Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

How to manage guarantor details

Updated

On this page

Imagine a microfinance lender running a portfolio of small business loans, notices a cluster of defaults. After investigating, they discovered that several of the defaulting borrowers listed the same person as their guarantor, someone who never had the financial standing to back even a single loan. Had the lender regularly reviewed their guarantor data, they could have caught this pattern early and limited their exposure. This is exactly the kind of oversight that guarantor management on Lendsqr makes possible. Whether you are a digital lender in Nigeria or anywhere else Lendsqr operates, the admin console gives you a centralized view of every guarantor backing your borrowers, what they have guaranteed, and whether they have been validated.

What is a loan guarantor?

A loan guarantor is a person who agrees to take on the responsibility of repaying a borrower’s loan if the borrower defaults. By providing a guarantor, the borrower gives the lender an additional layer of financial security, especially useful when the borrower’s own credit profile is thin or unproven. Guarantors are common in many lending contexts: • A salary earner guarantees a loan for a younger sibling who is self-employed and has no credit history. • An employer guarantees a loan for a staff member as part of a welfare benefit scheme. • A community leader or group head guarantees loans for members in a group lending program. In each of these scenarios, the lender needs to know who the guarantor is, verify that they are who they say they are, and monitor their exposure across multiple loans.

Why lenders should actively manage guarantor details

Simply collecting guarantor information at the point of loan application is not enough. Active management matters because:

A single guarantor can be linked to multiple loans. If several of those loans default simultaneously, the guarantor may not be able to cover all of them. Reviewing this exposure helps you set limits early.

Guarantor details can be fraudulent. Without validation, borrowers can submit false guarantor information. Lendsqr’s validation tools help you confirm a guarantor is real and consenting.

Regulatory compliance. In some jurisdictions, lenders are expected to keep verified records of anyone who acts as a guarantor on a loan agreement.

How to view guarantor details on the Lendsqr admin console

To access and manage guarantor information on the Lendsqr admin console, follow the steps below.

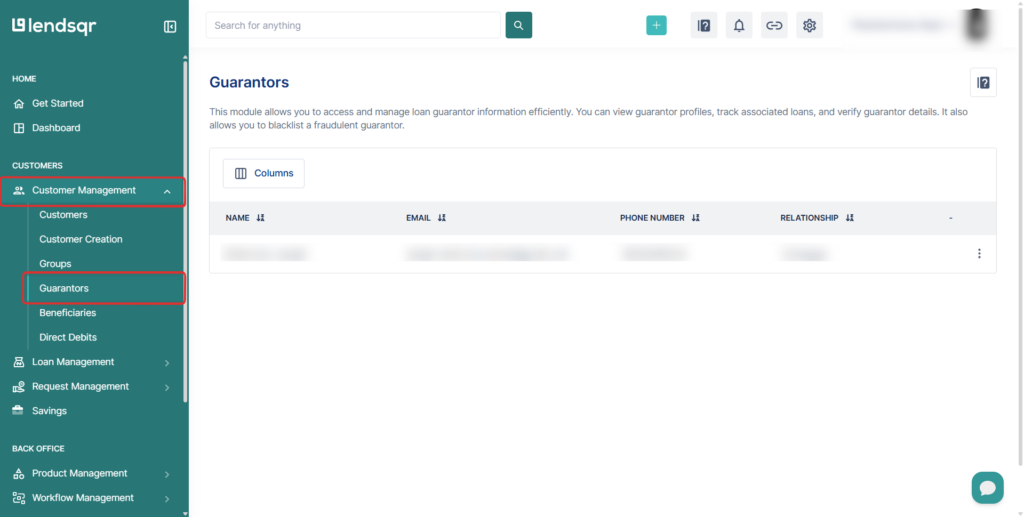

From the left-hand side navigation, click Customer Management.

Select Guarantors from the sub-menu.

