Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

How to view customers’ documents

Updated

On this page

When a borrower applies for a loan, the information they enter on the application is only part of the picture. Lenders still need supporting documents to confirm identity, verify income, and reduce the risk of fraud or default. These documents are a core part of Know Your Customer (KYC) checks and are often the difference between a safe approval and a risky one.

On Lendsqr, you can view all uploaded customer documents directly from the customer profile page. This gives your team a centralized view of verification files, their status, and what action is needed next.

Why customer documents matter in lending decisions

Documents help lenders move from assumption-based decisions to evidence-based decisions. Without them, a lender is relying entirely on self-reported information, which can be incomplete or misleading. With them, you can validate key claims before disbursing funds.

Lenders typically use customer documents to:

Confirm identity and prevent impersonation

Validate residential address

Verify income stability and employment status

Cross-check declared information against real evidence

Meet regulatory KYC and compliance requirements

Reduce exposure to fraud and identity manipulation

For example, if a borrower claims to earn a fixed monthly salary, a payslip or bank statement can confirm whether the income aligns with what was declared in the application. If there is a mismatch, the lender may pause or decline the application.

In higher-risk portfolios, documents also act as a second layer of defense after automated decisioning rules.

How documents influence real lending workflows

In practice, document review is not just a compliance step. It directly affects loan outcomes.

A typical lending flow looks like this:

Customer submits loan application

The system collects KYC documents

Credit decision rules are evaluated

Documents are reviewed by operations or risk teams

Final approval or rejection is issued

Each step depends on the quality of the documents provided.

Example scenario

A lender offering salary-based loans receives an application from a customer claiming a stable monthly income. The borrower uploads a payslip and a bank statement.

During review, the lender notices that:

The payslip shows a different employer name from the application

The bank statement reflects irregular income deposits

In this case, even if the application passes initial automated checks, the document review introduces a manual risk flag. The lender may downgrade the loan amount, request clarification, or reject the application entirely.

This is why document visibility inside the customer profile is critical.

What you will find in the Documents tab

On Lendsqr, all uploaded customer files are stored in the Documents tab inside the customer profile.

Depending on your configuration, this may include:

Government-issued identity documents

Utility bills or proof of address

Payslips and employment letters

Bank statements

Custom documents defined by your lending policy

Each file is stored with its verification status, making it easier to track what has been reviewed and what still requires attention.

The Documents tab is only visible when a customer has uploaded at least one document through the Lendsqr customer web app.

If no documents have been uploaded, the tab will not appear in the customer profile. In this case, you may need to request that the customer complete their KYC or upload the required files before proceeding with verification or loan assessment.

This ensures your workspace stays clean and only shows relevant verification data for active applications.

