Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

What is Karma on the Lendsqr admin console?

Updated

On this page

Karma is a blacklist engine that stores information on parties who defaulted on loans or committed fraud on Lendsqr-powered platforms.

On the Lendsqr admin console, Karma appears as a module inside a credit risk rule or decision model. When enabled, it runs a set of configurable checks on a borrower before the loan decision is completed. This helps lenders detect known fraud patterns, identify repeat defaulters, and stop suspicious applications earlier in the lending process.

Karma is not a standalone loan decision engine. Instead, it works as one part of a broader credit risk setup, alongside modules such as Credit Bureau, Scoring, Ecosystem, Whitelist, and Custom rules.

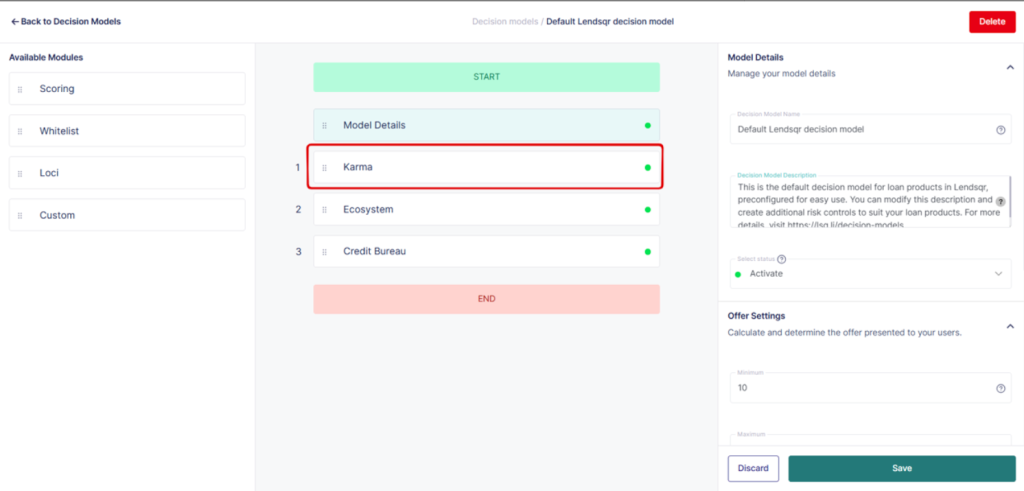

Where Karma lives on the admin console

Karma is configured within a credit risk rule or decision model on the Lendsqr admin console.

When a lender opens a decision model, Karma appears as one of the available modules that can be added to the credit decision flow. Once selected, the module can be configured from the side panel, where the lender can view the module details, turn controls on or off, and choose which checks should be applied during evaluation.

This means Karma is set up at the policy level, not manually applied one borrower at a time. Once the rule is configured, the system automatically evaluates eligible applications using the selected Karma checks.

How Karma works

Karma checks different borrower attributes against the Karma database and related fraud signals. It works on a pass or fail basis.

In the support guidance for this module, a pass means the borrower matched a disqualifying condition, which automatically makes the customer ineligible for the loan. In other words, Karma acts as a hard risk gate when configured that way.

A typical flow looks like this:

A borrower submits a loan application.

The application enters the lender’s decision model.

The Karma module checks the borrower using the enabled criteria.

If a disqualifying match or inconsistency is found, the borrower fails the rule.

If no disqualifying issue is found, the application continues through the rest of the decision flow.

This makes Karma especially useful early in the journey, before offer generation or final approval.

What Karma checks

From the Karma configuration page, the module can be set to check the following borrower attributes:

IP address

BVN

Phone number

BVN phone number relationship

Device ID

Office email address

Personal email address

Office email domain

Personal email domain

These checks help lenders decide how strict or broad the fraud screening should be for a given product or decision model.

BVN checks

BVN-related checks help the lender identify whether the borrower’s identity details match known records and whether that identity has already been associated with risk signals in the Karma ecosystem.

This is useful for detecting suspicious identity usage and stopping repeat bad actors who may be applying through a new lender.

Phone number checks

Phone number checks help detect whether a number has been linked to previous suspicious activity, chronic default behavior, or identity inconsistencies.

These checks are particularly useful in environments where fraudsters cycle through multiple applications using reused or manipulated contact details.

BVN phone number checks

This check looks at whether the borrower’s BVN and phone number relationship is consistent with known records.

If the submitted phone number does not align with the borrower identity being used, that can be a strong fraud signal and may cause the borrower to fail the Karma rule.

Device ID checks

Device checks help surface patterns such as one device being used across multiple borrower profiles, or a single borrower account appearing across unusual device combinations.

This is useful because device reuse is often one of the clearest indicators of coordinated fraud, account sharing, or synthetic application behavior.

IP checks

IP checks can help identify suspicious network behavior, especially where multiple applications appear to originate from the same source or a source already associated with risky activity.

