segment with significantly different requirements.

For example, a lender launching a new nano-loan product may want to create a rule focused on transaction activity and behavioral scoring rather than traditional employment verification.

Starting from scratch gives lenders complete flexibility to define approval logic according to their specific needs.

However, because credit risk rules contain numerous configurable parameters, this method typically requires a clearer understanding of risk strategy and operational requirements.

Why cloning is often the better option

Lendsqr credit risk rules are highly powerful and support extensive customization across multiple decision points.

With over 100 configurable parameters, building a completely new rule can become complex, especially for lenders who are still refining their credit processes.

Cloning an existing rule provides a strong foundation while reducing setup time and minimizing unnecessary configuration work.

It also helps lenders maintain consistency between loan products while still allowing room for experimentation and optimization.

For example, lenders can test slight variations in approval logic by cloning a rule and modifying only specific thresholds instead of redesigning the full structure.

This approach supports faster iteration and more controlled lending strategy updates.

Benefits of custom credit risk rules

More consistent lending decisions

Configured rules ensure borrowers are evaluated against the same standards every time. This reduces inconsistencies caused by manual review and improves fairness in loan approvals.

Better risk management

Custom rules help lenders define exactly who qualifies for credit based on business goals and portfolio performance targets. This reduces unnecessary risk exposure and supports healthier lending outcomes.

Improved operational efficiency

Automation reduces manual underwriting workload, allowing internal teams to focus on complex or exceptional loan cases. This leads to faster approval times and improved customer experience.

Greater flexibility

Lenders can continuously refine rules as borrower behavior, regulations, or business priorities evolve. This makes lending operations more adaptive and scalable over time.

Lendsqr’s credit risk rules give lenders the flexibility to automate loan decisions according to their unique risk appetite and business goals. Whether you choose to clone an existing rule or create one from scratch, the platform provides the tools needed to design structured, scalable, and consistent lending workflows.

For most lenders, cloning an existing credit risk rule and fine-tuning it offers the fastest and most efficient way to create a tailored lending strategy while maintaining strong risk controls.