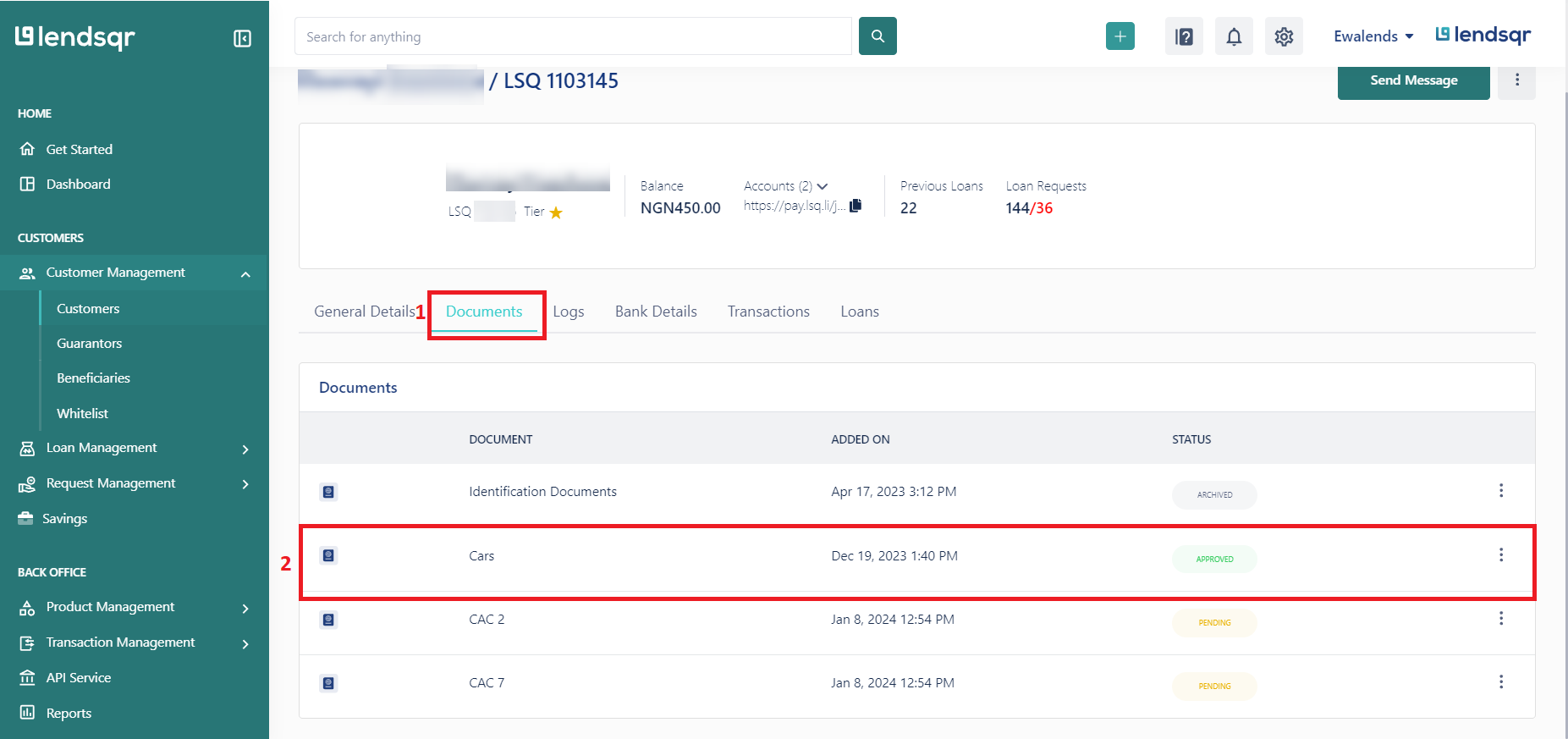

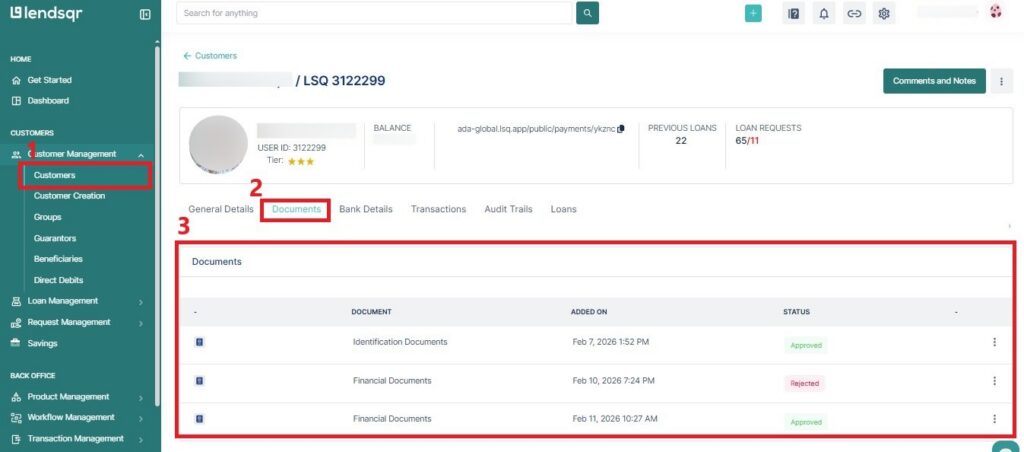

How to view customer documents on Lendsqr

To access and review customer documents:

