Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

How to enable NIN verification on your loan product

Updated

On this page

Identity fraud is one of the most common risks digital lenders face in Nigeria. Someone applies using another person’s details, passes basic checks, and receives funds they never intend to repay. By the time the lender notices, the money is gone.

Requiring borrowers to verify their National Identification Number (NIN) during the application is one of the most effective ways to stop this. Lendsqr lets lenders enable this on any loan product and choose exactly when in the borrower journey the check runs.

This guide explains what NIN verification does in lending, how the timing options compare, and how to configure it in your admin console.

Why NIN verification matters for lenders

A National Identification Number (NIN) is a unique identity number the Nigerian government assigns to every citizen through the National Identity Management Commission (NIMC). It links to a person’s biometric data, including fingerprints and facial image. This makes it one of the most reliable identity credentials available to lenders in Nigeria.

When a lender enables NIN verification on a loan product, the system cross-checks the borrower’s NIN record against their BVN data. If the details match, the borrower passes. If they do not, the application stops until the issue gets resolved.

This matters for three reasons.

Fraud prevention. A fraudster applying with stolen identity details would need both the NIN and BVN of the same person to align. NIN verification makes this combination significantly harder to fake.

Compliance. Regulatory expectations around Know Your Customer (KYC) requirements in Nigeria are increasing. Collecting and verifying NIN data helps lenders demonstrate that they took reasonable steps to confirm borrower identity before disbursing funds.

Portfolio quality. Loans made to verified borrowers tend to perform better than those made without proper identity confirmation. Borrowers who know their real identity is on record are less likely to default strategically.

Understanding the available timing options

Lendsqr gives lenders a choice about when NIN verification happens in the loan application flow. This is not a minor detail. The timing you choose affects both borrower experience and your overall risk exposure. Here are the available timing options for NIN verification:

Before loan request

When you choose this option, a borrower must complete NIN verification before the system lets them submit a loan application. If they cannot verify their NIN, they cannot proceed.

This is the stricter setting. It works well for lenders who want to filter out unverifiable applicants early. It also reduces wasted processing time on applications that would ultimately fail the NIN check anyway.

The trade-off is friction. Some borrowers may have minor discrepancies between their NIN and BVN records due to data entry errors made during enrollment. These borrowers may abandon the application at this step, even though they are legitimate customers. If drop-off rates matter to you, this setting warrants careful monitoring after you enable it.

After loan request

With this option, borrowers can submit a loan application first. NIN verification then runs as a required step before the loan gets approved or disbursed.

This approach keeps the initial application experience smooth and lets you collect more borrower data before running the identity check. It suits lenders who want to assess affordability and creditworthiness first, then run the NIN check only on applicants who actually qualify.

The risk with this approach is that unverified borrowers appear in your pipeline until the check runs. If your team manually reviews applications, this means some effort goes into cases that may ultimately fail identity verification.

None

This option turns NIN verification off for the product. Use this for products where NIN verification is not required, or where you rely on other identity verification methods.

