Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

Introduction to manual loan scoring for underwriting

Introduction

Manual Loan Scoring allows lenders to introduce human underwriting into the loan decision process using configurable scoring forms and decision models.

Instead of relying entirely on automated application data, authorized officers can manually assess a loan request, provide additional underwriting information, and trigger scoring based on internal credit rules.

This feature is configured at the loan product level and works together with your existing credit risk and offer generation setup.

Cases where underwriters need to provide additional context before offer generation

Configuring Manual Loan Scoring

Manual loan scoring is configured under the loan product settings.

To configure it:

Navigate to Product Management

Open the preferred loan product

Go to Product Settings

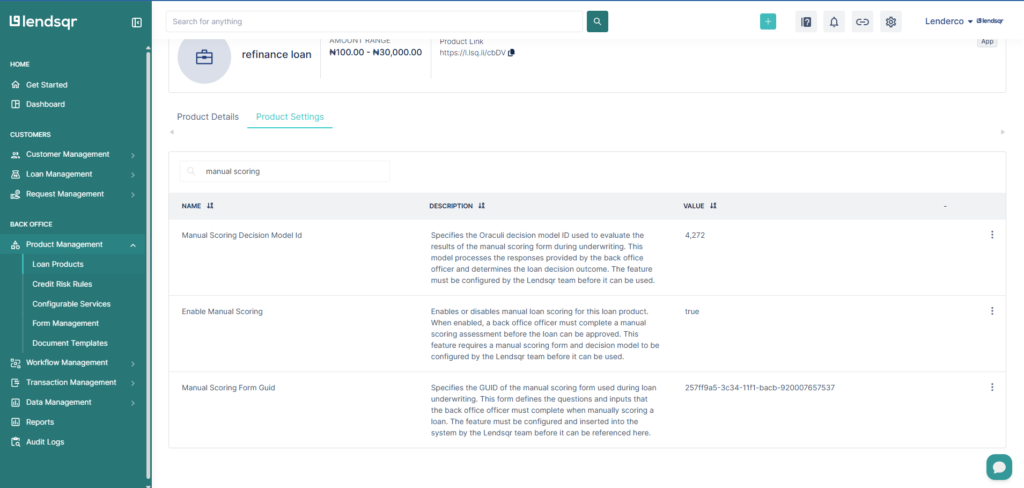

The following settings are available for configuration

Setting

Description

Manual Loan Scoring Form

Allows you to select the preconfigured form that underwriters will complete during scoring. The dropdown displays all previously created forms available for scoring. To create a form, refer to the Forms Management guide.

Enable Manual Loan Scoring

Checkbox used to enable or disable manual scoring for the product. When enabled, underwriters can manually score loan requests for the product.

Decision Model to Perform Scoring

Allows you to select the credit risk rule or decision model that will process the submitted scoring data. Available options are fetched from your configured credit risk rules.

Important Configuration Requirement

To ensure scoring works correctly, all field IDs used within the scoring form must be referenced inside the decision model logic using:

attributes.id

Each field should use the correct attribute reference expected by the scoring engine.

Example:

If a scoring form field has an ID of:

monthly_income

The decision model should reference:

attributes.monthly_income

This ensures the submitted form data is properly passed into the scoring logic.

