Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

How to create or edit a tier on the Lendsqr admin console

Updated

On this page

Not all borrowers are the same. A first-time customer who has just signed up is very different from one who has completed their identity verification, maintained a clean repayment record, and built a relationship with your platform over time. Treating them identically, giving them the same loan limits, the same withdrawal caps, and the same access to products, is a missed opportunity at best and a risk management failure at worst.

This is where customer tiering comes in. It is one of the most practical tools a lender can use to match services to borrower profiles, and it sits at the heart of how modern digital lenders operate responsibly.

Tier management allows you to categorize your customers based on predefined limits and rules such as KYC level, loan limits, and withdrawal caps. With Lendsqr, it’s easy to create or edit a tier on the admin console using just a few steps.

What is a customer tier?

A customer tier is a category that groups borrowers based on how much information you have about them and how much trust they have earned on your platform. Each tier comes with its own set of rules: what documents a borrower must provide, how much they can borrow, how much they can withdraw, and what products they can access.

Think of it like levels of access. A borrower who has only provided a phone number and email address sits at a basic tier with limited privileges. One who has submitted their identity documents, verified their bank account, and completed full KYC requirements moves into a higher tier with more access and larger limits.

The tier a borrower occupies at any point determines what they can do on your platform. As they provide more information and build a track record, they move up. This keeps your risk exposure proportionate to what you actually know about each customer.

Why tiering matters in lending operations

Customer tiering is not just a technical configuration. It shapes how a lending business grows and how well it manages risk. Here is why lenders who build their operations around tiering have a meaningful advantage.

It enforces proportionate risk. Giving a new, unverified borrower the same loan limit as a fully verified, long-standing customer is a risk no lender should take. Tiers ensure that borrowing privileges scale with trust and verified information.

It supports regulatory compliance. Most financial regulators require lenders to apply Know Your Customer (KYC) requirements in stages. Tiering is the operational mechanism for this. You set what each tier requires, and the system enforces it automatically.

It creates a clear path for borrower progression. When borrowers know what they need to do to unlock higher limits or access better products, they have an incentive to complete their profiles and engage more deeply with your platform. This drives both compliance and retention.

It protects new customers from over-indebtedness. Starting borrowers at conservative limits and scaling up as they demonstrate reliability is a form of consumer protection. It prevents lenders from extending credit that a borrower cannot reasonably repay.

It makes your portfolio easier to manage. When borrowers are segmented by tier, you can analyze performance, default rates, and repayment behavior at each level. This makes it easier to spot problems, adjust policies, and understand which segments of your customer base are most valuable.

It enables product differentiation. Different tiers can unlock different loan products. A borrower at your highest tier might access longer tenures, lower interest rates, or larger loan amounts. This gives lenders a natural upselling path without creating unnecessary risk.

A practical tiering example

Consider a digital lender with three tiers. Tier one requires only a phone number and basic personal information. Borrowers here can access small short-term loans with low limits and modest withdrawal caps. Tier two requires government-issued ID and a verified bank account. It unlocks higher loan amounts and faster approvals. Tier three requires full KYC verification including income documentation. It gives access to the lender’s premium products, the largest loan limits, and the most favorable terms.

A new borrower starts at tier one. They take a small loan, repay on time, and submit their ID. The platform moves them to tier two. Over time, as they demonstrate repayment behavior and complete their full KYC, they progress to tier three. At each stage, the lender’s exposure grows in proportion to what they know and what the borrower has demonstrated.

This is tiering working as it should.

How to create a tier on Lendsqr

Lendsqr’s admin console gives you full control over your tier structure. You can create as many tiers as your lending model requires and define the specific rules that apply to each one.

To create a new tier:

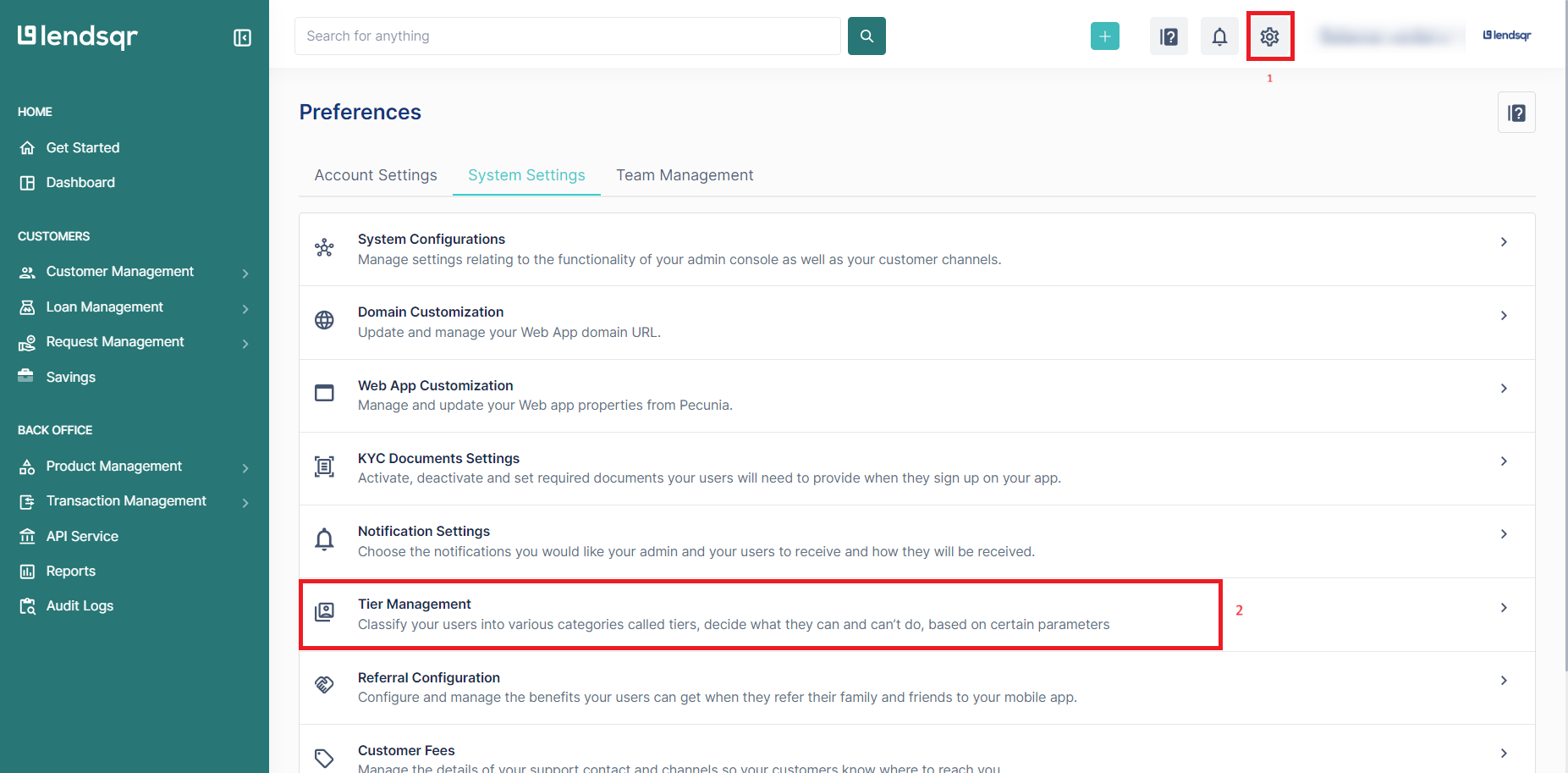

Click the Settings button at the top right corner of the admin console.

Select Tier Management from the menu.