Step 2: Open a guarantor’s profile

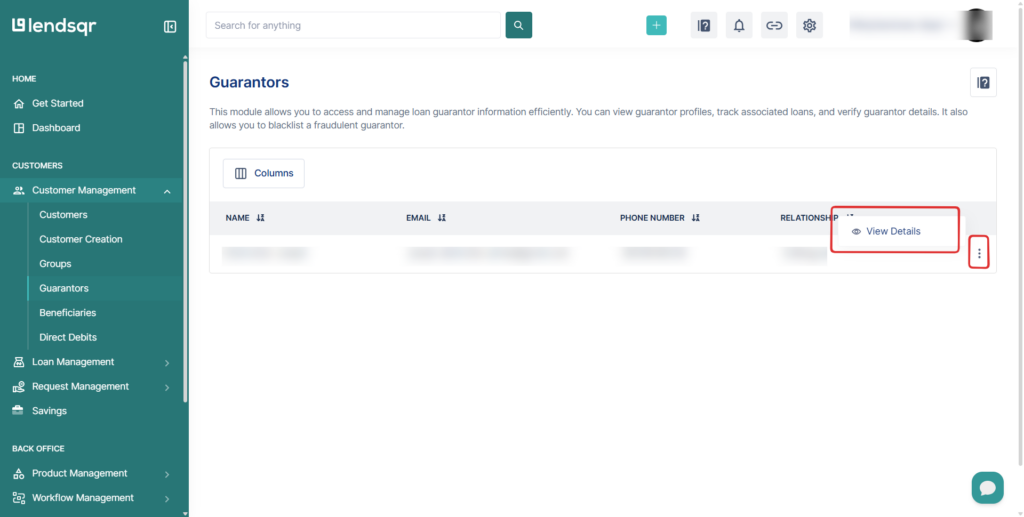

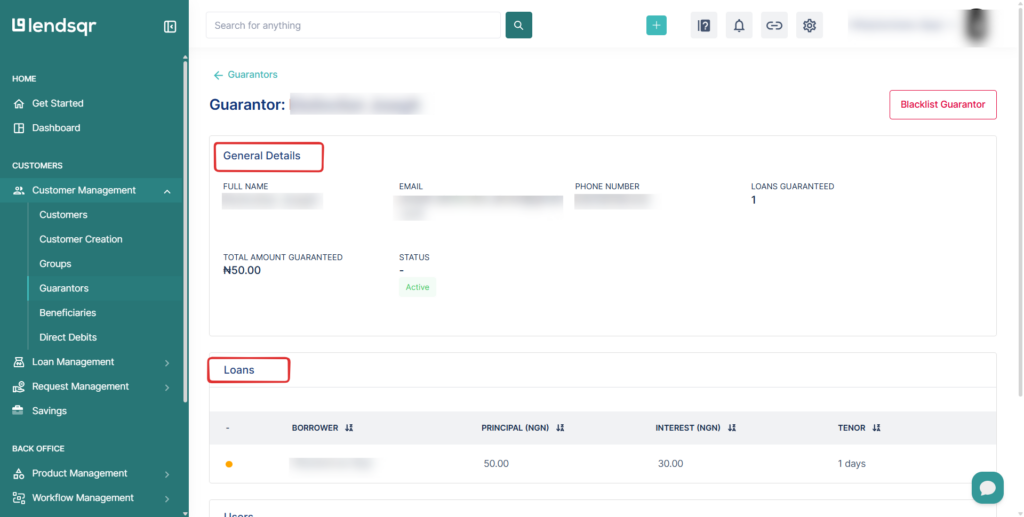

Once you have located the guarantor in the results table, click on their name or row to open their full profile, or you can click the three-dot menu (…) at the end of the row and select “View Details“. Inside, you will find three main sections:

General Details: Here you will find personal information about the guarantor, including their name, contact details, and identity verification status.

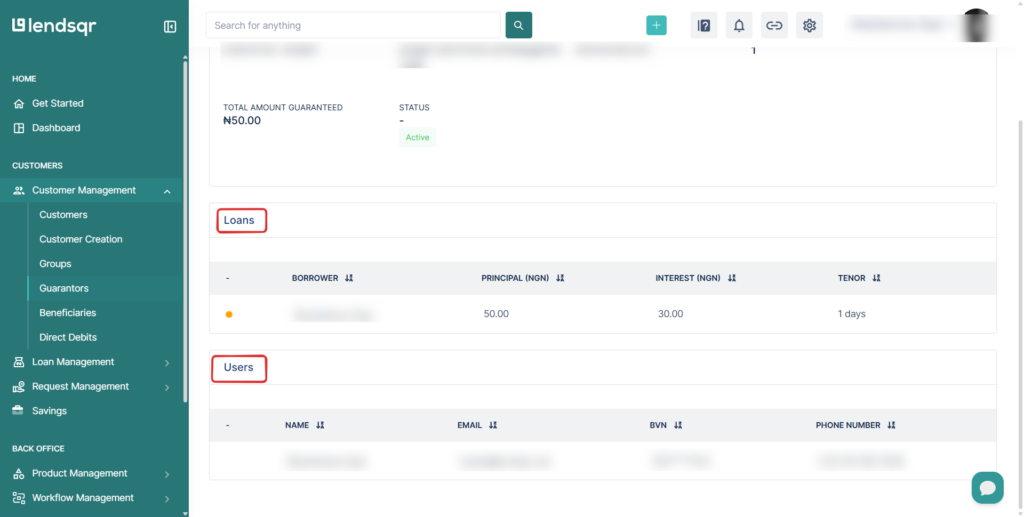

Loans: This section contains a list of the loans tied to a guarantor.