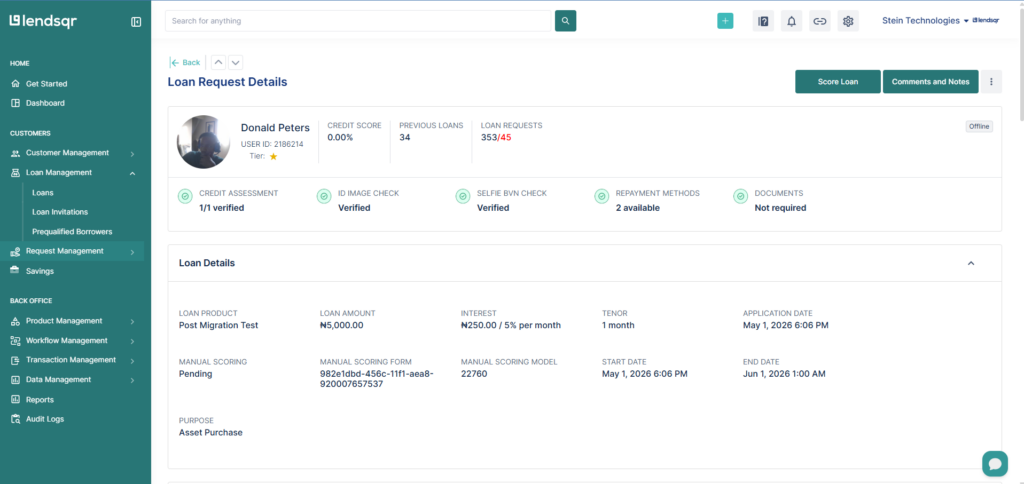

How to score a loan after configuration

Once a customer applies for this loan, it is visible on the Loan requests module. To score the loan, kindly follow the steps below:

Navigate to the specific Loan request

Click on Score

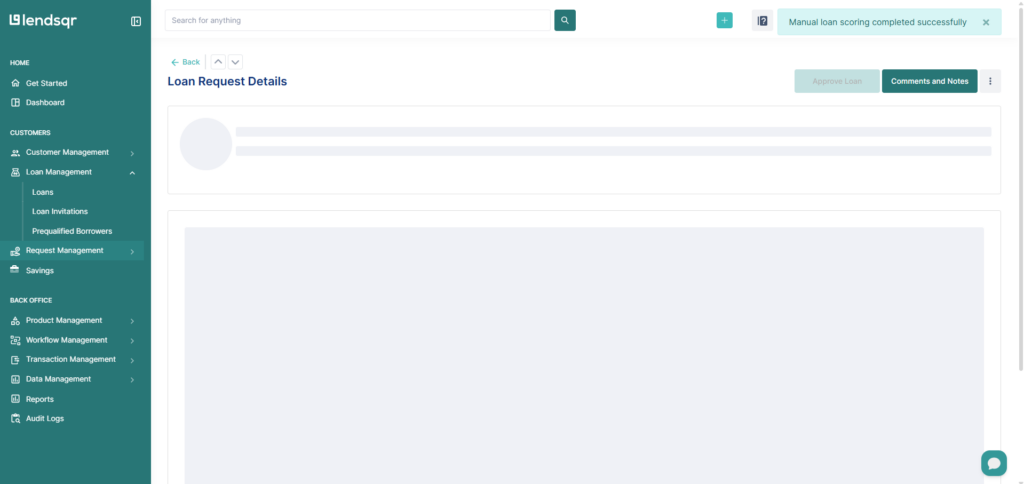

Complete the form required for scoring and Submit

You should see a message that the loan has been successfully scored.

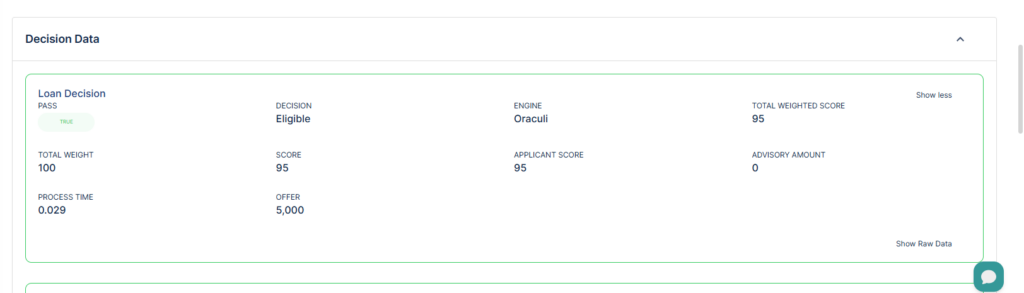

Scroll down to the decision data section to see the new update

feature")