Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

How to use tiers to manage customer KYC

Updated

On this page

Know Your Customer (KYC) is a fundamental requirement in the financial services sector. It is a process used by financial institutions to verify customers’ identities and assess potential risks associated with maintaining a business relationship with them. Over time, KYC has evolved from a simple identity check into a comprehensive framework for monitoring user activity, preventing fraud, and ensuring regulatory compliance.

KYC is not optional. It is a legal and regulatory obligation for lenders and financial service providers. Regulatory authorities require institutions to perform due diligence on their customers to prevent financial crimes such as money laundering, identity theft, and terrorist financing. Failure to comply with KYC requirements can result in penalties, reputational damage, and operational restrictions.

Beyond compliance, KYC also plays a critical role in operational efficiency and risk management. By properly verifying and categorizing users, lenders can make more informed decisions, set appropriate transaction limits, and tailor services based on user profiles.

KYC management on Lendsqr

The Lendsqr admin console provides a built-in system for managing KYC through a structured tiering framework. This system allows lenders to group users into different levels based on the information they have provided and the level of verification they have completed.

Each tier represents a specific level of trust and access. Users in lower tiers typically have limited access to platform features and lower transaction thresholds, while users in higher tiers enjoy increased privileges and fewer restrictions.

This tier-based approach allows lenders to balance accessibility with risk control. New users can onboard quickly with minimal requirements, while additional verification steps can be introduced progressively as users engage more deeply with the platform.

Understanding KYC tiers

A KYC tier is essentially a classification level assigned to a user based on the documentation they have submitted and the verification checks they have passed. Each tier is defined by a set of rules and requirements.

These rules typically include:

The type of identification documents required, such as a national ID, a voter card, or an international passport

Verification steps, such as phone number confirmation or address verification

Transaction limits, including maximum loan amounts, wallet balances, or transfer limits

Access to specific platform features such as loan applications, bill payments, or savings products

For example, a basic tier may require only a phone number and email address, with strict transaction limits. A higher tier may require government-issued identification and proof of address, allowing for larger transactions and broader access to services.

Benefits of using tiers

Implementing KYC tiers within Lendsqr offers several operational and strategic advantages:

Improved compliance with regulatory standards by enforcing identity verification at different levels

Better risk management through controlled access to financial services

Enhanced user experience by allowing gradual onboarding instead of requiring full documentation upfront

Flexibility to align KYC requirements with both regulatory expectations and internal risk appetite

Ability to monitor and control transaction volumes and user behavior across different customer segments

This approach ensures that lenders can scale their operations while maintaining control over risk exposure.

Tier upgrades and downgrades

One of the key features of the Lendsqr KYC system is the ability to dynamically adjust user tiers. Users are not permanently fixed to a single tier. Instead, they can move between tiers based on their activity and compliance with requirements.

Users can be upgraded when they meet the criteria for a higher tier. This typically involves submitting additional documentation or completing further verification steps. For example, a user may move from a basic tier to an advanced tier after providing a valid government ID and proof of address.

Conversely, users can also be downgraded if necessary. This may happen if previously submitted documents expire, fail verification, or if suspicious activity is detected. Downgrading a user helps mitigate risk by reducing their access to platform features until issues are resolved.

This flexibility allows lenders to maintain an accurate and up-to-date assessment of each user’s risk profile.

Using the tier management feature within Lendsqr is straightforward. The admin console provides an interface for lenders to create, edit, and manage tiers based on their operational needs.

Follow the steps below to access and configure tiers:

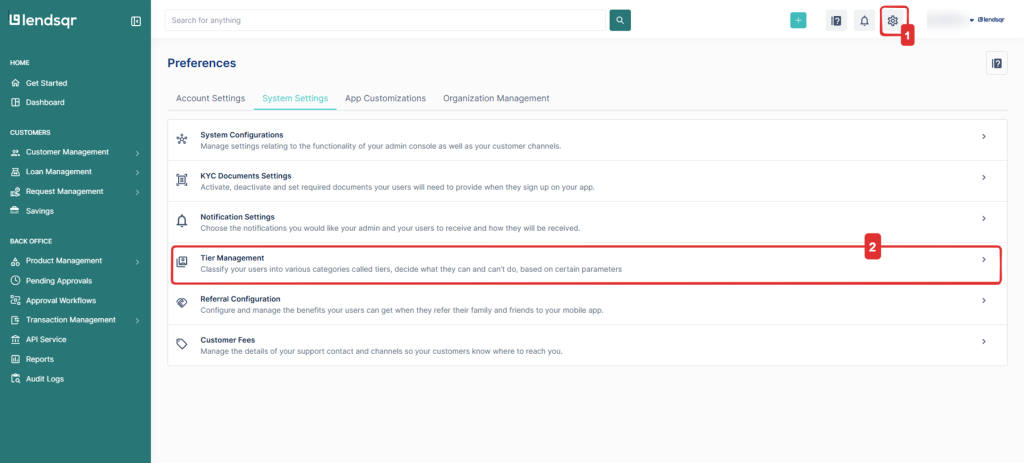

Click the Settings iconat the top right corner of the Lendsqr Admin console.

Click on Tier Management under the “System settings” section

You can choose to modify a pre-existing tier to your preference or create a new tier, click on Edit for any existing tier to modify them or click on New Tier to create a new tier

Proceed to create or update the various tiers and set the limits and documents required for each tier.

Once configured, these tiers will automatically or manually categorize users based on your setup.

Configuring tier requirements

When creating or editing a tier, it is important to carefully define the requirements and limits associated with that tier. These configurations directly impact user experience and risk exposure.

Key elements to consider when configuring tiers include:

Documentation requirements. Specify what users must provide to qualify for the tier.

Transaction limits. Define caps on loans, transfers, wallet funding, and other financial activities.

Feature access. Determine which services are available to users within the tier.

Verification rules. Ensure that submitted documents meet validation standards before approval.

For example, a lender may configure a mid-level tier that requires a government ID and allows moderate loan access, while restricting higher-risk features until further verification is completed.

Compliance and regulatory alignment

KYC tiering must align with applicable regulatory frameworks. Different jurisdictions have specific requirements regarding identity verification, transaction monitoring, and reporting.

Lenders should ensure that:

Tier requirements meet minimum regulatory standards for customer identification

Transaction limits are consistent with compliance guidelines

Verification processes are documented and auditable

Customer data is securely stored and handled in accordance with data protection laws

Failure to align with regulations can expose lenders to legal and financial risks. It is therefore essential to periodically review tier configurations and update them as regulatory requirements evolve.

After implementing KYC tiers, ongoing monitoring is necessary to ensure effectiveness. Lenders should track how users move between tiers and how these movements impact platform activity.

Key metrics to observe include:

Conversion rates from lower tiers to higher tiers

Transaction volumes across different tiers

Incidents of fraud or suspicious activity

User drop-off during the verification process

By analyzing these metrics, lenders can refine their tier structure to improve both compliance and user experience.

This video provides a practical walkthrough of the tier setup process and highlights important configuration steps.