Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

Duplicating an existing credit risk rule

Updated

On this page

In digital lending, consistency and speed are essential for making reliable credit decisions. Lenders often process large volumes of loan applications, each requiring careful evaluation to determine borrower eligibility, assess risk, and define appropriate loan terms. Without structured systems in place, this process can quickly become inefficient, inconsistent, and difficult to scale.

To address this challenge, lending platforms use credit risk rules. Within Lendsqr, credit risk rules help automate lending decisions by applying predefined rules and checks that determine whether a borrower qualifies for a loan and what offer should be extended. Rather than relying entirely on manual judgment, lenders can define repeatable decision logic that improves efficiency while maintaining control over lending policies.

As lending strategies evolve, lenders may also need to create variations of existing rules to serve new borrower groups or test alternative approval conditions. Instead of building every one from the ground up, Lendsqr allows administrators to duplicate existing rules and make targeted adjustments. This functionality saves time, improves consistency, and supports faster experimentation with lending strategies.

A credit risk rule is a set of lending rules and evaluation checks used to automatically determine whether a borrower qualifies for a loan and what type of loan offer they should receive.

These models function as the decision-making engine behind automated lending. Rather than reviewing every application manually, lenders can define conditions that evaluate borrowers against specific criteria. Once the system completes these checks, it generates an outcome based on the lender’s predefined rules.

Credit risk rules often assess variables such as credit score, income level, employment history, repayment behavior, and previous loan performance. Depending on the lender’s setup, the system may approve an application, decline it, or provide a tailored loan offer aligned with the borrower’s risk profile.

For example, a lender may configure a model that automatically approves borrowers with stable income histories and strong repayment performance while flagging high-risk applicants for additional review. Another lender may use separate decision logic for different customer segments, such as salaried employees, business owners, or gig economy workers.

At a practical level, decision models help lenders standardize credit decisions, reduce manual effort, and improve operational scalability.

Why credit risk rules matter in lending

Loan decisions involve balancing accessibility with risk management. Approving too many high-risk borrowers may increase defaults, while overly strict requirements may limit business growth and customer acquisition.

Credit risk rules help lenders strike this balance by creating structured and repeatable approval logic.

One major benefit is consistency. When lending decisions rely solely on manual reviews, outcomes may vary depending on the person evaluating applications. Credit risk rules reduce inconsistency by ensuring applications are assessed according to the same predefined criteria every time.

Speed is another important advantage. Automated evaluations reduce processing delays, enabling lenders to provide faster responses to borrowers. This often improves customer satisfaction and operational efficiency.

Credit risk rules also improve scalability. As application volumes increase, manually reviewing every request becomes increasingly difficult. Automated decisioning allows lenders to grow without proportionally increasing operational workload.

Additionally, credit risk rules support smarter risk management. Since rules can be customized according to borrower segments and lending goals, organizations can design strategies that reflect their specific risk appetite.

Why lenders duplicate credit risk rules

As lending businesses grow, strategies often become more sophisticated. A single set of credit risk rules may no longer meet the needs of every borrower category, product type, or market segment.

This is where duplication becomes valuable.

Duplicating a credit risk rule allows lenders to create a new model based on an existing one without rebuilding the entire configuration from scratch. Instead of recreating every rule manually, administrators can copy a working model and modify only the elements that need adjustment.

For example, imagine a lender already has a successful credit risk rule designed for salaried employees. The organization now wants to expand into lending for self-employed borrowers. Although the new borrower segment may require different income verification methods or offer structures, many core lending rules may remain unchanged.

Rather than creating a completely new credit risk rule, the lender can duplicate the existing one and adjust only the necessary parameters. This significantly reduces setup time while maintaining consistency across lending strategies.

Similarly, lenders may duplicate rules to test alternative approval thresholds, compare repayment performance across borrower groups, or launch pilot lending programs.

At a strategic level, duplication supports experimentation without disrupting existing workflows.

Creating a new credit risk rule from scratch can be time-consuming, especially when multiple lending rules, offer conditions, and verification checks are involved.

Duplication eliminates the need to rebuild existing configurations manually. By starting with a working framework, lenders can create new models more efficiently and accelerate deployment timelines.

Improved consistency

Consistency is important in lending operations.

When lenders manually recreate credit risk rules, there is always a risk of overlooking important rules or introducing unintended differences. Duplication reduces this risk by preserving the original model structure, allowing teams to maintain alignment while making targeted adjustments.

Easier testing and experimentation

Lenders frequently experiment with new lending strategies to improve approval rates, reduce defaults, or expand customer reach.

Duplicating a credit risk rule creates a safe way to test changes without affecting an existing production workflow. Teams can compare performance across different rule variations and evaluate outcomes before fully implementing new strategies.

Better borrower segmentation

Different borrower groups often require different lending approaches.

For example, a lender may use one credit risk rule for salaried workers, another for small business owners, and a third for repeat borrowers with strong repayment histories. Duplicating existing models makes it easier to adapt lending rules for each segment while preserving operational efficiency.