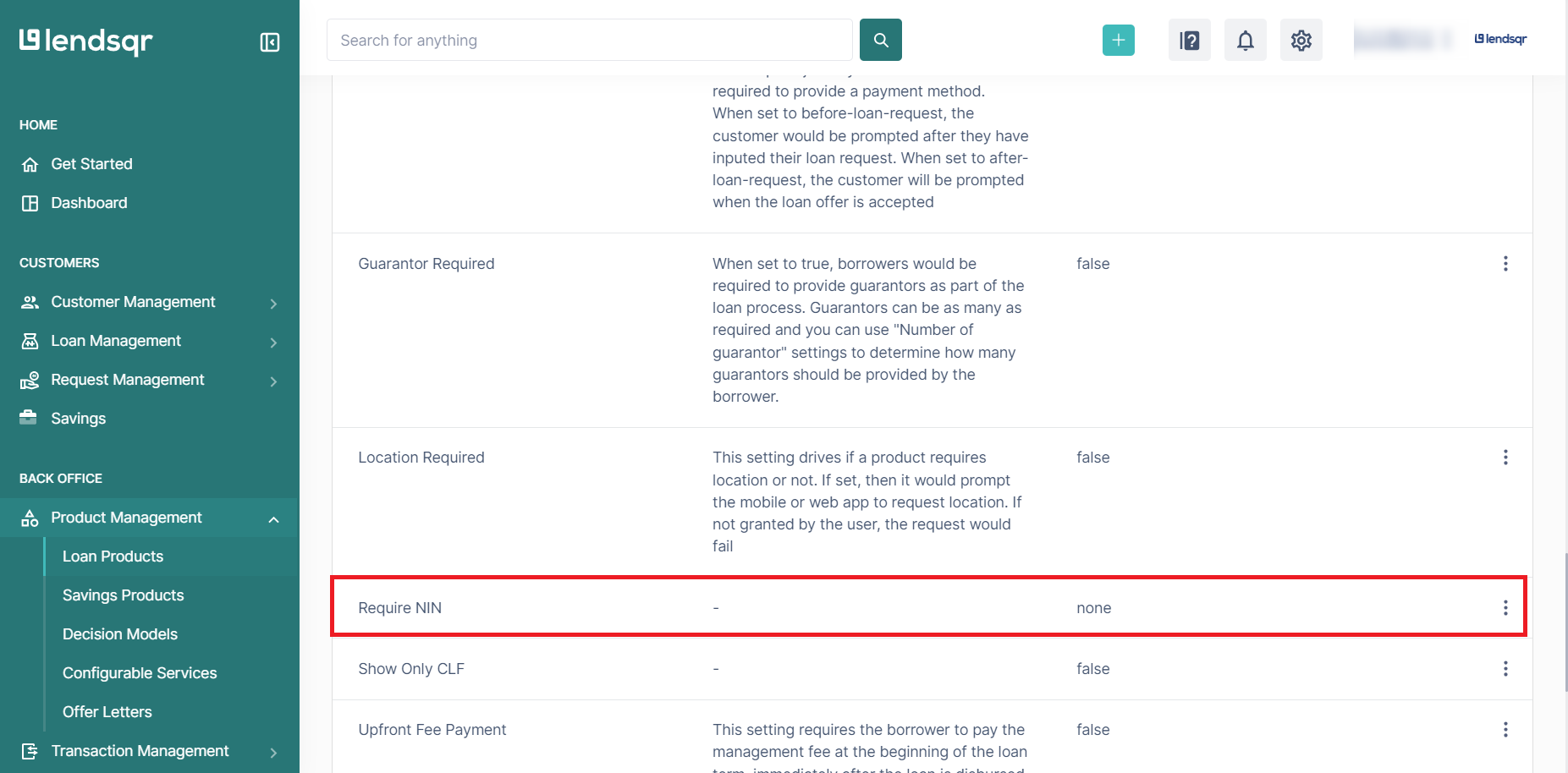

How to enable NIN verification on your loan product

Log in to your Lendsqr admin console and navigate to Product Management, then select Loan Products.

Select an existing loan product or create a new one.

Click on the Product Attributes tab within the product settings page.

