Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

What are the payment methods on Lendsqr?

Updated

On this page

A borrower gets approved for a loan. The funds hit their wallet. Two weeks later, repayment is due. What happens next depends entirely on the payment method your loan product is configured to use.

If the method does not match how your borrowers manage their money, collections become a problem. Borrowers miss payments not because they cannot afford to repay, but because the repayment process creates friction they were not prepared for. The result is avoidable defaults, strained borrower relationships, and a collections team chasing payments that a better-configured system would have captured automatically.

Lendsqr gives lenders three repayment methods: card payments, direct debit, and virtual accounts. This article explains how each one works, when to use it, and how to configure the repayment method on your loan product.

Why your repayment method choice matters

The payment method on a loan product is not just a technical setting. It is a collection strategy decision.

A lender offering salary advance loans to urban workers needs a fast, low-friction method that collects automatically when payday arrives. For higher-value business loans, something harder for borrowers to cancel is the better fit. When borrowers are more comfortable with bank transfers than digital cards, the right method aligns with that behavior.

Getting this wrong increases default risk, adds collections overhead to your team, and creates unnecessary friction for borrowers. Getting it right means the system collects most repayments automatically and your team focuses only on genuine exceptions.

Card payments

Card payments are the default repayment method for all Lendsqr lenders. During the loan application process, borrowers link a debit card. When a repayment falls due, the platform’s automated collection engine charges the card directly.

How borrowers experience it: The borrower adds their card once during onboarding. Repayments are made automatically on the scheduled date, with no further action required from them. Most borrowers find this straightforward, especially those accustomed to subscription services that operate similarly.

Best for: Short-term, lower-value consumer loans where speed of setup matters and borrowers are digitally active. Card payments are fast to activate and have no delay between loan approval and repayment readiness.

The limitation: Borrowers can block or deactivate a card through their bank at any time. A borrower in financial difficulty often does this early, which can disrupt automatic collections and require manual follow-up from your team. For higher-value loans, consider pairing card payments with direct debit to give your collection engine a second channel.

Direct debit lets borrowers authorize your platform to collect repayments directly from their bank account on scheduled dates. The authorization uses a mandate, which is a formal agreement between borrower and lender specifying the collection amount and duration.

On Lendsqr, direct debit is powered primarily by NIBSS.

Through NIBSS: The process is fully digital. After providing bank details, the borrower receives a link to authorize the mandate electronically using their signature. This requires no bank visit on the part of the customer.

How borrowers experience it: Direct debit feels more like a standing instruction than an active payment. Repayments leave the account automatically on the scheduled date without the borrower needing to do anything after the mandate is active.

Best for: Higher-value loans, salary-backed products, and any situation where repayment reliability is critical. A direct debit mandate is significantly harder for borrowers to cancel than a card block. Disabling it requires deliberate action at the bank level, making it a more durable collection mechanism.

The limitation: Mandate activation can take a few hours to 48 hours, depending on the provider and the borrower’s bank. For borrowers who need funds urgently, this setup time can feel like a barrier during the application process.

Virtual accounts give each borrower a dedicated account number on the Lendsqr platform. This account receives loan disbursements when a loan is approved and is also where the borrower transfers repayments when they are due. On the repayment date, Lendsqr automatically deducts the scheduled amount from the virtual account balance.

How borrowers experience it: The borrower knows their virtual account number and transfers the repayment amount before the due date, just like a regular bank transfer. This is familiar to most borrowers in African markets who regularly use bank transfers for everyday payments.

Best for: Borrowers who prefer to manage their own repayment timing through bank transfers, and for lending models where manual repayment is expected. This works well when borrowers are disciplined about their own payment schedules.

The limitation: This method depends on the borrower taking action. A borrower who forgets to transfer on time, sends the wrong amount, or delays the payment creates a gap that your collections team needs to follow up on. For lenders with large borrower bases, this dependency adds operational overhead compared to fully automated collection methods.

How to configure the repayment method on a loan product

The repayment method is set at the loan product level in the admin console. Each loan product can have its own configured method. Here are the steps for configuring the repayment method on your loan product:

Log in to the Lendsqr admin console. Navigate to the “Product Management” tab in the left sidebar and select “Loan Products.”

Find the loan product you want to configure and click on it to open the product page. On the loan product page, click “Product Settings.”