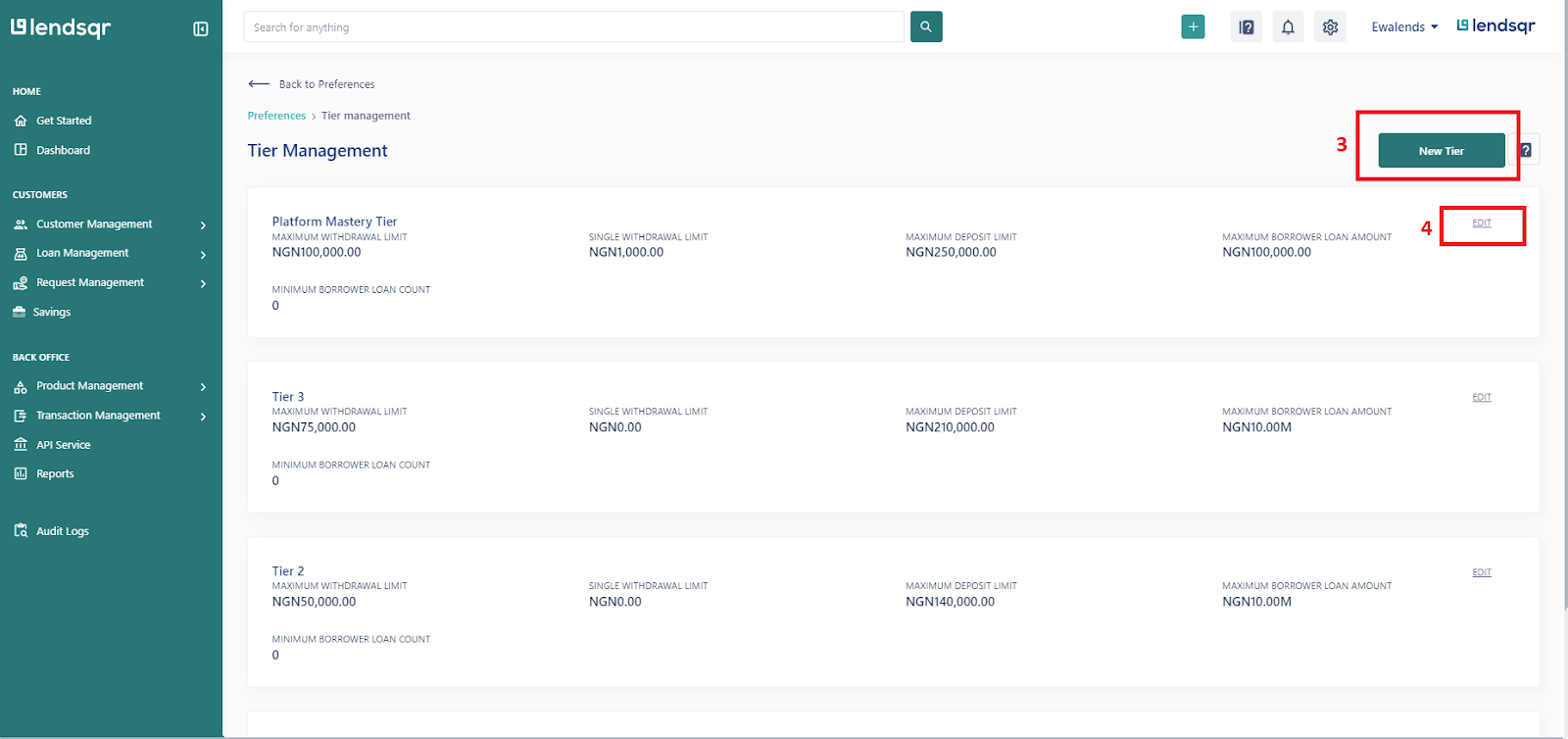

Click the New Tier button.

Fill in the required fields, including tier limits, KYC requirements, loan limits, and withdrawal caps.

Click Create to save the new tier.

What you can configure within a tier

Each tier on Lendsqr gives you control over several parameters. You can specify:

The maximum loan amount a borrower in this tier can request

The maximum number of active loans they can hold at once

The maximum amount they can withdraw at a time

The KYC documents they must provide to qualify for this tier

Any additional loan eligibility requirements specific to this tier

These settings give you the flexibility to build a tiering structure that matches your actual credit policy, not just a generic template.

How to edit an existing tier

As your business grows and your understanding of your borrowers deepens, you may need to adjust your tier settings. Lendsqr makes it straightforward to update any tier without disrupting borrowers who are already active on your platform.

To edit a tier:

Click the Settings button at the top right corner of the admin console as shown previously.

Select Tier Management.

Locate the tier you want to modify and click Edit.

Update the relevant fields with the new values.

Click Save changes to confirm. A confirmation message will appear once the tier has been updated successfully.

Tips for designing your tier structure

Before setting up your tiers, it helps to think through the logic behind them. Here are a few practical considerations.

Start with your KYC policy. Decide what documents or verifications move a borrower from one tier to the next. Your regulatory environment will often guide this.

Align your limits to your risk appetite. The loan and withdrawal limits for each tier should reflect what you are comfortable extending to borrowers at that level of verification. Conservative limits at lower tiers protect you while still keeping lower-tier borrowers engaged.

Keep the number of tiers manageable. Two to four tiers are usually enough for most lending operations. Too many tiers add administrative complexity without meaningful benefit.

Review your tiers regularly. As your portfolio matures, you will learn more about how borrowers in each tier behave. Use that data to fine-tune your limits and requirements.

Learn more

To understand the broader concept behind customer tiering on Lendsqr, see What is tier management?