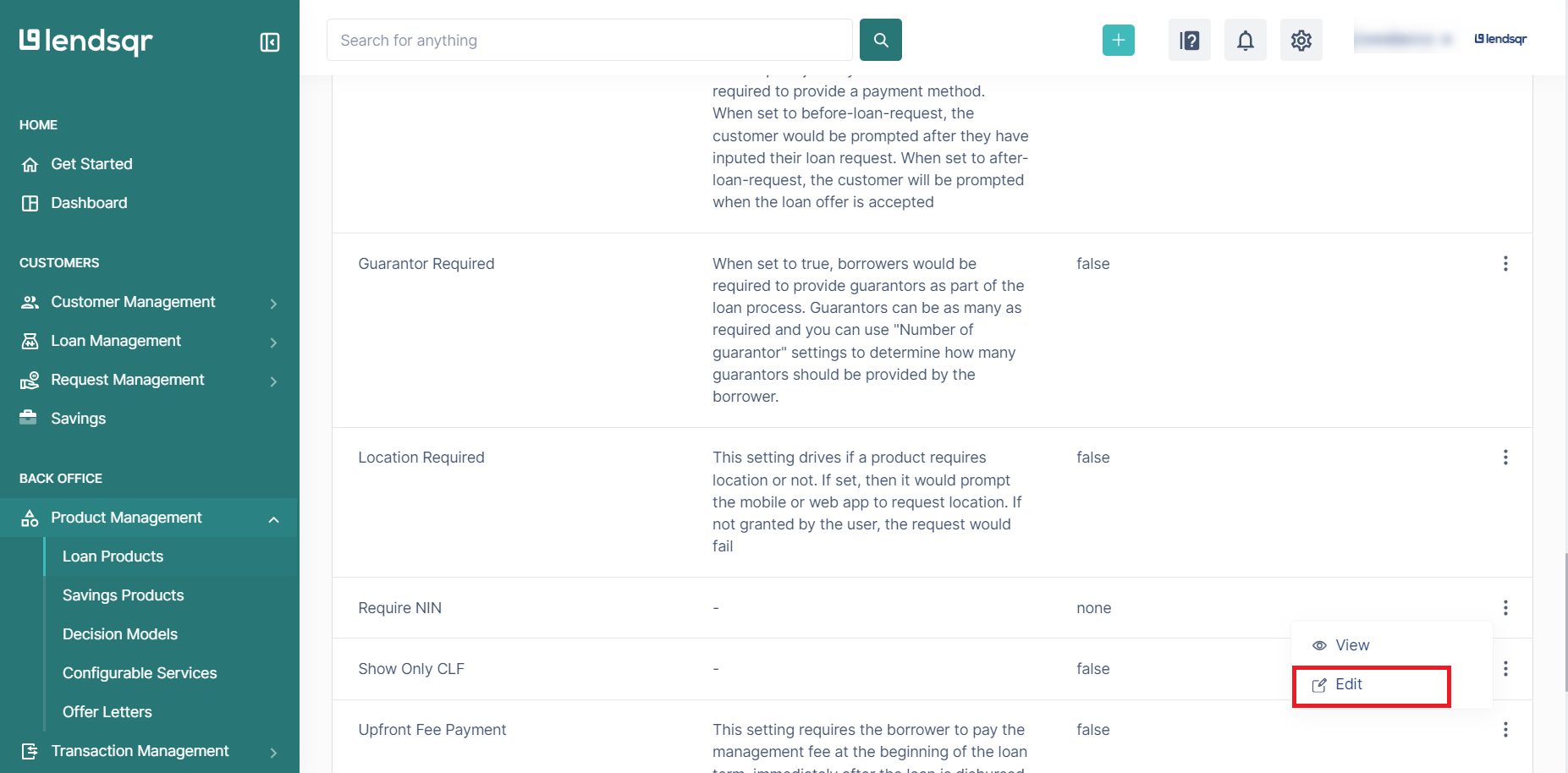

Scroll through the attributes list to find Require NIN. Click the more options button next to it and select Edit.

