Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

How to use prequalified borrowers to offer loans in Lendsqr

Updated

On this page

In digital lending, not every borrower who applies for a loan should be evaluated in the same way. Some customers are already known, trusted, or have been pre-approved based on historical data, behavioral patterns, or internal lender rules. To support this type of controlled lending approach, Lendsqr provides a feature known as prequalified borrowers.

Previously referred to as whitelists, prequalified borrowers allow lenders to define a set of users who are eligible for specific loan products without going through the standard discovery or qualification process. This helps lenders streamline loan origination, reduce risk for trusted customers, and create faster loan approval journeys for selected borrower groups.

This guide explains what prequalified borrowers are, why they matter, and how to configure and use them effectively within your lending operations.

Understanding prequalified borrowers

Prequalified borrowers are a curated list of customers who have been identified as eligible for specific lending products. These users bypass certain standard qualification checks because they already meet predefined criteria set by the lender.

In most lending systems, borrowers must go through a full evaluation process before being approved for credit. This includes credit checks, income verification, behavioral scoring, and other risk-based assessments. However, in some cases, lenders already have sufficient confidence in certain customers.

For example, customers with strong repayment history, salaried employees in partner organizations, or users who have successfully completed multiple loan cycles may be added to a prequalified group. These borrowers can then access loan products more quickly, with fewer friction points during the application process.

This approach improves efficiency while still maintaining control over lending decisions.

Why prequalified borrowers are important

The prequalified borrowers feature plays a critical role in balancing speed, trust, and risk management in lending operations.

One of the primary benefits is faster loan access for trusted customers. Instead of repeating full eligibility checks, lenders can instantly approve or prioritize users who already meet internal standards. This improves customer experience and encourages repeat borrowing.

Another important benefit is improved operational efficiency. By reducing the number of checks required for known customers, lenders can focus their risk and underwriting resources on new or higher-risk applicants.

Prequalified borrowers also help improve customer retention. When borrowers experience faster approvals and smoother loan journeys, they are more likely to return and continue using the platform.

Finally, this feature supports strategic lending segmentation. Lenders can design different borrowing experiences for different customer groups, such as salaried employees, gig workers, or high-value customers.

How prequalified borrowers work in Lendsqr

The prequalified borrowers feature works by linking specific users to defined loan products or eligibility rules. Once a borrower is added to the prequalified list, the system recognizes them during loan application and adjusts the decision flow accordingly.

Instead of going through full evaluation logic, the borrower may bypass certain checks or receive a simplified approval path depending on how the loan product is configured.

This does not mean risk is ignored. Instead, it means risk is managed in advance through selection criteria. Lenders are responsible for ensuring that only qualified users are added to the list.

The feature is tightly integrated with loan products, meaning each product can have its own set of prequalified borrowers depending on the lender’s strategy.

Step-by-step guide to using prequalified borrowers

Lenders can manage prequalified borrowers directly from the Lendsqr Admin Console. The process is designed to be simple and flexible, allowing quick updates as lending strategies evolve.

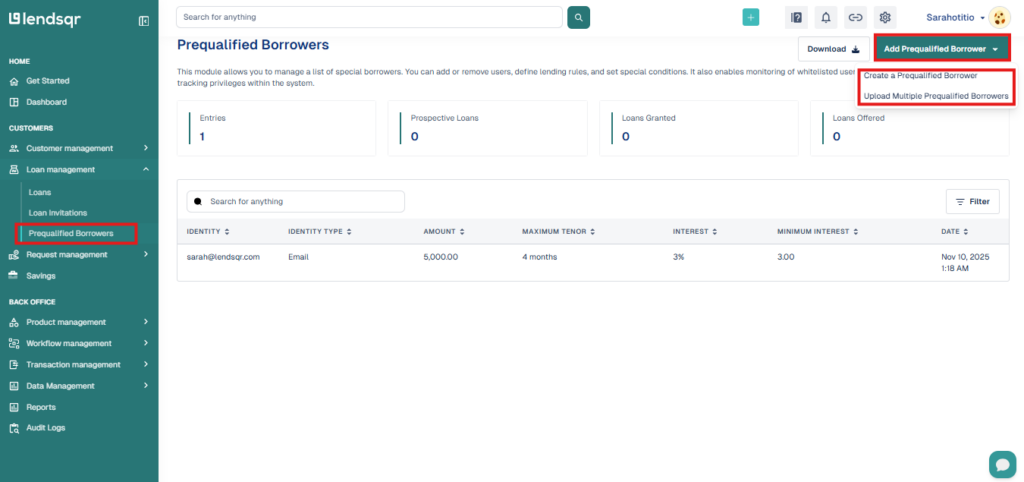

Step 1: Navigate to Loan management

Begin by logging into the Lendsqr Admin Console.

From the side navigation menu, locate the Loan Management section. This area contains all configurations related to loan products, decision rules, and borrower eligibility settings.

Within Loan management, select the section that handles borrower eligibility or prequalification settings.

This is where lenders can manage which customers are marked as prequalified for specific lending products.

