Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

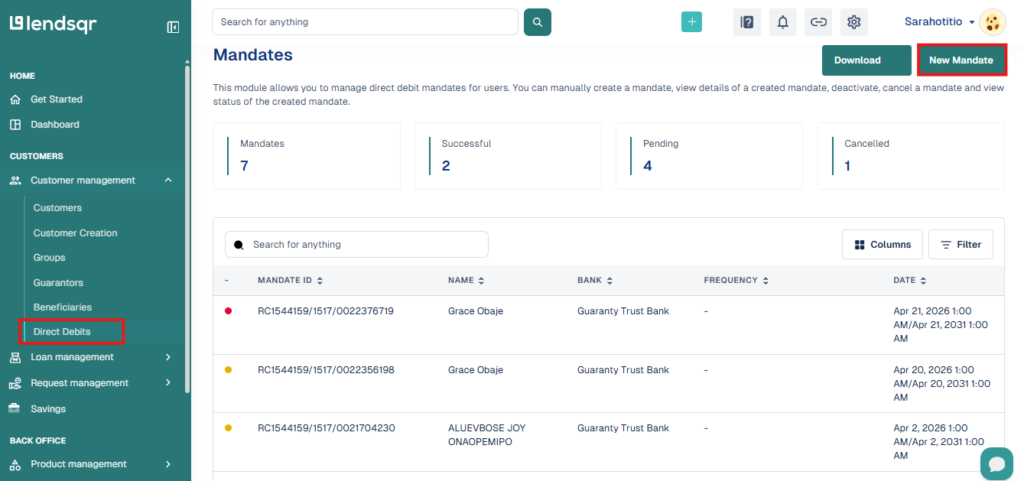

How to create a direct debit mandate

Updated

On this page

In lending, repayment consistency is essential for maintaining portfolio health and reducing default risks. While many borrowers repay loans successfully using cards, transfers, or wallet-based methods, repayment interruptions can occur when cards expire, payment methods fail, or borrowers intentionally disable repayment channels. To reduce these challenges, lenders often rely on Direct Debit as a more structured repayment mechanism.

A Direct Debit is a payment method where a customer’s account is authorized through a mandate. This authorization allows lenders to debit repayments directly from the borrower’s bank account according to agreed repayment schedules. Because repayments are linked directly to a customer’s bank account, Direct Debit can improve repayment reliability and help lenders recover funds even in situations where borrowers block cards or stop using linked payment methods.

When dealing with defaulting customers, Direct Debit becomes particularly useful because repayments are deducted directly from bank accounts instead of relying solely on debit cards. This creates a more dependable repayment method and helps lenders maintain better control over collections.

Within Lendsqr, lenders are also able to create Direct Debit mandates to collect funds for loans booked outside the Lendsqr ecosystem. This means organizations can centralize repayment management through the Lendsqr Admin Console, even when loans originated elsewhere.

A Direct Debit mandate is an authorization granted by a borrower that permits a lender to debit repayments directly from the customer’s bank account.

The mandate serves as formal approval for recurring deductions according to agreed loan terms.

Unlike card-based repayment methods, which may fail due to expired cards, insufficient balances, or blocked payment channels, Direct Debit offers greater repayment continuity because deductions happen directly from the borrower’s bank account.

For lenders, this repayment structure improves collection efficiency and reduces dependence on manual repayment follow-ups. Borrowers also benefit from a more seamless repayment process since scheduled deductions occur automatically.

However, because Direct Debit involves access to a borrower’s bank account, mandates must be set up carefully and with the correct authorization process.

Why Direct Debit matters for lenders

Managing repayment reliability is one of the most important parts of maintaining a healthy lending portfolio.

When borrowers delay payments or intentionally avoid repayments, lenders may face operational challenges, increased collection costs, and rising default risks.

Direct Debit helps reduce these challenges by providing a repayment mechanism that continues functioning even when borrowers block or stop using debit cards.

For example, some defaulting customers intentionally disable card payments after loan disbursement to avoid automatic collections. In these situations, card-based repayment systems may become ineffective.

Since Direct Debit pulls funds directly from a bank account, lenders have a more dependable repayment pathway when mandates have already been approved.

Another important advantage is automation. Direct Debit reduces manual repayment tracking and minimizes operational effort for collections teams.

For lenders managing high borrower volumes, this automation can improve repayment efficiency significantly.

Creating mandates for loans outside the Lendsqr ecosystem

Lendsqr allows lenders to create mandates for customer accounts even when loans were booked outside the platform.

