Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

How to view and edit penalty calculations on your loans

Updated

On this page

Understanding penalty calculations in loan management

Penalty calculations help you manage loans more effectively by encouraging borrowers to repay on time and follow the agreed terms. Lenders usually apply these penalties when borrowers miss payments, delay repayment, or violate other terms of the loan agreement.

With the Penalty Calculation feature, you can view a detailed breakdown of all penalties linked to a customer’s loan under Loan Details. Additionally, you can edit penalties attached to approved loans. If any incorrect penalty fees were added, you can easily update them to reflect the correct amounts.

The role of penalties in effective loan management

Penalties serve multiple strategic purposes in lending operations beyond simply punishing late payment. Understanding these purposes helps you design penalty structures that support your business objectives while maintaining fair treatment of borrowers.

First and foremost, penalties create financial incentives for timely repayment. When borrowers know that missing a payment will result in additional charges, they are more likely to prioritize your loan repayment over other financial obligations. This motivation becomes particularly important in environments where borrowers juggle multiple debts and must decide which creditors to pay first.

Penalties also help compensate lenders for the costs associated with late payments. When borrowers miss payments, your organization incurs additional administrative costs from follow-up calls, collection efforts, and extended monitoring. The interest you would have earned on timely payments is delayed, creating opportunity costs. Reasonable penalties help offset these tangible business impacts.

Penalties also establish clear expectations and consequences that protect the integrity of your loan agreements. Without penalties, loan terms become suggestions rather than binding commitments. Borrowers might delay payments, knowing there are no real consequences, creating a culture of non-compliance that undermines your entire lending operation.

However, penalties must be balanced carefully. Excessive penalties can push struggling borrowers deeper into financial distress, increasing default rates rather than improving collections. They can also damage your reputation and potentially violate consumer protection regulations. The key is designing penalty structures that encourage compliance without becoming predatory.

Definition of terms in penalty calculations

Each penalty comes with specific settings that determine how it is applied. Understanding these components allows you to configure penalties that align with your business strategy and regulatory requirements.

Name

Effective naming helps both your internal team and borrowers understand what the penalty is for. Examples include “Late Payment Fee,” “Missed Payment Penalty,” “Early Repayment Charge,” or “Covenant Violation Fee.” Clear, descriptive names reduce confusion and make reporting more transparent.

Amount

The amount represents the penalty’s fixed amount. It applies a fixed penalty charge, regardless of the loan size. For example, you might charge a flat 500 naira late payment fee, whether the loan is 10,000 naira or 100,000 naira. Fixed amounts work well for small administrative penalties where the cost to your business is roughly the same regardless of loan size.

Percentage

The percentage indicates what portion of the applicable amount contributes to the penalty. It calculates the penalty based on a specific percentage of the applicable amount. For instance, a 5% late payment penalty on a loan with 20,000 naira outstanding would generate a 1,000 naira penalty. Percentage-based penalties scale with loan size, which often feels more proportionate and fair to borrowers.

Applicable to

This setting determines whether the penalty applies only to the principal or to both principal and interest. Applying penalties to principal only results in lower penalty amounts but might not adequately compensate for lost interest revenue. Applying to both principal and interest generates higher penalties that more fully reflect your actual losses from late payment. Your choice here significantly impacts penalty amounts and should reflect your business model and competitive positioning.

Minimum amount

The minimum amount sets the lowest possible penalty that can be charged, providing a floor. Even if the percentage calculation would result in a very small penalty, the minimum ensures you collect at least a baseline amount. For example, you might set a 2% penalty with a minimum of 200 naira, ensuring that even small loans incur meaningful penalties that justify the administrative effort of tracking and collecting them.

Maximum amount

This setting caps the penalty, ensuring it does not exceed a certain amount, even for larger loans. Maximum caps protect borrowers from extremely high penalties on large loans while potentially keeping you compliant with regulations that restrict penalty amounts. For example, a 5% penalty with a 5,000 naira maximum means a borrower with a 200,000 naira loan would pay 5,000 naira rather than the 10,000 naira that an uncapped calculation would generate.

Grace period

The grace period specifies the number of days after the due date before a penalty is applied. Grace periods acknowledge that sometimes delays happen for legitimate reasons like bank processing times or temporary cash flow timing issues. A three to five day grace period is common, giving borrowers a small window to make late payments without penalty while still maintaining overall payment discipline.

Frequency

This specifies how often the penalty gets applied, whether daily, weekly, monthly, or as a one-time charge. Daily penalties compound quickly and create strong incentives for immediate payment, but can seem harsh. Weekly or monthly penalties are less aggressive but might not motivate urgent action. One-time penalties are simplest to understand and administer, but do not increase pressure over time if the borrower continues to delay.

Max amount basis

This setting caps the penalty at either the principal, outstanding principal of a loan schedule, or allows for no capping, depending on your business and regulatory requirements. Using principal as the basis means penalties can never exceed the original loan amount. Using outstanding principal as the basis means penalties are capped based on what is currently owed, which decreases over time as the borrower repays.

