Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

Introduction to KYC

KYC (Know Your Customer) is the process of verifying a borrower’s identity before extending credit. For credit providers in Nigeria and across West Africa, KYC is not optional. It is mandated under Anti-Money Laundering (AML) regulations enforced by the Central Bank of Nigeria (CBN). Beyond compliance, KYC is a foundational risk management tool. Without it, lenders are effectively extending credit to unknown entities with no reliable way to assess repayment capacity, trace fraud, or enforce recovery.

Effective KYC covers three dimensions: identity verification (confirming a borrower is who they claim to be using government-issued ID, biometric matching, and BVN linkage), financial assessment (understanding income, transaction history, and credit behaviour through document review and integrated credit scoring), and risk classification (assigning each borrower a risk tier that determines how much credit they can access and under what conditions). Lendsqr brings all three together in one automated workflow, from the borrower’s first selfie upload to the lender’s final approval decision.

Why credit providers need KYC

Lenders that skip or rush KYC expose themselves to risks that compound over time. Here is what proper KYC protects against:

Identity fraud: criminals use stolen or synthetic identities to take multiple loans with no intention of repaying. Lendsqr’s Document Verification module cross-references selfies against uploaded IDs using AI-powered facial matching, flagging mismatches before disbursement.

Money laundering: fraudsters use loans to legitimise illicit funds. Document verification combined with Lendsqr’s transaction monitoring helps detect suspicious patterns early.

Regulatory penalties: non-compliance with CBN AML directives can result in fines of up to N500 million, public sanctions, and licence suspension.

Poor collection outcomes: when borrowers default, unverified contact details make recovery nearly impossible. KYC-verified information feeds directly into Lendsqr’s Collections module, improving recovery rates.

Portfolio deterioration: lending to unverified, high-risk borrowers without tier controls inflates default rates and provisions. Lendsqr’s Tier Management tool restricts lending limits based on verification depth, keeping the portfolio healthy.

When a borrower completes onboarding, they are automatically placed at Tier 1. As they submit and receive approval for additional verification documents, Lendsqr’s Tier Management tool upgrades them automatically, unlocking higher lending limits at each stage.

Tier 1 requires selfie and OTP verification, and gives borrowers access to small, short-term loans. Identity is confirmed, but risk data is limited. Tier 2 requires a government-issued ID and proof of address, unlocking moderate loan limits once identity and residence are confirmed. Tier 3 requires BVN linkage and income documentation, unlocking the highest lending limits once a full creditworthiness profile is established.

Lenders can view each borrower’s current tier and progression status in the KYC Dashboard and configure lending rules in the Tier Management tool to align credit limits with verification depth.

Real-world scenario 1: the first-time borrower

A borrower downloads a lender’s app built on Lendsqr and applies for her first loan. She uploads a selfie and completes OTP verification, placing her at Tier 1. The system’s AI facial recognition confirms the selfie is live and matches their stated identity. The lender’s Tier Management configuration allows a maximum of N20,000 for Tier 1 borrowers, so the borrower is approved for N15,000 on her first application.

Two weeks later, the borrower submits their National ID card and a utility bill for address verification. The KYC Dashboard flags the submission as pending review. A loan officer opens the Document Verification module, confirms the ID is valid and unexpired, checks that the address on the utility bill matches the declared address, and verifies it. The borrower is then upgraded to Tier 2, and the maximum loan limit increases to N100,000.

Tier progression is driven by verified documents, not time or loyalty. Lendsqr automates the limit upgrade as soon as a document is approved, eliminating manual intervention from the credit rules.

Step-by-step guide: Accessing KYC information and documents

Once a borrower submits their documents via the borrower app, lenders review and approve them through the following workflow in Lendsqr.

