Access your Back Office at your fingertips.

Download the app now on Google Play Store.

Scan the QR code

You can also scan QR code with your phone to download the app.

How loan penalty charges work and when to use each type

When a borrower misses a repayment, lenders can apply a penalty charge. Lendsqr supports three penalty calculation methods: fixed, percentage, and hybrid. Choosing the right one shapes how much you recover, how borrowers respond to late payments, and how fair your collections process feels. This article explains how each method works, when to use it, and what happens in edge cases like repeated defaults.

What a penalty charge is and why it matters

A penalty charge is an extra fee added to a borrower’s balance when a repayment falls past its due date. It compensates the lender for the cost of delayed collection and creates a financial incentive for borrowers to pay on time.

Getting penalty design right matters more than most lenders realize. A penalty that is too low gives borrowers little reason to prioritize repayment. A penalty that is too high can push a struggling borrower into a debt spiral, making recovery harder rather than easier. The goal is a structure that motivates timely repayment without making defaults worse for borrowers who would repay if given a fair chance.

The three penalty methods on Lendsqr

Fixed penalty

A fixed penalty applies a flat fee each time a repayment falls overdue. The amount does not change based on how much the borrower owes.

How it calculates: A ₦500 fixed penalty means a borrower who misses a payment owes an extra ₦500 on top of their overdue amount.

When to use it: Fixed penalties work best for small, short-term loan products where loan amounts are similar across borrowers. A flat fee is easy for borrowers to understand and predict. It also means your penalty income stays consistent regardless of how much each borrower owes.

Real-world example: A lender offering quick loans between ₦5,000 and ₦20,000 sets a fixed penalty of ₦300. Every borrower who misses a payment knows exactly what they owe in addition to their installment. There is no ambiguity, and the fee feels proportionate while still creating a repayment incentive.

Percentage penalty

A percentage penalty calculates the fee as a portion of the overdue amount. The bigger the outstanding balance, the larger the penalty.

How it calculates: At 2%, a borrower with ₦50,000 overdue pays ₦1,000 in penalties.

When to use it: Percentage penalties are better suited to products with a wide range of loan amounts. A flat fee that feels proportionate on a ₦10,000 loan feels trivial on a ₦500,000 loan. Scaling the penalty to the outstanding balance ensures the incentive to repay stays meaningful regardless of loan size.

Real-world example: A lender offering business loans ranging from ₦100,000 to ₦2,000,000 sets a 1.5% monthly penalty on overdue balances. A borrower with ₦200,000 outstanding pays ₦3,000 in penalties per month, while a borrower with ₦1,000,000 outstanding pays ₦15,000. The proportionality keeps the penalty meaningful at both ends of the range.

Hybrid penalty

The hybrid method combines a flat fee with a percentage of the overdue amount. It also supports a minimum floor and a maximum cap, giving lenders fine-grained control over how penalties scale.

How it calculates: A lender sets 1% of the overdue amount plus a ₦200 flat fee, with a minimum of ₦300 and a cap of ₦3,000. If a borrower owes ₦10,000, the calculated penalty would be ₦100 (1%) plus ₦200, totaling ₦300. Since that meets the minimum, ₦300 applies. If a borrower owes ₦400,000, the calculation would yield ₦4,200, but the cap holds it to ₦3,000.

When to use it: Hybrid works best when you want scaling penalties but need guardrails at both ends of the loan range. The floor keeps the penalty meaningful on small loans. The cap prevents it from becoming punitive on large balances.

How grace periods interact with penalties

Before a penalty activates, most lenders configure a grace period. This is a set number of days after the due date during which no penalty applies.

Three to seven days is a common grace period for salaried borrowers whose pay may arrive a day or two late. It shows goodwill and reduces the volume of penalty disputes from borrowers who were only slightly late.

Setting the grace period to zero means penalties kick in the day after a missed payment. This suits short-duration products where each day of delay matters, but requires clear upfront communication to borrowers.

