Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

Understanding credit life insurance on Lendsqr

Updated

On this page

A borrower takes out a ₦300,000 loan to fund a small business. Three months in, he passes away unexpectedly. The loan is still active. His family has no obligation to repay it, but without a recovery mechanism, that outstanding balance becomes a loss on your books.

Credit life insurance exists to cover exactly this kind of situation. When a borrower cannot repay due to death, permanent disability, or job loss, the insurance policy settles the outstanding loan balance. The lender recovers the outstanding balance, and the borrower’s family avoids inheriting a debt they never agreed to take on.

Lendsqr has partnered with MyCover.ai to make credit life insurance available directly through the platform. When you enable it on a loan product, a policy is automatically created for every loan disbursed under that product. There is no manual enrollment and no complex claims setup for your team to manage at origination.

Why credit life insurance matters for lending portfolios

The most common argument against credit life insurance is that it adds cost to the borrower. That is true. The premium comes out of the loan amount at disbursement. But the more important question for lenders is what the portfolio looks like without it.

Uninsured defaults after death or disability are unrecoverable: A borrower who passes away or becomes permanently disabled cannot repay. Your collections team cannot pursue a deceased borrower’s estate for a consumer loan. Without insurance, that balance writes off. With it, the insurer settles the outstanding amount.

The borrower’s family carries less risk: Borrowers with dependents are often more willing to take a loan if they know their family will not inherit the debt in a worst-case scenario. For some segments, particularly lower-income and informal sector borrowers, this assurance matters when deciding whether to borrow.

Lenders can offer more competitive terms: Transferring a portion of default risk to an insurer reduces your overall portfolio exposure. This gives lenders more flexibility to price products competitively without absorbing all the downside themselves.

How a claim works in practice

When a covered event occurs, your team or the borrower’s family can invoke the insurance policy to settle the outstanding loan balance.

Here is how this typically plays out. A borrower on your platform with an active loan dies. A family member or your collections team identifies that the loan has an active credit life policy. A family member or your team submits the claim to MyCover.ai with supporting documentation confirming the event. Once MyCover.ai verifies and approves the claim, the insurer pays the outstanding loan balance directly. The loan closes, your disbursement account receives the covered amount, and your team avoids pursuing the estate or family for repayment.

The key operational implication is that your team should be aware of when a claim situation exists. If a borrower stops responding to collections contact and there is reason to believe a covered event occurred, checking whether a credit life policy is in place should be part of the collections escalation process.

What credit life insurance covers and what it does not

The coverage on Lendsqr’s credit life insurance applies to three events: death of the borrower, permanent disability that prevents the borrower from working, and loss of employment.

It does not cover voluntary resignation, temporary unemployment, loans that fall into default for financial reasons unrelated to a covered event, or situations where the borrower simply chooses not to repay. Credit life insurance is not a substitute for credit risk assessment or your collections process. It covers the narrow set of catastrophic events where the borrower genuinely cannot repay.

This is worth communicating to borrowers at the point of loan disbursement. Many borrowers assume the insurance covers any reason they cannot pay. Clarifying the scope upfront prevents disputes when a borrower’s claim does not meet the policy criteria.

How the premium works and what borrowers pay

The system calculates the premium automatically based on the loan amount. Lendsqr deducts it from the loan at disbursement, so the borrower receives slightly less than the approved amount. For example, a borrower approved for ₦200,000 with a ₦3,000 premium receives ₦197,000.

The premium amount is not configurable by the lender. The system handles the calculation, and you should not edit the credit life insurance fee once you add it to a product. Editing it would break the automatic calculation.

Because the premium reduces the amount the borrower receives, it should appear clearly on the loan offer letter so borrowers understand the deduction before accepting. This avoids confusion at disbursement when they receive less than the headline amount. For guidance on configuring what appears on your offer letter, read how to configure and customize loan offer letters in Lendsqr.

How to enable credit life insurance on a loan product on the Admin Console

You can enable credit life insurance on a loan product using the following steps:

Log in to the Lendsqr admin console. Navigate to “Product Management” in the left sidebar and select “Loan Products.”

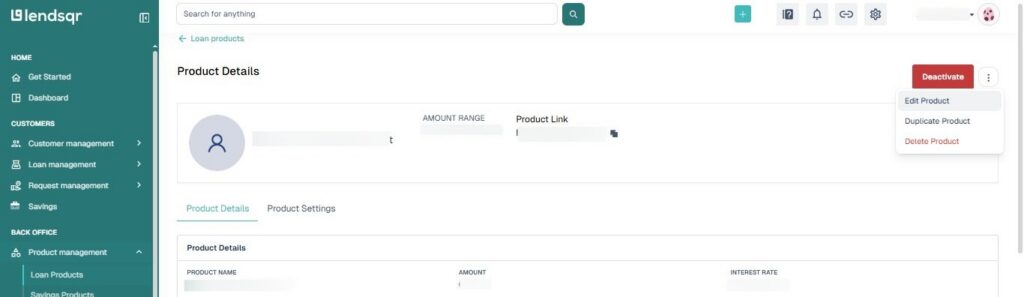

Click on an existing loan product to edit it, or create a new one.

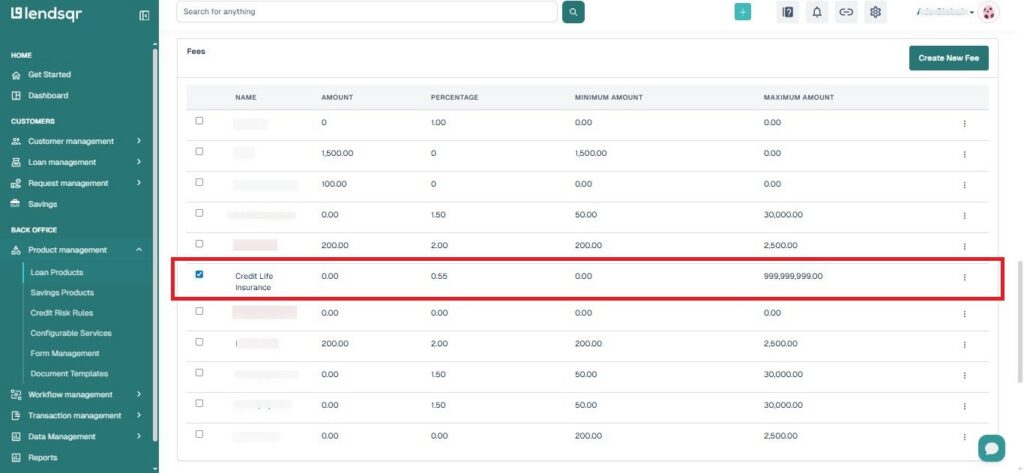

Navigate to the Fees section on the loan product and select the Credit Life Insurance fee. Proceed to update any other fees or details as required by your organization. Then, save the product or changes.

The credit life insurance fee is now active on the product. From this point, every loan disbursed under this product will have a policy automatically created by MyCover.ai at the time of disbursement. Your team takes no further action for each loan after that.

To get answers to common questions about coverage scope, claim eligibility, and borrower communication, read FAQs on credit life insurance.