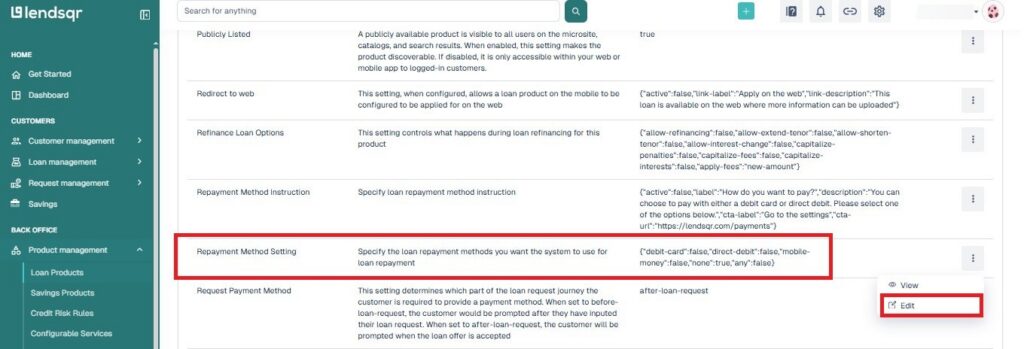

In the settings list, locate “Repayment Method Setting.” Click the “More Options” icon next to it and select “Edit.”

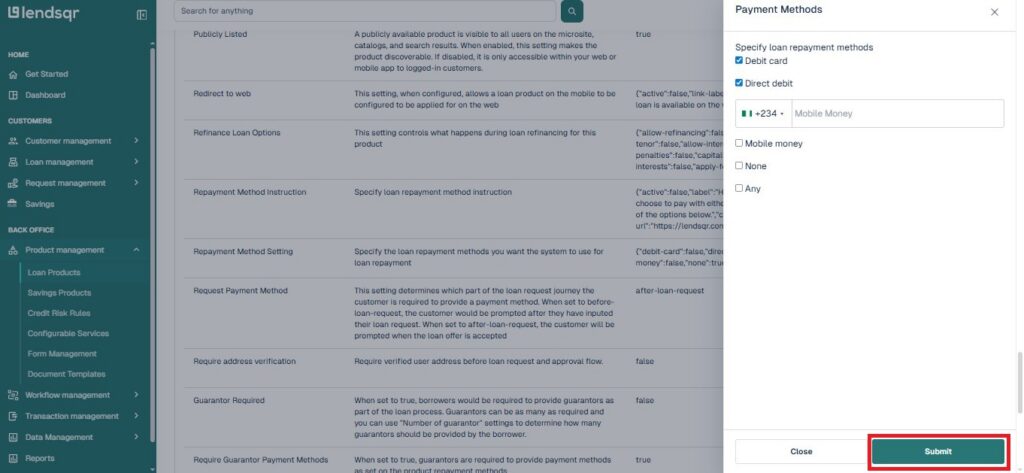

Select your preferred repayment method from the available options and click “Submit.”

The change applies to all new loans created under this product from that point forward. Existing active loans continue to use whatever method was in place when they were issued.

Choosing the right method for your loan products

Card payments work best for short-term, lower-value consumer loans where speed and simplicity matter and borrowers are digitally active.

Direct debit is the stronger choice for higher-value loans, salary-backed products, or any situation where repayment reliability is critical. Many lenders configure both card payments and direct debit on higher-value products to give the collection engine two channels to use.

Virtual accounts suit lending models where borrowers are more comfortable with traditional bank transfers and where some manual repayment management is acceptable.

Can I enable more than one payment method on the same loan product? Yes. You can configure both card payments and direct debit on a single loan product. Lendsqr’s collection engine will use whichever method is available and active on the borrower’s profile.

Is direct debit available for lenders outside Nigeria? Direct debit via NIBSS and Remita is currently available for Nigerian lenders. For lenders in other markets, contact Lendsqr support to understand which collection providers are available in your region.

What happens if a borrower’s virtual account balance is insufficient on the repayment date? If the balance in the virtual account is below the repayment amount on the due date, the automatic deduction will not complete. Your collections team will need to follow up with the borrower to ensure the correct amount is transferred before the next collection attempt.

How do I set direct debit as the repayment method for a loan product? Navigate to the loan product settings on your admin console, go to the Repayment Methods section, and select direct debit. For a step-by-step guide, see: How to set direct debit as a loan repayment method.