Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

Triggering manual loan repayment

Updated

On this page

Sometimes a loan repayment does not go through as expected. A borrower’s card may fail, a direct debit mandate may not execute, or the account may not have sufficient funds at the time of collection.

When this happens, lenders often need to recover the payment without waiting for the next scheduled cycle. This is where manual repayment collection becomes useful.

On Lendsqr, you can trigger a manual repayment to retry or recover a failed or overdue loan installment directly from the loan details page.

When to use manual repayment collection

Manual repayment is used in exceptional cases where automated repayment has failed or needs to be retried.

Common scenarios include:

Scheduled repayment failed due to insufficient funds

The card transaction was declined

The direct debit mandate did not execute

Borrower has confirmed funds are now available

The loan is overdue and requires recovery action

Example scenario

A borrower has a ₦50,000 monthly repayment scheduled. The first debit attempt fails due to a low account balance. Two days later, the borrower confirms that the salary has been credited.

Instead of waiting for the next cycle, the lender triggers a manual repayment to recover the installment immediately and reduce the risk of further delinquency.

What to know before you trigger a manual repayment

Before initiating a manual repayment, it is important to confirm:

The repayment is still due

The amount matches the repayment schedule

The payment method on file is valid

The borrower has been notified where necessary

Previous failure reasons have been reviewed

Manual repayment directly initiates a financial transaction, so incorrect usage may lead to disputes or failed retries.

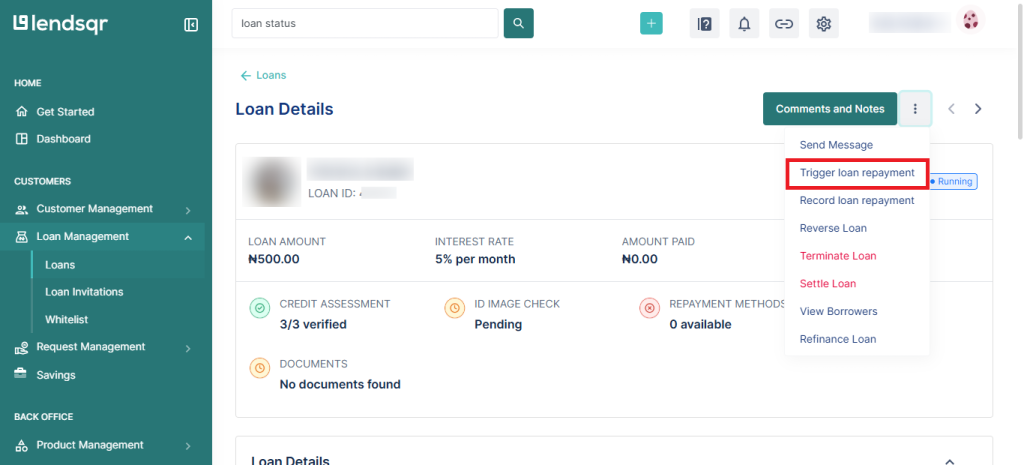

How to trigger manual loan repayment

To trigger manual loan repayment:

Follow the steps highlighted in the section above to locate a loan.

Click the three dots at the top right corner of the loan and then click on the “Trigger Loan Repayment” button. A modal will be displayed to you.

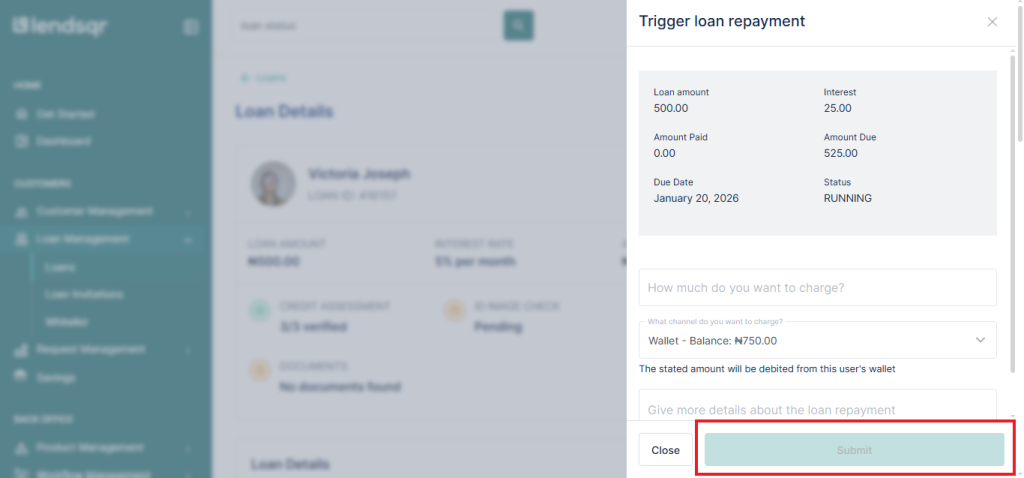

Enter the repayment details, i.e., amount to be triggered for repayment, channel (Wallet, card, or Direct Debit), and the comments to specify what happened exactly.

Click on “Submit” to repay the loan or part of the loan

Enter your 2FA token to authorize the system to trigger repayment from the user’s wallet, card, or Direct Debit.

Once your payment is processed successfully, the loan schedule will be automatically updated.

Triggering for manual loan repayment will only work if the user has a card, wallet, or Direct Debit with funds in it. To repay a loan that was paid from external transfers or cash, read more here: Repaying a User’s Loan. Once submitted, the system immediately attempts to collect the repayment.

Manual repayment gives lenders control over recovering failed or overdue loan installments when automated collection does not succeed.

With Lendsqr, lenders can trigger repayment attempts directly from the loan details page, track outcomes in real time, and take appropriate follow-up actions based on the response.