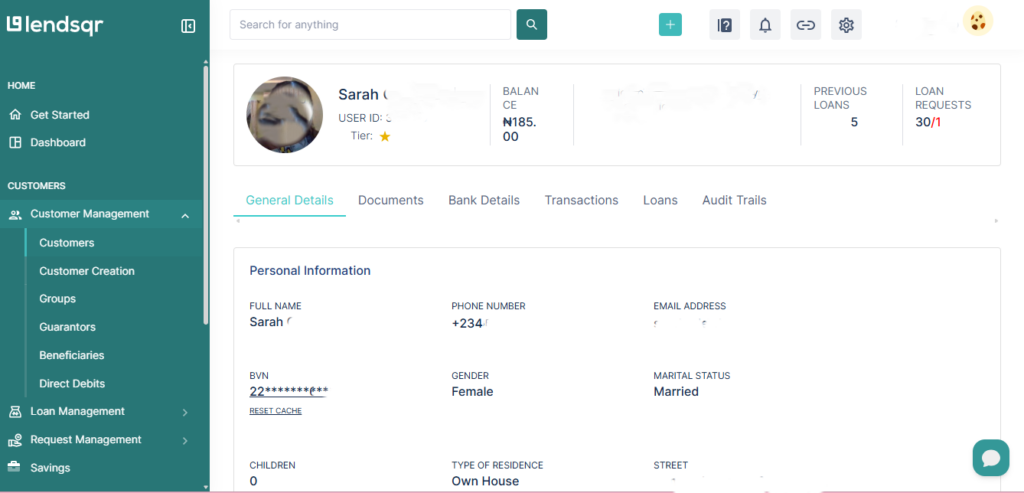

Step 1: Head to the sidebar and go to Customer management, then click Customers to land on the KYC dashboard.

Step 2:. Select any customer from the list to open their full profile.

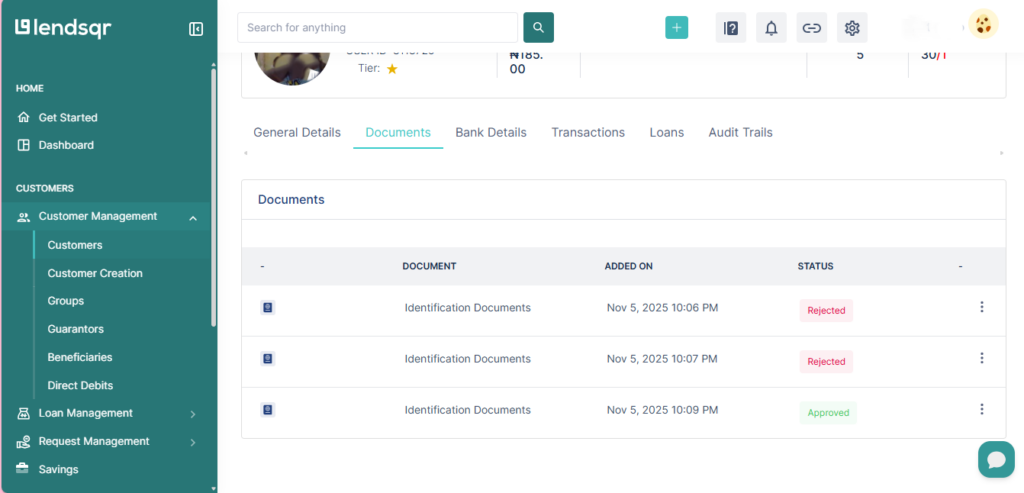

Step 3: The profile is split into six tabs which include the customer’s General details, Documents, Bank details, Transactions, Loans, and Audit trail. The General details tab shows the customer’s full name, phone number, and their tier level, which is represented by stars (e.g. three stars = Tier 3). The Documents tab lists each submitted document alongside its status, which is either approved or rejected.

Acceptable document checklist

Sharing this checklist with your review team and displaying sample images in your borrower app onboarding flow can significantly reduce first-submission rejection rates.

Selfies must be live photos taken in-app. Common rejection reasons include blurry images, obscured faces, photos of photos, and poor lighting.

Government-issued ID (National ID, Driver’s Licence, International Passport, or Voter’s Card) must be fully visible and unexpired. Common rejection reasons include cropped edges, glare or reflection over key fields, and laminate damage.

Proof of address (utility bill, bank statement, or tenancy agreement) must be no older than three months. Common rejection reasons include out-of-date documents, an address that does not match the declared location, and name mismatches.

Ongoing KYC monitoring

KYC is not a one-time event. Borrower circumstances change, and lenders who treat verification as a permanent record rather than a living process expose themselves to risk over time. Lendsqr’s Ongoing Monitoring tab supports annual ID refreshes (automatically prompting borrowers whose IDs are approaching expiry), behavioural triggers (flagging accounts showing unusual repayment patterns, sudden location changes, or device switches), and bulk updates for high-volume refresh requests.

Lenders operating under CBN AML guidelines are expected to demonstrate that KYC is maintained throughout the customer relationship, not just at onboarding. Lendsqr’s audit-ready logs support this requirement, generating compliance reports that can be presented during regulatory reviews.

Legal and financial consequences of poor KYC

Regulatory penalties: the CBN can impose fines of up to N500 million on institutions found non-compliant with AML directives. Repeat violations can result in licence revocation.

Financial losses: without verified borrower data, collections are significantly harder. Default rates rise, provisions increase, and portfolio health deteriorates.

Reputational damage: public regulatory sanctions and audit findings erode customer trust and make it harder to attract institutional funding or partnerships.

Lendsqr’s automated KYC workflow, tiered verification system, and audit logs are designed to make compliance the path of least resistance, not an additional burden layered on top of lending operations.

feature")