Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

Mapping a credit risk rule to a loan product

Updated

On this page

Effective lending depends on more than offering the right financial products. Lenders also need a reliable way to ensure every loan application is evaluated consistently, fairly, and according to predefined business rules. Without structured assessment systems, loan decisions may become inconsistent, increase operational workload, and expose lenders to unnecessary credit risks.

In the Lendsqr Admin Console, credit risk rules help automate and standardize how loan applications are assessed. These rules determine whether borrowers qualify for a loan product and what lending outcomes should be generated based on predefined criteria. However, creating credit risk rules alone is not enough. To ensure the right evaluation process applies to the right borrowers, lenders must map those rules to specific loan products.

Mapping credit risk rules to loan products ensures that applications are assessed using the correct approval logic every time. For example, a lender offering nano loans to gig workers may use a lightweight assessment process that evaluates basic identity information and transaction behavior, while a salary-backed loan product may require stricter employment and income checks. By connecting the right credit risk rules to each product, lenders remove unnecessary manual work while maintaining consistency in decision-making.

Credit risk rules are structured lending criteria that determine how borrower applications are evaluated.

These rules help lenders automate loan assessments by defining conditions borrowers must meet before receiving approval. Rather than reviewing every application manually, lenders can configure automated logic that evaluates customer information and generates decisions according to business requirements.

Depending on the lending strategy, credit risk rules may evaluate factors such as borrower identity, repayment history, employment status, transaction behavior, income consistency, or previous interactions with the platform.

For example, a lender targeting first-time borrowers may create more conservative approval rules to reduce exposure to risk. On the other hand, repeat borrowers with strong repayment histories may qualify under more flexible conditions.

At a practical level, credit risk rules improve efficiency, consistency, and scalability by reducing dependence on manual loan reviews.

Why mapping credit risk rules matters

Creating credit risk rules is only one part of building an effective lending system. To work correctly, those rules must be connected to the appropriate loan products.

Mapping ensures that every loan application follows the intended approval process for that product.

Without mapping, lenders risk inconsistencies in how applications are reviewed. Borrowers may be assessed using the wrong criteria, resulting in inaccurate loan decisions or operational inefficiencies.

For example, imagine a lender offering nano loans for gig workers alongside larger salary-backed loans for formally employed borrowers. These borrower groups often have different risk profiles and financial behaviors.

Gig workers may not have traditional payslips or employer verification records. Instead, lenders may choose to assess transaction consistency and wallet activity. Salary-backed borrowers, however, may require stricter employment checks and documented income verification.

By mapping the correct credit risk rules to each product, lenders ensure borrowers are assessed according to the requirements that best match the loan offering.

This setup also reduces manual intervention, improves approval consistency, and enables organizations to scale more effectively.

Real-world example of mapped credit risk rules

To better understand how mapping works, consider a lender offering short-term nano loans for ride-hailing drivers and delivery workers.

Because many gig workers earn variable income, the lender may create a simplified credit risk rule that evaluates only essential information such as identity verification, transaction activity, and average income patterns.

After building the rule, the lender maps it specifically to the gig worker nano loan product.

As a result, whenever borrowers apply for that product, applications are automatically evaluated according to the intended assessment logic. Loan officers do not need to manually review every request or apply separate criteria individually.

At the same time, the lender may maintain a completely different set of credit risk rules for higher-value loans requiring stronger income documentation and employment verification.

This flexibility allows lenders to personalize decision-making while maintaining operational consistency.

Benefits of mapping credit risk rules to loan products

Mapping credit risk rules to products provides several important operational benefits.

Consistent borrower evaluation

One of the most significant advantages is consistency.

When every loan application for a specific product follows the same assessment framework, lenders reduce inconsistencies in decision-making. Borrowers are evaluated according to standardized rules rather than subjective judgments.

This improves fairness and helps maintain trust in lending operations.

Reduced manual work

Manual loan reviews often slow down lending operations and increase operational costs.

Mapping credit risk rules eliminates much of this manual effort by automating borrower evaluations. Applications can be processed more quickly, allowing lenders to handle larger volumes efficiently.

For growing lending businesses, this automation becomes especially valuable.

Better risk management

Different loan products carry different levels of risk.

By assigning specific credit risk rules to each product, lenders can align approval criteria with the risk profile of individual offerings. Higher-risk products may require stricter evaluations, while low-risk offerings may support faster approvals.

This flexibility strengthens portfolio management and improves lending outcomes.

Mapped credit risk rules create a scalable framework where each product automatically follows predefined assessment logic. This allows organizations to grow operations without proportionally increasing administrative effort.

How to map credit risk rules to a loan product

Once a credit risk rule has been created, linking it to a loan product is straightforward within the Lendsqr Admin Console.