Common penalty structures and their applications

Different lending scenarios call for different penalty approaches. Understanding common structures helps you choose configurations that match your specific loan products and customer segments.

For short-term loans with quick turnaround expectations, aggressive penalty structures might be appropriate. A daily penalty of 1% after a two-day grace period creates strong motivation for rapid repayment. These penalties suit scenarios where you need fast capital recycling and borrowers understand the urgency.

For longer-term loans like mortgages or business loans, more moderate penalties work better. A one-time 5% late fee after a five-day grace period followed by additional monthly penalties if the situation continues balances firmness with reasonableness. This structure gives borrowers time to resolve temporary issues while maintaining consequences for prolonged delinquency.

Microfinance and salary advance loans often use percentage-based penalties with minimums to ensure even small loans generate meaningful penalties. A 3% penalty with a 100 naira minimum ensures administrative costs are covered while remaining proportionate to loan size.

Asset-backed loans might have different penalty structures for different violations. Missing a payment might trigger one penalty while failure to maintain insurance on collateral triggers another. Multiple penalty types help you enforce various loan covenants beyond just payment timing.

How to edit penalties on running loans

Sometimes you need to modify loan penalties that are already active. This might be necessary to correct errors, accommodate special circumstances, or respond to regulatory changes. The Lendsqr platform allows you to edit penalties attached to approved loans efficiently.

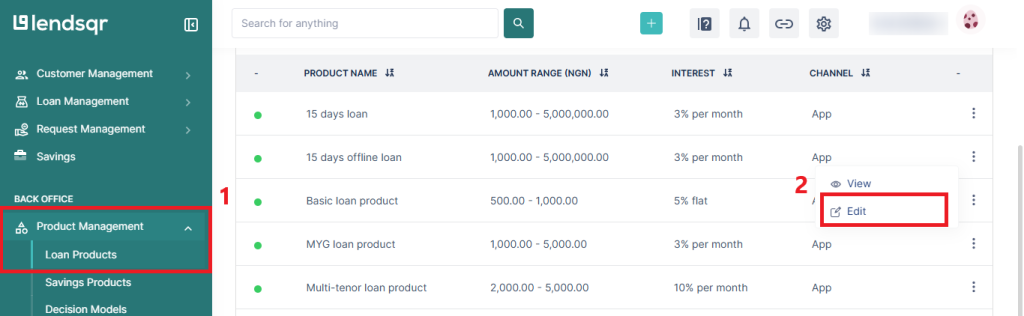

Step 1: Navigate to “Loan products” under the “Product management” tab

From the side navigation menu in the Lendsqr admin console, locate and click on the “Product Management” tab. This will expand to show various product-related options. Select “Loan Products” from this menu. You will be taken to a page displaying all the loan products you have created on your platform, including details like product names, interest rates, tenors, and current status.

Step 2: Select the loan product with the penalty and click “Edit”

Scan through the list of loan products to find the specific product that contains the penalty you need to modify. Each loan product will have associated actions accessible through a dropdown menu or action buttons. Click the dropdown menu for the relevant loan product, then select “Edit” from the options. This action opens the loan product configuration interface, where you can modify various settings, including fees and penalties.

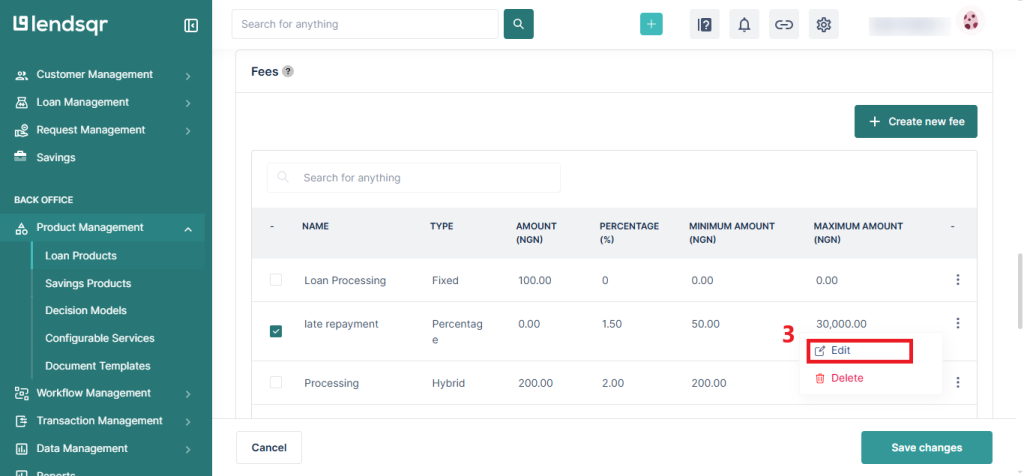

Step 3: Scroll down to the “Fees” section and click on “Edit” for the penal fee

Once you are in the loan product edit interface, scroll down through the various sections until you locate the “Fees” section. This section displays all fees and penalties associated with this loan product, including processing fees, management fees, and penalty fees. Identify the specific penal fee you want to modify. Each fee will have its own edit option. Click on “Edit” next to the penalty fee tied to the loan product that you wish to change.