Users: This section contains a list of borrowers this guarantor is backing.

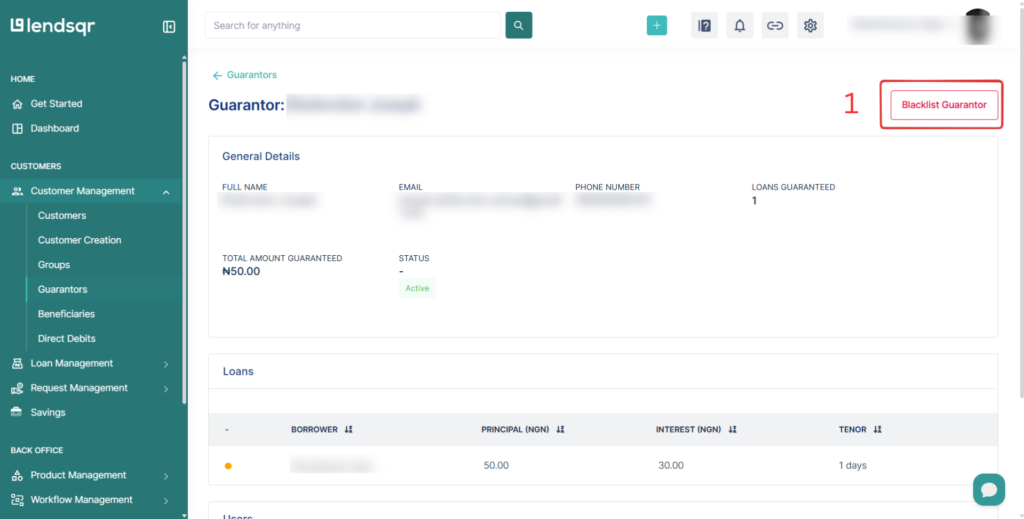

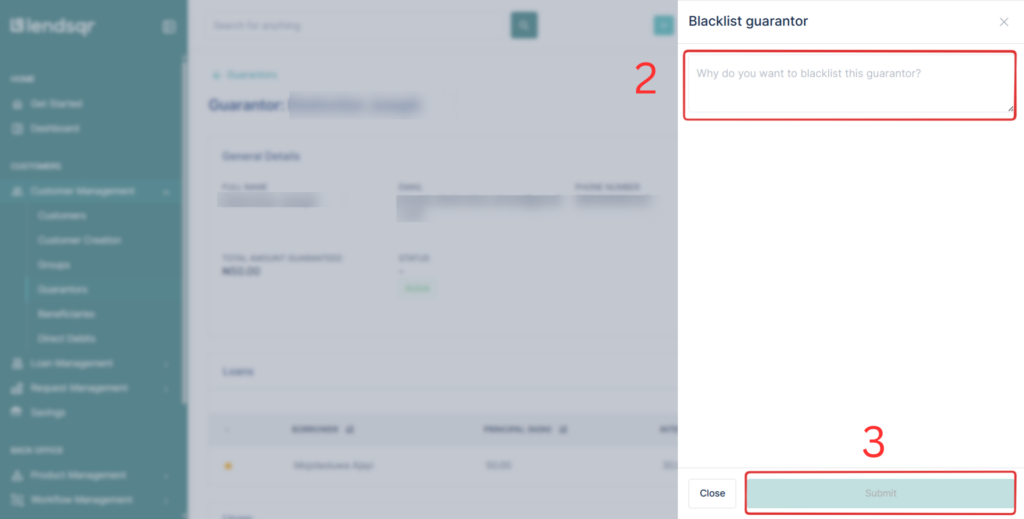

Step 3: Blacklisting a guarantor

To blacklist a guarantor you deem fraudulent, you simply have to click on the “Blacklist Guarantor” option at the top-right corner of the page. Then you’ll be prompted to input a reason why you want to blacklist the selected guarantor before proceeding to click on the “Submit” button to confirm the blacklisting.

What to look for when reviewing a guarantor

Once you are inside a guarantor’s profile, here are the key things to assess:

Validation status. Has the guarantor been formally validated? An unvalidated guarantor means their identity or consent has not yet been confirmed.

Number of loans guaranteed. If one guarantor is backing a large number of loans, consider whether their financial standing actually supports that exposure.

Repayment performance of linked borrowers. If several borrowers under the same guarantor are defaulting or falling behind, this is a risk signal.

Contact details accuracy. If you ever need to contact a guarantor to enforce repayment, you need accurate phone and email records.