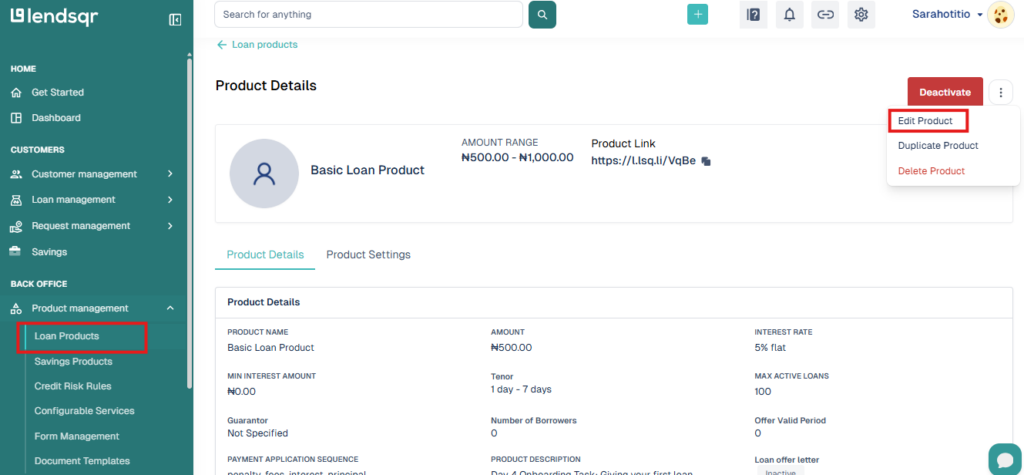

Step 1: Navigate to loan products

Begin by logging into the Lendsqr Admin Console.

From the side navigation menu, locate the Product Management tab and select the Loan Products sub-tab.

This section contains all available lending products and serves as the management center for creating and modifying loan offerings.

Step 2: Create or edit a loan product

Next, decide whether you want to create a new loan product or update an existing one.

If you are launching a new lending product, begin the creation process as usual. If the product already exists, open it for editing.

At this stage, lenders should already have a clear understanding of the borrower segment the product targets and the type of assessment logic required.

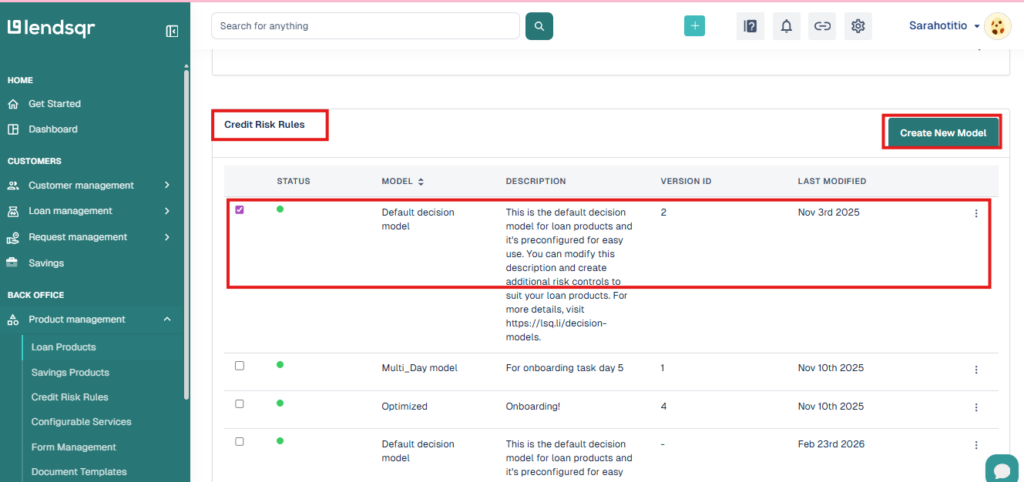

Step 3: Select the credit risk rule

Scroll to the bottom of the loan product page.

Locate the section where you can select the credit risk rule you want to use for that loan product. Choose the rule that best aligns with the intended borrower profile and lending requirements or you can create a new one.

Carefully reviewing the selected rule before proceeding helps reduce mismatches between loan products and evaluation logic.

Step 4: Save changes

After selecting the preferred credit risk rule, click Save Changes to finalize the setup.

Once saved, all future applications submitted under that loan product will automatically be evaluated using the selected credit risk rule.

This ensures borrowers are assessed according to the predefined approval logic associated with that specific lending product.

Common mistakes to avoid

Although mapping credit risk rules is relatively simple, lenders sometimes make avoidable errors.

One common mistake is assigning the wrong rule to a product. Since different borrower groups often require different evaluation methods, mismatched rules may lead to inaccurate approvals or unnecessary declines.

Another issue involves failing to review mapped rules after updates. If credit risk rules are modified but not revalidated against existing products, unintended lending outcomes may occur.

Lenders should also avoid using identical rules across every product without considering borrower differences. Tailored evaluation logic often produces better approval quality and stronger portfolio performance.

Finally, organizations should periodically review mapped rules to ensure they still reflect business goals, borrower behavior, and market conditions.

Best practices for managing credit risk rule mappings

The most effective lenders treat mapping as an ongoing optimization process rather than a one-time configuration.

Organizations should regularly evaluate whether loan products are performing as expected under current approval rules. High default rates or unusually low approval volumes may signal the need for adjustments.

It is also important to maintain clear naming conventions for credit risk rules to reduce confusion when managing multiple lending products.

Internal testing before launching new products can further improve outcomes by confirming that borrowers are being assessed according to intended logic.

As lending operations become more sophisticated, maintaining accurate connections between products and evaluation criteria becomes increasingly important. Mapping credit risk rules to loan products helps lenders automate decisions, improve consistency, reduce manual effort, and strengthen portfolio management.

By carefully aligning each product with the right credit risk rule, lenders can create more scalable and reliable lending operations while maintaining full control over how borrower applications are assessed.