Step 4: Update the fee details and save changes

After clicking edit, you will see the detailed configuration for that penalty fee. You can now update any of the penalty parameters, including the amount, percentage, applicable setting, minimum amount, maximum amount, grace period, frequency, or max amount basis. Make the necessary changes to reflect the correct penalty structure. Review your changes carefully to ensure accuracy. Once you are satisfied with the updates, click “Update Fee” to save and effect the changes. The system will process your modifications and apply them to the loan product.

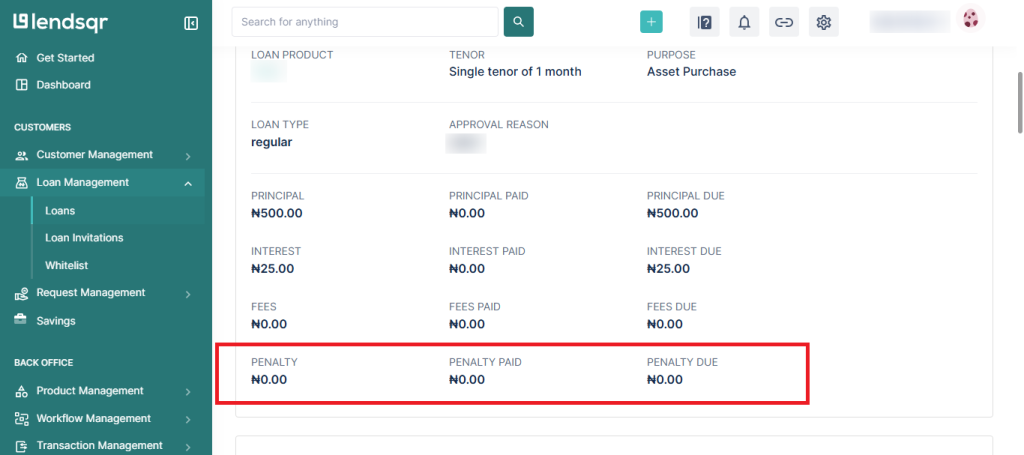

Step 5: View the penalty fee and updates in the loan details

To verify that your changes have been properly applied and to see how penalties are calculated on actual loans, navigate to the “Loans” tab in your admin console. Select a specific loan that uses this loan product. Scroll down to the “Loan Details” section of that loan. In this section, you can view comprehensive information about the loan including the penalties owed or paid. This view shows you the practical impact of your penalty configurations on real borrower accounts. You can see how much in penalties has been charged, when penalties were applied, and whether borrowers have paid them.

Best practices for penalty management

Effective penalty management requires more than just configuring the technical settings. Follow these best practices to ensure your penalty structures serve your business objectives while treating borrowers fairly.

Always communicate penalty terms clearly to borrowers before they take out loans. Include detailed penalty information in loan agreements and offer letters. Borrowers should never be surprised by penalty charges because they were not properly informed up front.

Set penalties at levels that motivate compliance without being predatory. Research what competitors charge and what regulators allow. Penalties that are too low will not change behavior, while penalties that are too serious damage your reputation and might violate consumer protection laws.

Monitor penalty revenue and incidence regularly. High penalty revenue might initially seem positive but often indicates underlying problems with your underwriting or borrower education. If many borrowers are paying penalties, you might need to improve borrower selection or provide better payment reminders.

Consider the borrower’s circumstances when enforcing penalties. While consistent enforcement is important for credibility, having discretion to waive penalties in genuine hardship cases builds goodwill and can improve long-term recovery rates. A borrower who lost their job might default if you pile on penalties, but might recover and repay if you show flexibility.

Use penalties as engagement triggers rather than just revenue sources. When a borrower incurs their first penalty, reach out to understand what happened and offer assistance. Early intervention often prevents a small issue from becoming a major default.

Keep detailed records of all penalty assessments, waivers, and modifications. This documentation protects you in disputes and audits while providing data for analyzing penalty effectiveness.

Review and update your penalty structures regularly based on performance data. If certain penalties do not seem to improve payment behavior, adjust them. If borrowers frequently request waivers for specific penalties, the penalty might be poorly designed or communicated.

Ensure your technology correctly calculates and applies penalties. Errors that overcharge borrowers damage trust and can trigger regulatory action. Errors that undercharge penalties cost you revenue and undermine the deterrent effect. Regular audits of penalty calculations help catch and correct issues.

Train your customer service team on penalty policies and give them clear guidelines on when they can waive or modify penalties. Inconsistent enforcement creates perceptions of unfairness and can lead to borrower complaints.

Penalty calculations represent a critical tool in your loan management arsenal. When configured thoughtfully and administered fairly, they promote repayment discipline, compensate for collection costs, and provide early warning of borrower distress. When misused, they can damage borrower relationships and expose you to regulatory risk.

feature")