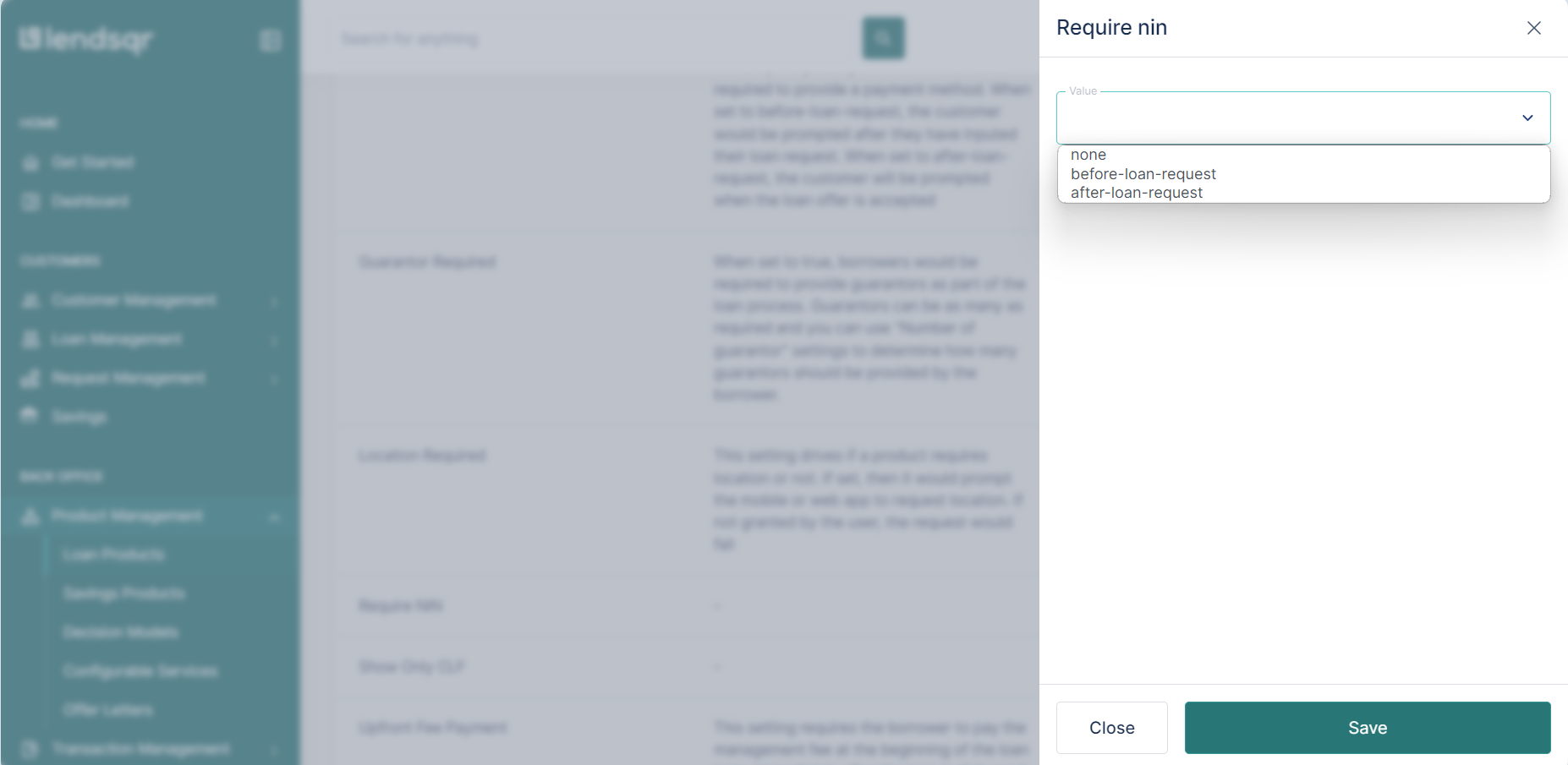

Select one of the three options:

1. Before Loan Request: This ensures that the customer’s NIN is verified before they can make a loan request.

2. After Loan Request: This allows customers to make a loan request, but verifies their NIN before approval or disbursement.

3. None: Opt-out of NIN verification if it is not required for this loan product.

Once you have selected an option, click on the Save button to apply the changes to the loan product.

What to keep in mind after enabling NIN verification

Once NIN verification is active on a product, every new loan application under that product follows the timing you selected. Existing loans already in the pipeline are not affected.

If borrowers struggle to pass NIN verification because of mismatches between their NIN and BVN records, you can adjust which fields the system cross-checks. This separate configuration is covered in the guide: How to fix NIN verification mismatches on your loan applications.

For a broader understanding of how identity verification fits into your KYC setup on Lendsqr, read the Introduction to KYC. For more on managing fraud risk in digital lending, visit the Lendsqr blog.