Real-world scenarios for credit risk rule duplication

Understanding how duplication works in practice helps illustrate its value.

Consider a lender that initially serves only salaried employees. After observing strong performance, the lender decides to expand into freelance lending. Since freelancers often have variable income patterns, the organization may need slightly different verification requirements and offer logic.

Rather than building an entirely new credit risk rule, the lender duplicates the salaried employee model and modifies specific rules related to income verification and eligibility thresholds.

Another example involves geographic expansion. A lender entering a new market may duplicate an existing configuration and adjust approval settings based on regional economic conditions or repayment behavior patterns.

Organizations may also duplicate risk rules to support seasonal lending campaigns or pilot programs aimed at testing revised approval strategies.

Duplicating a credit risk rule within the Lendsqr admin console is designed to be straightforward.

Step 1: Navigate to credit risk rules

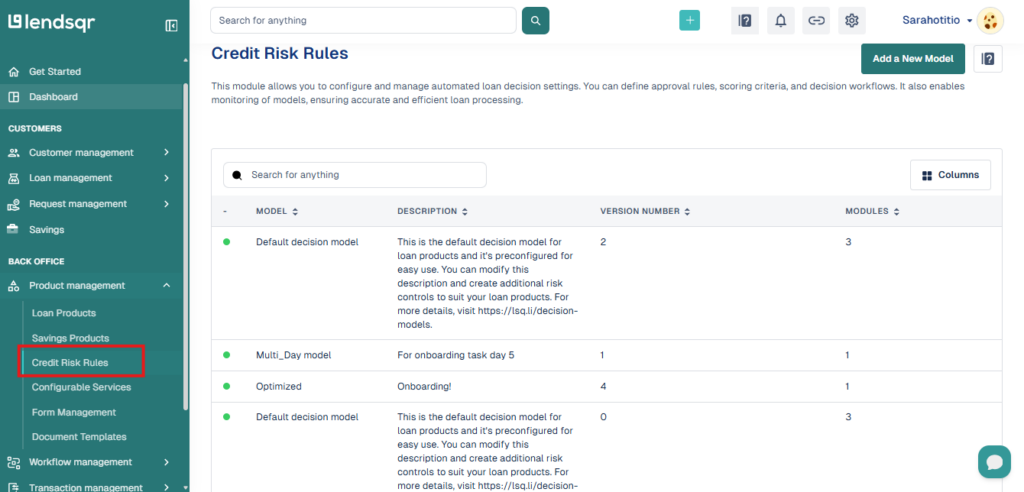

Begin by logging into the Lendsqr admin console. Using the side navigation menu, locate the Product Management grouping and click on the Credit Risk Rules tab. This section serves as the central location for creating, reviewing, and managing lending decision logic.

Step 2: Select the rule to duplicate

Within the Credit Risk Rule page, identify the existing model you want to use as the foundation for the new version.

Choose a model that closely matches the intended lending workflow to minimize unnecessary adjustments later.

Step 3: Open credit risk rule options

On the selected model, click the options button represented by the three-dot menu.

From the available options, select Duplicate.

This action creates a copy of the selected model and redirects you to the decision model setup page.

Step 4: Update risk rule information

Once the duplicated credit risk rule opens, enter a new name and description.

The name should clearly distinguish the duplicated model from the original. For example, instead of a generic title, lenders may use labels such as “Self-Employed Borrowers” or “Pilot Approval Model.”

Descriptions should briefly explain the model’s purpose to improve internal clarity and collaboration.

Step 5: Review and save

Before finalizing the duplicated risk rule, carefully review all inherited rules and configurations.

Although duplication preserves existing settings, lenders should confirm that approval logic, offer conditions, and borrower requirements align with the intended strategy.

After reviewing the configuration, save the model to make it available for use.

Common mistakes to avoid

One common mistake lenders make is duplicating a credit risk rule without thoroughly reviewing inherited rules. Since duplicated models retain existing configurations, failing to update outdated criteria may lead to unintended lending outcomes.

Another issue involves unclear naming conventions. Poorly labeled models can create confusion for operational teams managing multiple lending strategies.

Lenders should also avoid making too many simultaneous changes when testing new strategies. Incremental adjustments make performance evaluation easier and reduce confusion when analyzing results.

Finally, organizations should avoid treating duplication as a substitute for regular model reviews. Lending conditions evolve, and decision logic should be updated periodically to reflect changing borrower behavior and risk patterns.

Duplicating credit risk rules on the Lendsqr admin console provides lenders with a practical way to adapt lending strategies without rebuilding workflows from scratch. Whether serving new borrower segments, testing revised approval criteria, or launching new lending products, duplication enables organizations to move faster while maintaining consistency and control.

By using duplication strategically, lenders can improve operational efficiency, experiment with confidence, and scale decision-making processes more effectively.