This functionality helps lenders centralize repayment management without requiring every loan to originate directly within the Lendsqr ecosystem.

For example, a lender may have historical loans managed through another system before migrating to Lendsqr. Instead of managing repayments separately, administrators can create Direct Debit mandates within the admin console and maintain repayment visibility in one place.

This flexibility helps organizations improve operational efficiency while maintaining repayment consistency across portfolios.

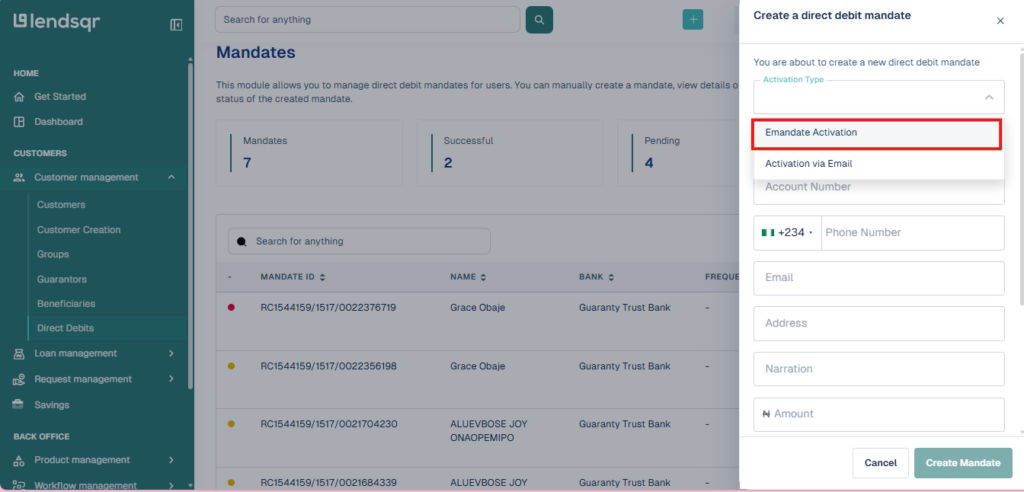

Understanding mandate activation types

Before repayments can begin through Direct Debit, lenders must activate a mandate.

The mandate activation type determines how borrower authorization is completed and validated.

Within the Lendsqr Admin Console, lenders can choose different activation methods depending on operational needs.

For this guide, the selected option is Emandate Activation.

Emandate activation allows lenders to digitally authorize repayment mandates, helping simplify setup and improve borrower onboarding efficiency.

Ensuring the correct activation method is selected is important because repayment processing depends on successful authorization.

Things to confirm before creating a mandate

Before setting up a Direct Debit mandate, lenders should confirm several important details.

First, borrower information should be reviewed carefully. Since deductions will occur from a bank account, accurate account details are essential for successful mandate setup.

Lenders should also ensure borrowers understand repayment expectations and mandate authorization. Clear communication reduces misunderstandings and helps borrowers understand how repayments will be collected.

It is also important to confirm that the chosen mandate activation type aligns with internal operational processes.

Reviewing these details beforehand helps reduce failed setups and repayment disruptions.

How to create a Direct Debit mandate in Lendsqr

Creating a mandate within the Lendsqr Admin Console follows a straightforward process.

Although mandate creation is relatively simple, some mistakes may affect repayment success.

One common issue is entering incorrect borrower or banking information. Even small errors may delay authorization or prevent mandate setup entirely.

Another mistake involves selecting the wrong activation type. Since repayment processing depends on proper authorization, lenders should confirm the selected option aligns with organizational requirements.

Lenders should also avoid creating mandates without borrower understanding. Clearly communicating repayment expectations helps reduce disputes and improves customer trust.

Finally, administrators should always verify successful mandate creation before relying on Direct Debit for repayment collection.

Best practices for managing Direct Debit mandates

Successful lenders treat Direct Debit as part of a broader repayment strategy.

Organizations should maintain clear communication during mandate setup and ensure borrowers understand repayment schedules and authorization terms.

Regularly reviewing mandate performance may also help identify failed authorizations or repayment disruptions early.

Keeping repayment records organized within the admin console further improves visibility and supports operational oversight.

As lending becomes increasingly digital, repayment reliability becomes even more important for maintaining healthy portfolios. Direct Debit provides lenders with a practical way to automate collections, reduce repayment failures, and improve operational efficiency.

By following the correct steps to create mandates in Lendsqr and ensuring borrowers are properly authorized, lenders can strengthen repayment consistency while maintaining greater control over collections management.