Email and email domain checks

Karma can also evaluate personal and office email addresses, as well as their domains. These checks help uncover repeated use of shared email identities, suspicious domain patterns, or contact details already connected to problematic applications.

What Karma helps detect

Karma is more than a basic blacklist lookup. It helps identify both known bad actors and patterns that suggest fraud or misrepresentation.

Based on the support material and product screenshots, Karma can help detect:

Identity mismatches

If a borrower’s submitted details do not align properly across records, that may indicate impersonation, altered identity information, or a fabricated profile.

For example, inconsistencies between BVN and phone number details can be treated as an immediate risk signal.

Reused or shared devices

If multiple customers are applying from the same device, or a borrower appears across several devices in a suspicious way, Karma can help flag that behavior for automatic failure or further review.

Recycled contact details

Repeated use of the same phone numbers, email addresses, or email domains across questionable applications can indicate account farming or coordinated fraud attempts.

Known fraud and chronic default signals

Karma also helps surface cases where the borrower has already been associated with default or fraud-related activity within the wider ecosystem.

This is one of the biggest advantages of the module. A borrower may be new to one lender but not new to the broader network of risk signals.

Why lenders use Karma

Karma gives lenders access to shared intelligence that goes beyond their own internal customer history.

Instead of waiting to discover fraud or default patterns after disbursement, lenders can use Karma to identify risk much earlier. This helps reduce avoidable losses, improve approval quality, and strengthen automated lending controls.

Lenders typically use Karma to:

screen out high-risk borrowers earlier

reduce fraud exposure

identify repeat defaulters across a wider ecosystem

improve automated underwriting decisions

add an extra layer of protection before presenting an offer

This is especially valuable for lenders running digital lending products, where decisions need to be made quickly and manual checks may not be practical at scale.

Module controls on the Karma page

The Karma module also includes configuration controls that affect how it behaves within the decision model.

Required

When this is enabled, the Karma module becomes a mandatory part of the evaluation flow. The application must pass through Karma as configured.

Continue on Failure

This setting determines whether the rest of the decision flow should continue if the module itself encounters a technical issue.

This is an operational setting rather than a risk rule, but it matters because it affects how resilient or strict the lending flow is during service interruptions.

Pre Offer

When enabled, Karma runs before an offer is generated. This is useful for lenders who want to block risky borrowers before the system calculates or displays a loan offer.

A practical example

Imagine a borrower applies for a loan with details that look valid on the surface. The application includes a phone number, BVN, and email address that appear complete, and the borrower passes basic form validation.

However, Karma detects that:

the BVN and phone number combination is inconsistent

the device has already been used across multiple borrower accounts

the email address has been linked to earlier suspicious applications

Without Karma, that borrower might continue deeper into the loan process. With Karma enabled, the application can be stopped immediately as part of the decision model.

This helps the lender avoid preventable risk before disbursement happens.

What Karma is not

To avoid confusion, Karma should be clearly distinguished from other risk tools.

Karma is not a credit bureau

Karma does not replace credit bureau reporting or credit bureau scoring. It is not designed to serve as a formal bureau product.

Karma is not a lending platform on its own

Karma does not disburse loans or manage the entire credit lifecycle by itself. It supports lenders by providing fraud and default intelligence within the broader Lendsqr ecosystem.

Karma is not the only approval criterion

Karma is one input into a decision model. Lenders may still use bureau checks, internal scoring, affordability logic, employment checks, product rules, or manual review as part of final approval decisions.

Data and ecosystem context

Karma is built around a shared intelligence model. It benefits from data signals contributed within the Lendsqr ecosystem and uses those signals to help lenders detect risky borrowers more effectively.

That shared structure is part of what makes the module useful. A lender may not yet have enough internal history to identify a problematic borrower, but Karma can help by drawing from a wider pool of fraud and default intelligence.

This also explains why Karma should be viewed as an ecosystem risk tool rather than a lender-specific rule in isolation.

When to use Karma

Karma is most useful when a lender wants stronger protection against fraud and chronic default at the point of decision.

It is especially relevant when:

approvals are automated or semi-automated

fraud risk is high

the lender serves many first-time borrowers

manual review capacity is limited

the business wants to identify risky applicants before offer generation

In many cases, Karma works best when combined with other decision modules so that both fraud risk and creditworthiness are evaluated together.

Summary

Karma on the Lendsqr admin console is a configurable fraud and default intelligence module used within credit risk rules and decision models. It helps lenders screen borrowers using checks such as BVN, phone number, device ID, IP address, and email-based signals.

Its purpose is to help lenders detect suspicious applications, identify known bad actors, and reduce avoidable credit losses earlier in the lending process.

Used properly, Karma strengthens underwriting by giving lenders another layer of intelligence before a loan is approved. It is not a credit bureau and it should not be the only factor in decision-making, but it is an important part of a stronger risk control framework on Lendsqr.