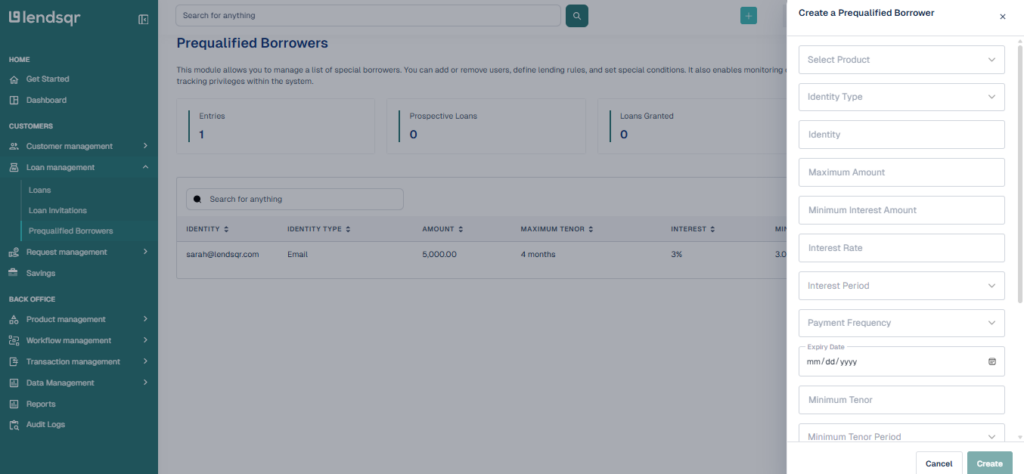

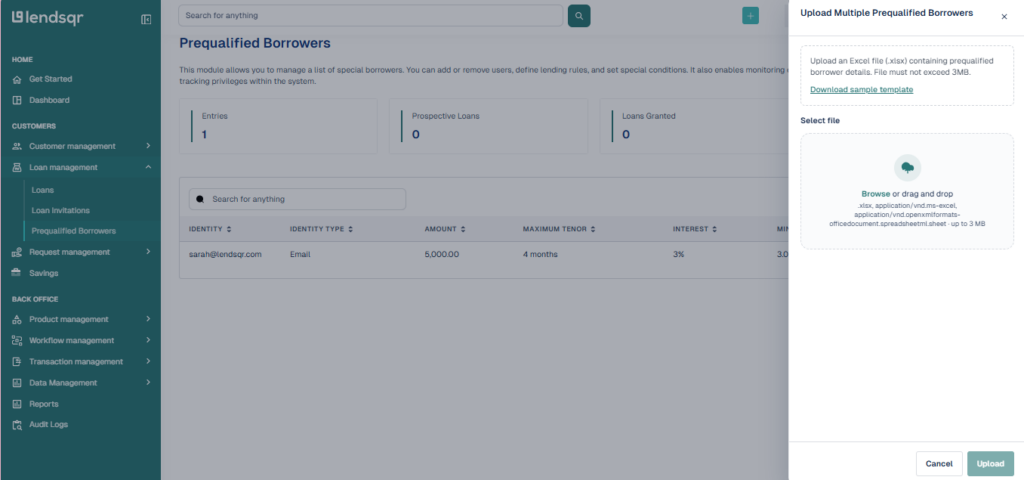

Step 2: Select prequalified borrowers and add them to the prequalified borrowers list

On the top right corner of this tab, there is a section to add prequalified borrowers. This can be done for individuals or for multiple prequalified borrowers at a time.

Step 4: Save and activate configuration

After inputting the appropriate borrowers, save your configuration changes. Once saved, the system immediately applies the updated prequalification rules to the selected loan product.

From this point onward, any borrower included in the list will be treated as prequalified during loan application flows.

How lenders prequalify customers

Lenders can prequalify customers in two primary ways, depending on operational needs and scale.

Individually

Customers can be added one at a time by entering their details directly into the Lendsqr Admin Console. These details typically include identifiers such as phone number, customer ID, or BVN.

This method is best suited for small groups of trusted borrowers or specific high-value customers who require immediate eligibility for loan products.

In bulk

Lenders can also prequalify multiple customers at once by uploading a preformatted CSV file containing customer records.

This approach is more efficient for large-scale onboarding scenarios such as corporate partnerships, cooperatives, payroll-linked lending programs, or referral-based lending schemes.

Bulk upload ensures consistency, reduces manual effort, and allows lenders to quickly activate eligibility for large borrower groups.

To get the most value from this feature, lenders should follow structured best practices when managing prequalified groups.

First, ensure that selection criteria are clearly defined. Borrowers should only be added based on measurable performance indicators such as repayment history, account activity, or verified employment relationships.

Second, regularly review and update the prequalified list. Borrower behavior can change over time, so it is important to ensure that eligibility remains accurate and relevant.

Third, avoid overusing prequalification for too many users. The feature is most effective when used for clearly defined, low-risk segments rather than broad populations.

Finally, align prequalification rules with your overall credit risk strategy to ensure consistency across all lending decisions.

Common mistakes to avoid

One common mistake lenders make is treating prequalified borrowers as automatically risk-free. While these users are trusted, they should still be monitored for ongoing performance.

Another issue is failing to update the list regularly. Static borrower lists can quickly become outdated and may include users who no longer meet eligibility criteria.

Lenders should also avoid unclear selection rules, as this can lead to inconsistent lending decisions across teams.

Conclusion

Prequalified borrowers provide lenders with a powerful way to streamline lending operations while maintaining control over risk. By identifying trusted customers in advance, lenders can reduce friction, improve customer experience, and optimize operational efficiency.

When used correctly, this feature enables faster loan delivery for reliable borrowers while allowing lenders to focus their underwriting efforts on new or higher-risk applicants. As lending portfolios grow, prequalification becomes an essential tool for balancing speed, trust, and risk management in a scalable way.

By integrating prequalified borrowers into your lending strategy, you can create a more efficient and customer-friendly loan experience without compromising on control or credit quality.