How to configure penalty charges in Lendsqr

To create a penalty fee for an existing loan product, follow the steps below:

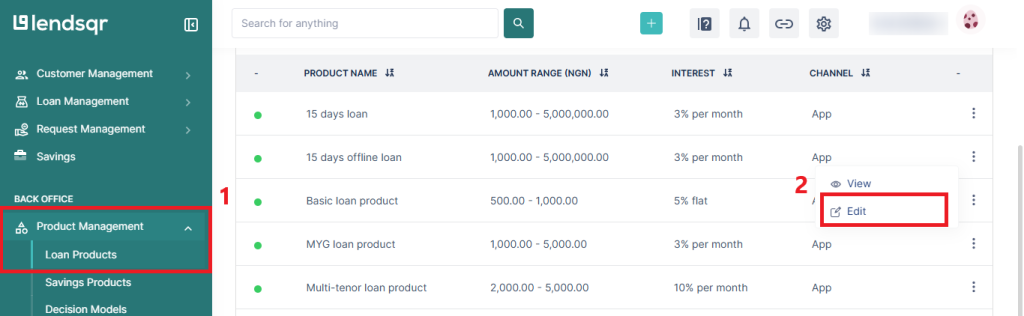

From your dashboard, navigate to “Product Management” and select “Loan Products.” Locate the product you want to configure and click the three vertical dots on the right of that row.

Click on “Edit” from the menu options.

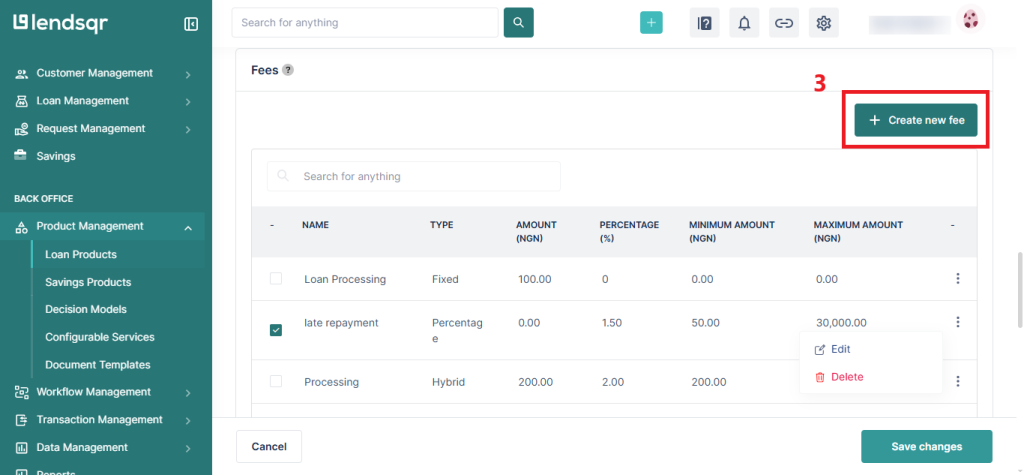

Within the loan product settings, scroll to the “Fees” section. This is where you can define penalty charges tied to the loan. Click on “Create new fee”.

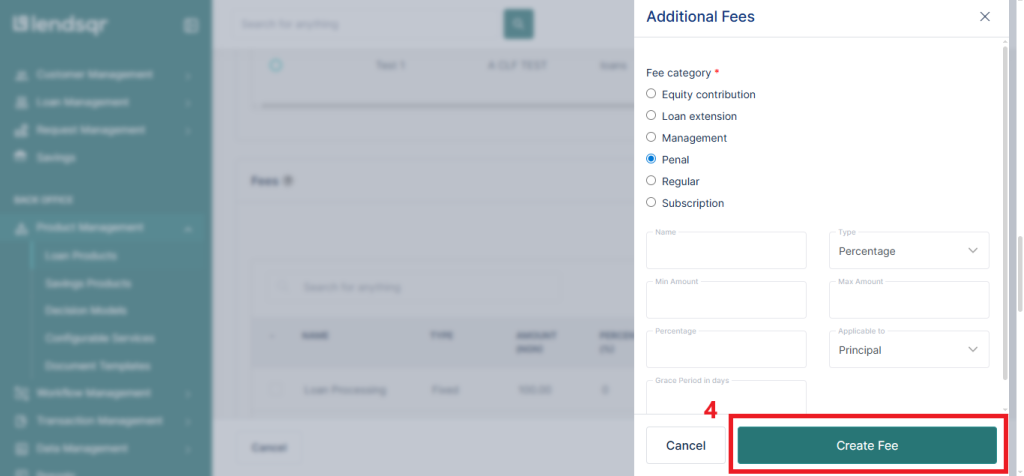

Select “Penal” and fill in the penalty fee details by providing the information in the required fields. Once all fields are filled in, click the “Create Fee” button at the bottom right to save changes.

The penalty configuration applies immediately to any new loans created under that product. You can also configure penalties while creating a new loan product from scratch using the same Fees section.

feature")