Log in to your Lendsqr admin console

Go to Customer Management

Search for the customer using name, phone number, or email

Open the customer profile

Click the Documents tab

Select any document to preview and review details

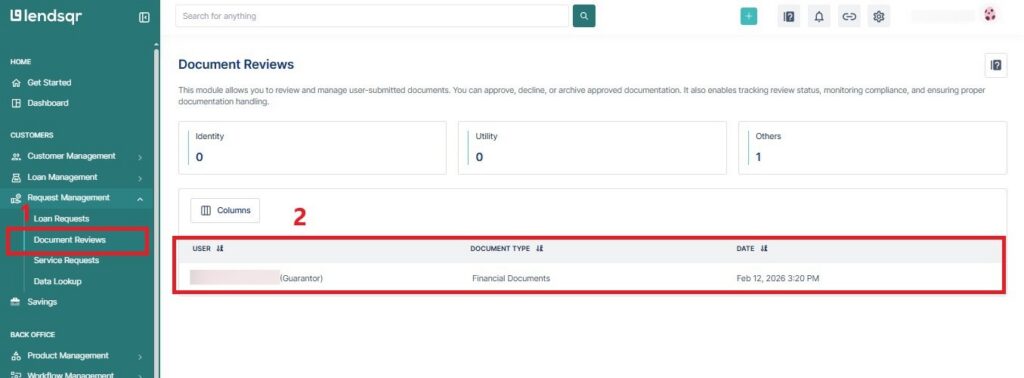

You can also view pending documents to be reviewed by heading over to the ‘Request Management’ tab.

Select ‘Document Reviews,’ and you should see the documents uploaded by your customers or even guarantors.

Understanding document verification statuses

Each uploaded document is assigned a status that reflects its current stage in the review lifecycle.

Pending

The document has been uploaded but has not yet been checked. At this stage, lenders typically prioritize it for review if the application is urgent or high-value.

Approved

The document has passed verification checks. It can now be used to support lending decisions or compliance audits.

Rejected

The document does not meet the required standards. This could be due to poor image quality, mismatched information, or signs of tampering.

Example in practice

If a customer uploads a blurred ID card, the reviewer may mark it as rejected and request a re-upload. The loan application will typically remain on hold until a valid document is provided.

This ensures that approvals are not based on incomplete or unreliable data.

When reviewing documents, lenders typically focus on both authenticity and consistency.

Key checks include:

Whether the document is readable and complete

Whether names match across all submitted files

Whether dates and expiry information are valid

Whether the document aligns with declared income or identity

Whether there are signs of editing or manipulation

Whether document quality meets internal standards

A consistent review process reduces subjectivity and ensures fairness across all applications.

In higher-volume lending operations, these checks are often standardized into internal review guidelines to ensure uniform decision-making across agents.

How document review affects loan outcomes

Document review can directly change the outcome of a loan application even after automated approval.

For example:

A loan may be downgraded if income cannot be verified

A loan may be paused if identity documents are unclear

A loan may be escalated for manual review if inconsistencies are detected

A loan may be approved faster if documents match pre-filled data

This makes document review an active part of risk management rather than a passive compliance step.

Because all documents sit inside the customer profile, lenders can evaluate them alongside loan history, repayments, and transaction data in one place.

Customer documents are one of the most important signals in lending decisions. They help lenders move beyond assumptions and rely on verified information when assessing risk.

With Lendsqr, all KYC documents are centralized within the customer profile, making it easier to review, validate, and act on them as part of the lending workflow.